- Switzerland

- /

- Building

- /

- SWX:DOKA

Has dormakaba Holding (VTX:DOKA) Got What It Takes To Become A Multi-Bagger?

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Ideally, a business will show two trends; firstly a growing return on capital employed (ROCE) and secondly, an increasing amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So while dormakaba Holding (VTX:DOKA) has a high ROCE right now, lets see what we can decipher from how returns are changing.

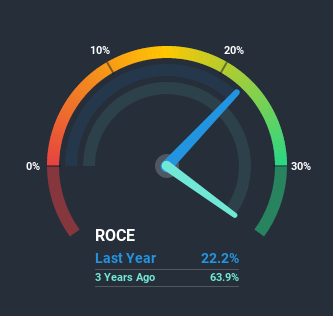

What is Return On Capital Employed (ROCE)?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on dormakaba Holding is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.22 = CHF253m ÷ (CHF1.8b - CHF670m) (Based on the trailing twelve months to June 2020).

Therefore, dormakaba Holding has an ROCE of 22%. In absolute terms that's a great return and it's even better than the Building industry average of 13%.

Check out our latest analysis for dormakaba Holding

In the above chart we have measured dormakaba Holding's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

So How Is dormakaba Holding's ROCE Trending?

When we looked at the ROCE trend at dormakaba Holding, we didn't gain much confidence. While it's comforting that the ROCE is high, five years ago it was 29%. Meanwhile, the business is utilizing more capital but this hasn't moved the needle much in terms of sales in the past 12 months, so this could reflect longer term investments. It may take some time before the company starts to see any change in earnings from these investments.

The Bottom Line On dormakaba Holding's ROCE

Bringing it all together, while we're somewhat encouraged by dormakaba Holding's reinvestment in its own business, we're aware that returns are shrinking. And investors appear hesitant that the trends will pick up because the stock has fallen 23% in the last five years. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

If you want to continue researching dormakaba Holding, you might be interested to know about the 2 warning signs that our analysis has discovered.

dormakaba Holding is not the only stock earning high returns. If you'd like to see more, check out our free list of companies earning high returns on equity with solid fundamentals.

When trading dormakaba Holding or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About SWX:DOKA

Excellent balance sheet with reasonable growth potential.