- Switzerland

- /

- Life Sciences

- /

- SWX:SKAN

3 European Stocks Trading At An Estimated Discount Of Up To 49.8%

Reviewed by Simply Wall St

As European markets navigate a complex landscape of trade tensions and inflation concerns, the pan-European STOXX Europe 600 Index has managed to edge higher, buoyed by hopes of increased government spending despite mixed performances across major stock indexes. In this environment, identifying undervalued stocks can be particularly appealing for investors looking to capitalize on potential discounts; these opportunities often arise when market uncertainty leads to mispricing relative to intrinsic value.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Romsdal Sparebank (OB:ROMSB) | NOK130.30 | NOK257.92 | 49.5% |

| Vimi Fasteners (BIT:VIM) | €0.97 | €1.90 | 49% |

| TTS (Transport Trade Services) (BVB:TTS) | RON4.25 | RON8.44 | 49.6% |

| Stratec (XTRA:SBS) | €25.90 | €50.97 | 49.2% |

| F-Secure Oyj (HLSE:FSECURE) | €1.722 | €3.43 | 49.8% |

| Deutsche Beteiligungs (XTRA:DBAN) | €26.50 | €52.70 | 49.7% |

| dormakaba Holding (SWX:DOKA) | CHF687.00 | CHF1352.81 | 49.2% |

| Carasent (OM:CARA) | SEK20.715 | SEK40.72 | 49.1% |

| Fodelia Oyj (HLSE:FODELIA) | €7.10 | €13.91 | 49% |

| Galderma Group (SWX:GALD) | CHF95.77 | CHF190.18 | 49.6% |

Let's dive into some prime choices out of the screener.

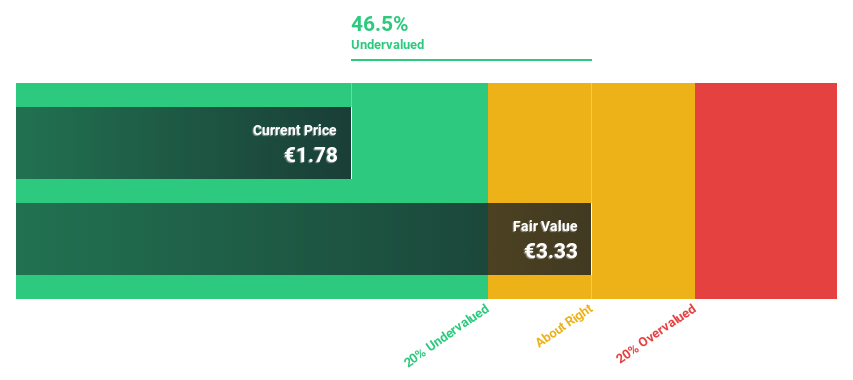

F-Secure Oyj (HLSE:FSECURE)

Overview: F-Secure Oyj is a cybersecurity company that provides security solutions in Finland and internationally, with a market cap of €300.79 million.

Operations: The company generates revenue primarily from its Consumer Security segment, amounting to €146.26 million.

Estimated Discount To Fair Value: 49.8%

F-Secure Oyj appears undervalued based on cash flows, trading at €1.72, significantly below its estimated fair value of €3.43. Despite high debt levels, the company is forecast to grow earnings by 13.5% annually, outpacing the Finnish market's growth rate. Recent earnings showed a slight decline in net income to €21.07 million for 2024 despite increased sales of €146.26 million, suggesting potential for improved cash flow leverage as revenues rise faster than the market average.

- Upon reviewing our latest growth report, F-Secure Oyj's projected financial performance appears quite optimistic.

- Dive into the specifics of F-Secure Oyj here with our thorough financial health report.

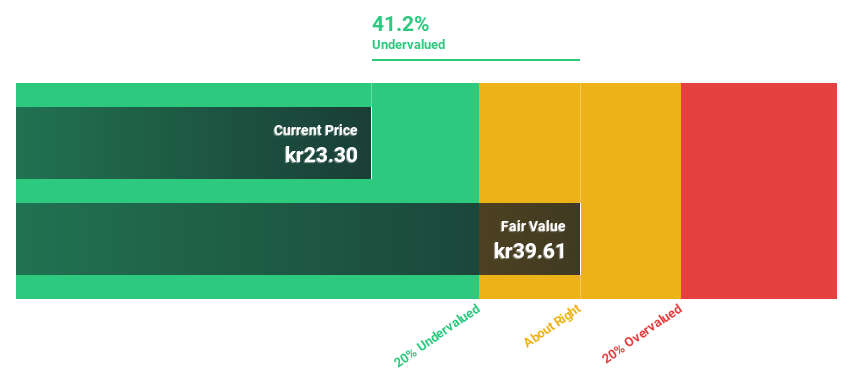

LINK Mobility Group Holding (OB:LINK)

Overview: LINK Mobility Group Holding ASA, along with its subsidiaries, offers mobile and communication-platform-as-a-service solutions and has a market capitalization of NOK6.23 billion.

Operations: The company's revenue segments consist of Central Europe (NOK1.69 billion), Western Europe (NOK2.11 billion), Northern Europe (NOK1.54 billion), and Global Messaging (NOK1.66 billion).

Estimated Discount To Fair Value: 43.1%

LINK Mobility Group Holding is trading at NOK22.1, significantly below its estimated fair value of NOK38.86, highlighting its undervaluation based on cash flows. Recent earnings show net income surged to NOK255.48 million from NOK67.28 million last year, with revenue reaching NOK6.99 billion. Despite large one-off items affecting results and a low forecasted return on equity, expected annual profit growth of 32% surpasses the Norwegian market's rate, indicating strong potential for future performance improvement.

- The analysis detailed in our LINK Mobility Group Holding growth report hints at robust future financial performance.

- Click here to discover the nuances of LINK Mobility Group Holding with our detailed financial health report.

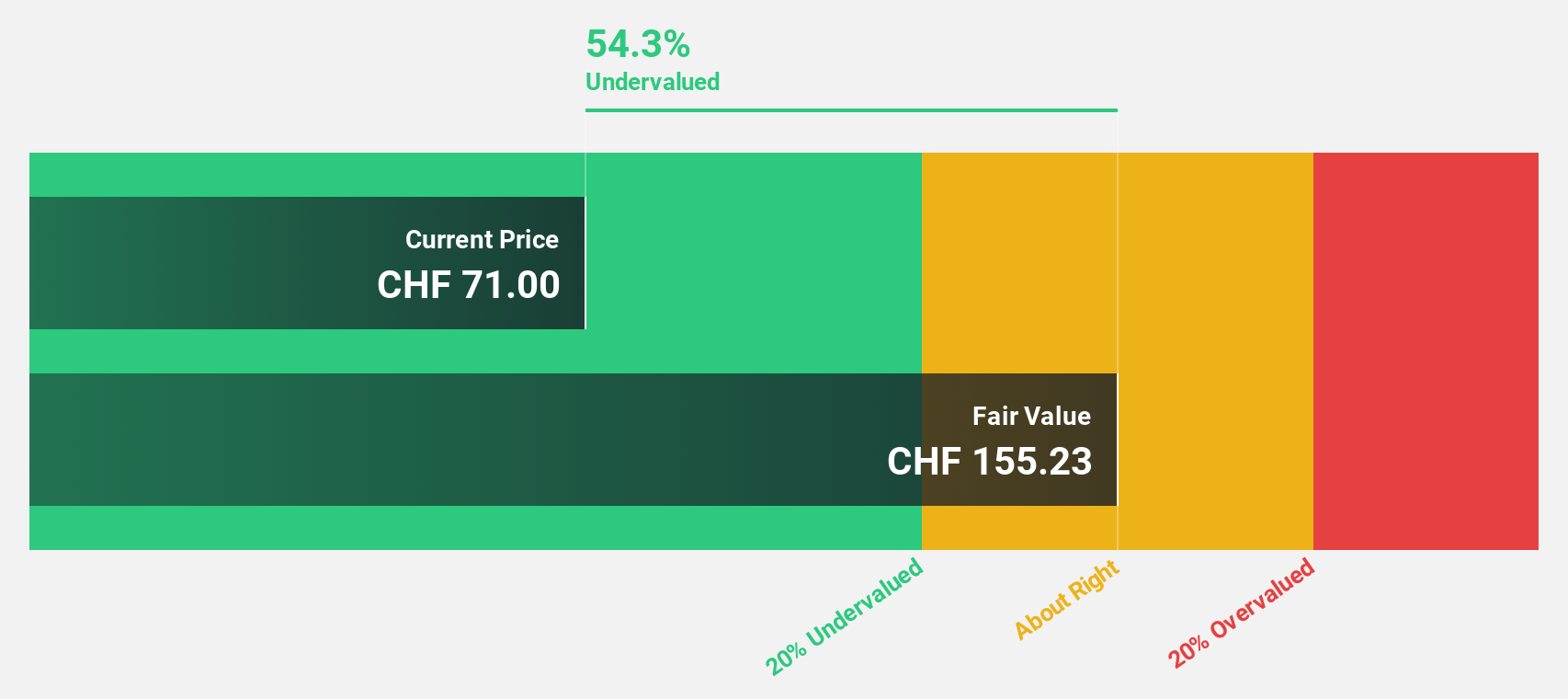

SKAN Group (SWX:SKAN)

Overview: SKAN Group AG, with a market cap of CHF1.67 billion, specializes in providing isolators, cleanroom devices, and decontamination processes for the pharmaceutical and chemical industries across Asia, Europe, the Americas, and internationally.

Operations: The company's revenue is derived from Equipment & Solutions, contributing CHF254.17 million, and Services & Consumables, which account for CHF89.84 million.

Estimated Discount To Fair Value: 16.5%

SKAN Group AG, trading at CHF74.2, is undervalued relative to its estimated fair value of CHF88.91. The company reported a net income increase to CHF38.8 million from CHF26.31 million last year, with earnings per share rising to CHF1.73 from CHF1.17. While revenue growth forecasts are moderate at 16% annually, they outpace the Swiss market's 4.5%. Analysts agree on a potential stock price rise of 22.2%, reflecting positive future prospects despite modest undervaluation based on cash flows.

- According our earnings growth report, there's an indication that SKAN Group might be ready to expand.

- Click here and access our complete balance sheet health report to understand the dynamics of SKAN Group.

Summing It All Up

- Discover the full array of 207 Undervalued European Stocks Based On Cash Flows right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:SKAN

SKAN Group

Provides isolators, cleanroom devices, and decontamination processes for pharmaceutical and chemical industries in Asia, Europe, the Americas, and internationally.

Excellent balance sheet with reasonable growth potential.

Market Insights

Community Narratives