Advertisement

- Switzerland

- /

- Banks

- /

- SWX:BCVN

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For Banque Cantonale Vaudoise's (VTX:BCVN) CEO For Now

Key Insights

- Banque Cantonale Vaudoise will host its Annual General Meeting on 25th of April

- Salary of CHF960.0k is part of CEO Pascal Kiener's total remuneration

- Total compensation is 95% above industry average

- Banque Cantonale Vaudoise's EPS grew by 12% over the past three years while total shareholder return over the past three years was 22%

CEO Pascal Kiener has done a decent job of delivering relatively good performance at Banque Cantonale Vaudoise (VTX:BCVN) recently. As shareholders go into the upcoming AGM on 25th of April, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for Banque Cantonale Vaudoise

Comparing Banque Cantonale Vaudoise's CEO Compensation With The Industry

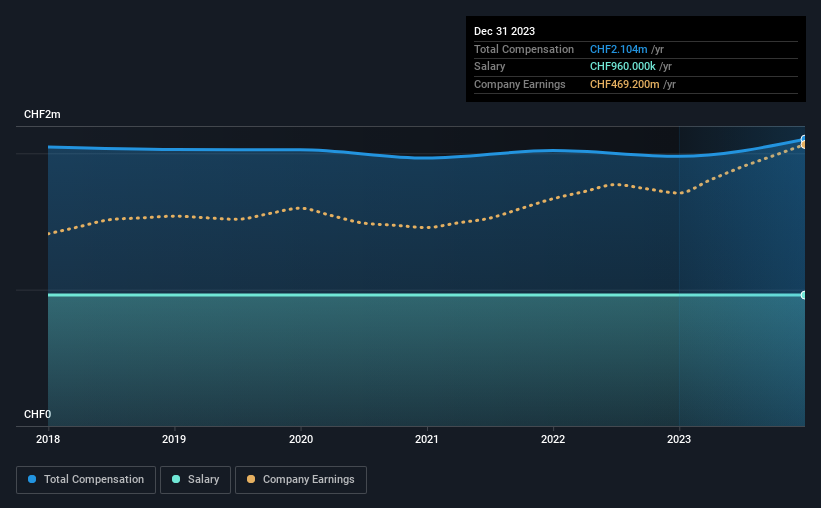

At the time of writing, our data shows that Banque Cantonale Vaudoise has a market capitalization of CHF8.6b, and reported total annual CEO compensation of CHF2.1m for the year to December 2023. That's a fairly small increase of 6.4% over the previous year. While we always look at total compensation first, our analysis shows that the salary component is less, at CHF960k.

In comparison with other companies in the Swiss Banks industry with market capitalizations ranging from CHF3.6b to CHF11b, the reported median CEO total compensation was CHF1.1m. Hence, we can conclude that Pascal Kiener is remunerated higher than the industry median. Moreover, Pascal Kiener also holds CHF2.7m worth of Banque Cantonale Vaudoise stock directly under their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CHF960k | CHF960k | 46% |

| Other | CHF1.1m | CHF1.0m | 54% |

| Total Compensation | CHF2.1m | CHF2.0m | 100% |

On an industry level, around 46% of total compensation represents salary and 54% is other remuneration. Our data reveals that Banque Cantonale Vaudoise allocates salary more or less in line with the wider market. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Banque Cantonale Vaudoise's Growth Numbers

Over the past three years, Banque Cantonale Vaudoise has seen its earnings per share (EPS) grow by 12% per year. In the last year, its revenue is up 12%.

Shareholders would be glad to know that the company has improved itself over the last few years. It's a real positive to see this sort of revenue growth in a single year. That suggests a healthy and growing business. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Banque Cantonale Vaudoise Been A Good Investment?

Banque Cantonale Vaudoise has generated a total shareholder return of 22% over three years, so most shareholders would be reasonably content. But they probably don't want to see the CEO paid more than is normal for companies around the same size.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

If you think CEO compensation levels are interesting you will probably really like this free visualization of insider trading at Banque Cantonale Vaudoise.

Switching gears from Banque Cantonale Vaudoise, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Banque Cantonale Vaudoise might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:BCVN

Banque Cantonale Vaudoise

Engages in the provision of various financial services in Vaud Canton and rest of Switzerland, the European Union, North America, and internationally.

6 star dividend payer with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor