- Switzerland

- /

- Healthcare Services

- /

- SWX:SHLTN

Market Cool On SHL Telemedicine Ltd.'s (VTX:SHLTN) Revenues Pushing Shares 27% Lower

Unfortunately for some shareholders, the SHL Telemedicine Ltd. (VTX:SHLTN) share price has dived 27% in the last thirty days, prolonging recent pain. For any long-term shareholders, the last month ends a year to forget by locking in a 77% share price decline.

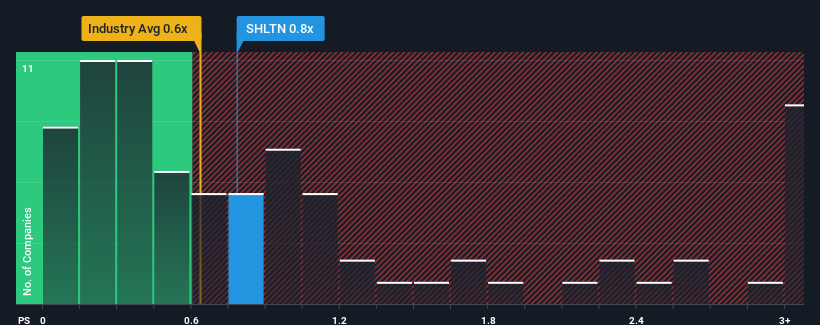

In spite of the heavy fall in price, there still wouldn't be many who think SHL Telemedicine's price-to-sales (or "P/S") ratio of 0.8x is worth a mention when the median P/S in Switzerland's Healthcare industry is similar at about 0.6x. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

See our latest analysis for SHL Telemedicine

How Has SHL Telemedicine Performed Recently?

SHL Telemedicine hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on SHL Telemedicine.Do Revenue Forecasts Match The P/S Ratio?

In order to justify its P/S ratio, SHL Telemedicine would need to produce growth that's similar to the industry.

In reviewing the last year of financials, we were disheartened to see the company's revenues fell to the tune of 2.0%. Even so, admirably revenue has lifted 34% in aggregate from three years ago, notwithstanding the last 12 months. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 22% during the coming year according to the lone analyst following the company. That's shaping up to be materially higher than the 3.7% growth forecast for the broader industry.

With this in consideration, we find it intriguing that SHL Telemedicine's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From SHL Telemedicine's P/S?

Following SHL Telemedicine's share price tumble, its P/S is just clinging on to the industry median P/S. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

Despite enticing revenue growth figures that outpace the industry, SHL Telemedicine's P/S isn't quite what we'd expect. When we see a strong revenue outlook, with growth outpacing the industry, we can only assume potential uncertainty around these figures are what might be placing slight pressure on the P/S ratio. However, if you agree with the analysts' forecasts, you may be able to pick up the stock at an attractive price.

Plus, you should also learn about these 3 warning signs we've spotted with SHL Telemedicine (including 1 which is significant).

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:SHLTN

SHL Telemedicine

Engages in the provision of telemedicine services in Israel, Europe, and internationally.

Excellent balance sheet low.

Similar Companies

Market Insights

Community Narratives