- Switzerland

- /

- Biotech

- /

- SWX:IDIA

Need To Know: Analysts Are Much More Bullish On Idorsia Ltd (VTX:IDIA) Revenues

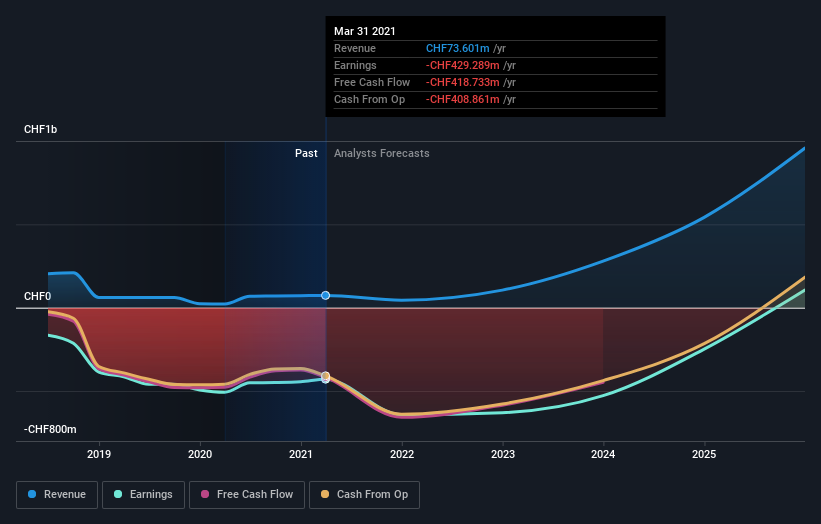

Celebrations may be in order for Idorsia Ltd (VTX:IDIA) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The consensus estimated revenue numbers rose, with their view now clearly much more bullish on the company's business prospects.

Following the latest upgrade, the nine analysts covering Idorsia provided consensus estimates of CHF44m revenue in 2021, which would reflect a disturbing 40% decline on its sales over the past 12 months. Per-share losses are expected to explode, reaching CHF3.84 per share. However, before this estimates update, the consensus had been expecting revenues of CHF34m and CHF3.92 per share in losses. So there's been quite a change-up of views after the recent consensus updates, withthe analysts noticeably increasing their revenue forecasts while also expecting losses per share to hold steady.

See our latest analysis for Idorsia

The consensus price target held steady at CHF30.42 despite the upgrade to revenue forecasts and ongoing losses. Analysts seem to think the business is otherwise performing roughly in line with expectations. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Idorsia at CHF40.00 per share, while the most bearish prices it at CHF19.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. One thing that stands out from these estimates is that revenues are expected to keep falling until the end of 2021, roughly in line with the historical decline of 46% per annum over the past three years. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 23% annually. So while a broad number of companies are forecast to grow, unfortunately Idorsia is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for this year, reflecting increased optimism around Idorsia's prospects. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. Seeing the dramatic upgrade to this year's forecasts, it might be time to take another look at Idorsia.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Idorsia going out to 2025, and you can see them free on our platform here..

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

If you decide to trade Idorsia, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SWX:IDIA

Idorsia

A biopharmaceutical company, engages in the discovery, development, and commercialization of drugs for unmet medical needs in Switzerland.

Moderate and slightly overvalued.