- Switzerland

- /

- Luxury

- /

- SWX:UHR

Assessing Swatch Group (SWX:UHR)’s Valuation as Italian Regulators Probe Alleged Price-Fixing Practices

Reviewed by Simply Wall St

Italian regulators have opened a competition probe into Swatch Group (SWX:UHR) over alleged price fixing with online distributors, putting fresh attention on how the Swiss watchmaker’s pricing power and margins might evolve from here.

See our latest analysis for Swatch Group.

The regulatory probe lands at a delicate moment for investors, with Swatch Group’s share price at CHF 161.85 after a weak recent stretch that includes a 1 month share price return of minus 8.4 percent. This sits alongside a stronger 3 month share price return of 8.26 percent, which contrasts with a more muted 1 year total shareholder return of just 0.97 percent and still deeply negative 3 year and 5 year total shareholder returns. Taken together, this suggests that while short term momentum is trying to turn, the longer term recovery story is far from assured.

If this kind of regulatory risk has you reassessing your watchlist, it might be worth scanning fast growing stocks with high insider ownership for other companies where insiders are heavily aligned with future growth.

With profits rebounding but the share price still lagging long term, has Swatch quietly become a contrarian value play, or are investors already correctly discounting regulatory risk and muted growth expectations?

Price-to-Earnings of 139.6x: Is it justified?

Swatch Group is trading on a Price to Earnings ratio of 139.6 times, which looks stretched against its CHF 161.85 last close and peer valuations.

The price to earnings multiple compares the current share price to earnings per share and is a common yardstick for established, profitable consumer brands. For Swatch, such an elevated P E suggests investors are either looking through current depressed profits or paying up aggressively for an earnings rebound.

Relative to both the European luxury average P E of 20.3 times and the sector peer average of 18.8 times, Swatch’s 139.6 times earnings looks extremely rich. It also trades far above the estimated fair P E of 45.1 times, implying a large premium that the market may eventually re rate closer to that fair ratio as earnings and sentiment normalize.

Explore the SWS fair ratio for Swatch Group

Result: Price-to-Earnings of 139.6x (OVERVALUED)

However, regulatory pressure and a share price already trading well above analyst targets could quickly puncture any contrarian value thesis around Swatch.

Find out about the key risks to this Swatch Group narrative.

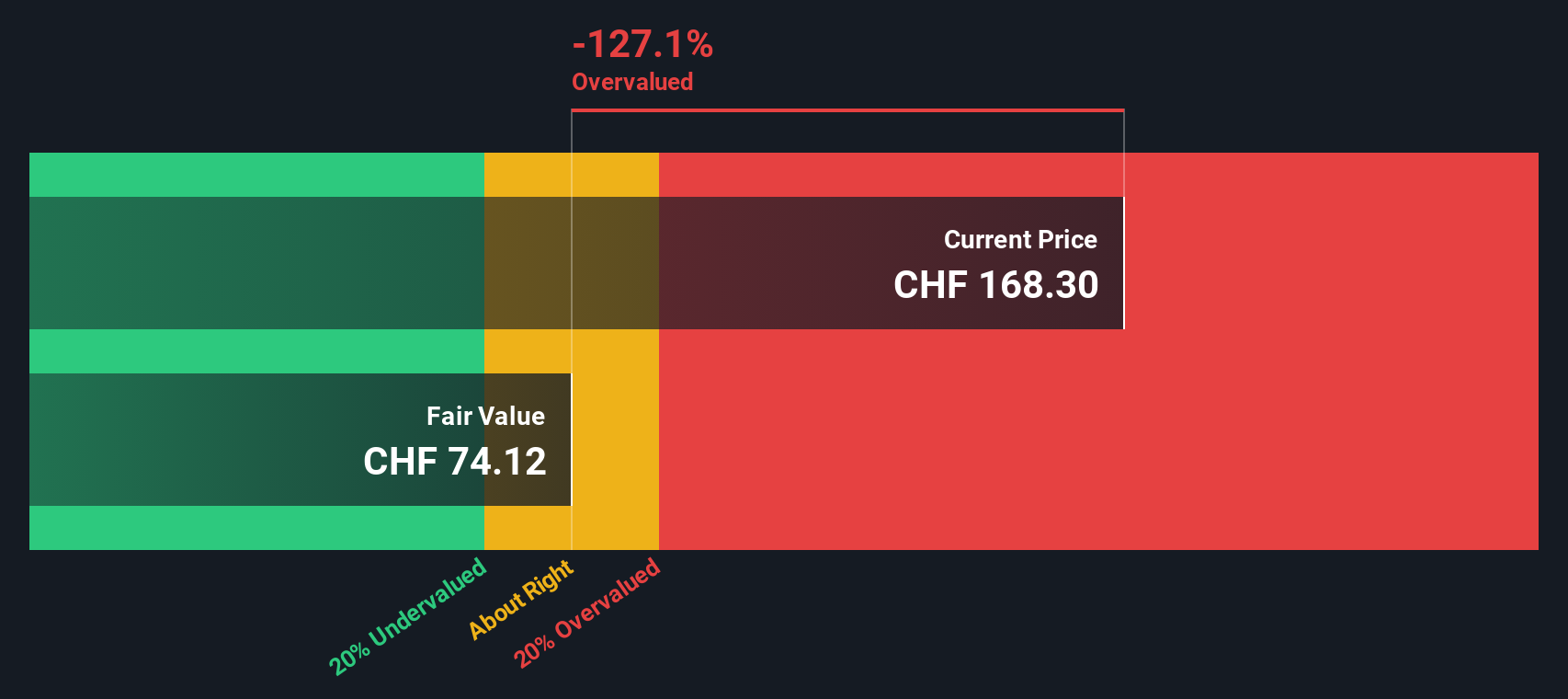

Another View on Value

Our DCF model paints a very different picture to the rich 139.6 times earnings multiple, suggesting fair value closer to CHF 74.14 per share, well below the current CHF 161.85. If both are using reasonable assumptions, which signal should investors trust more: sentiment or cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Swatch Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 909 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Swatch Group Narrative

Whether you see Swatch differently or simply want to examine the numbers yourself, you can build a complete view in under three minutes, Do it your way.

A great starting point for your Swatch Group research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop at one watchmaker. Use Simply Wall Street’s powerful Screener to uncover fresh opportunities before the crowd and position your capital where growth is building.

- Capitalize on mispriced quality by scanning these 909 undervalued stocks based on cash flows that combine strong cash flows with attractive entry points.

- Ride the wave of intelligent automation as you target these 25 AI penny stocks positioned to benefit from rapid adoption across industries.

- Lock in recurring income potential by reviewing these 12 dividend stocks with yields > 3% offering yields that can strengthen your portfolio’s long term returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:UHR

Swatch Group

Designs, manufactures, and sells finished watches, jewelry, and watch movements and components in Switzerland, rest of Europe, Greater China, rest of Asia, America, Oceania, and Africa.

Flawless balance sheet with reasonable growth potential.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026