The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Idorsia Ltd (VTX:IDIA) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Idorsia

What Is Idorsia's Net Debt?

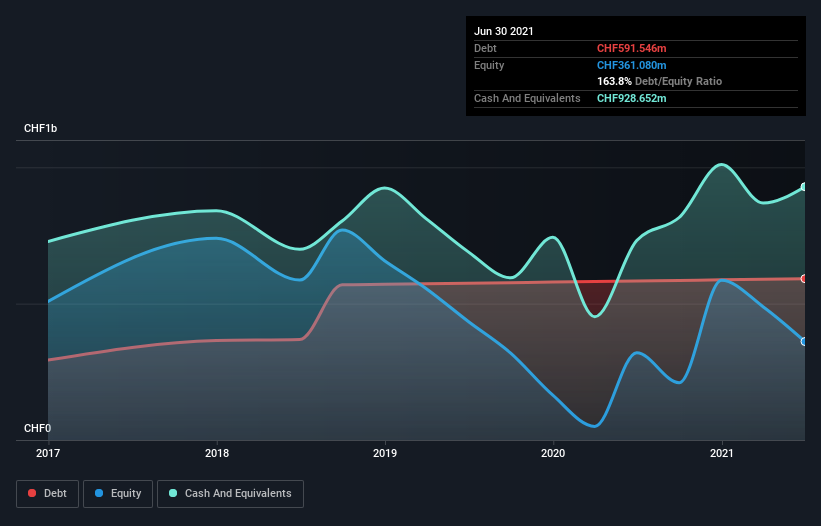

The chart below, which you can click on for greater detail, shows that Idorsia had CHF591.5m in debt in June 2021; about the same as the year before. But on the other hand it also has CHF928.7m in cash, leading to a CHF337.1m net cash position.

How Strong Is Idorsia's Balance Sheet?

The latest balance sheet data shows that Idorsia had liabilities of CHF118.9m due within a year, and liabilities of CHF706.5m falling due after that. Offsetting these obligations, it had cash of CHF928.7m as well as receivables valued at CHF5.59m due within 12 months. So it actually has CHF108.8m more liquid assets than total liabilities.

This surplus suggests that Idorsia has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Idorsia has more cash than debt is arguably a good indication that it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Idorsia can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Idorsia made a loss at the EBIT level, and saw its revenue drop to CHF27m, which is a fall of 60%. That makes us nervous, to say the least.

So How Risky Is Idorsia?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And the fact is that over the last twelve months Idorsia lost money at the earnings before interest and tax (EBIT) line. Indeed, in that time it burnt through CHF513m of cash and made a loss of CHF499m. Given it only has net cash of CHF337.1m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Idorsia you should know about.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you’re looking to trade Idorsia, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SWX:IDIA

Idorsia

A biopharmaceutical company, engages in the discovery, development, and commercialization of drugs for unmet medical needs in Switzerland.

Moderate and slightly overvalued.