Advertisement

Analysts Expect Intermap Technologies Corporation (TSE:IMP) To Breakeven Soon

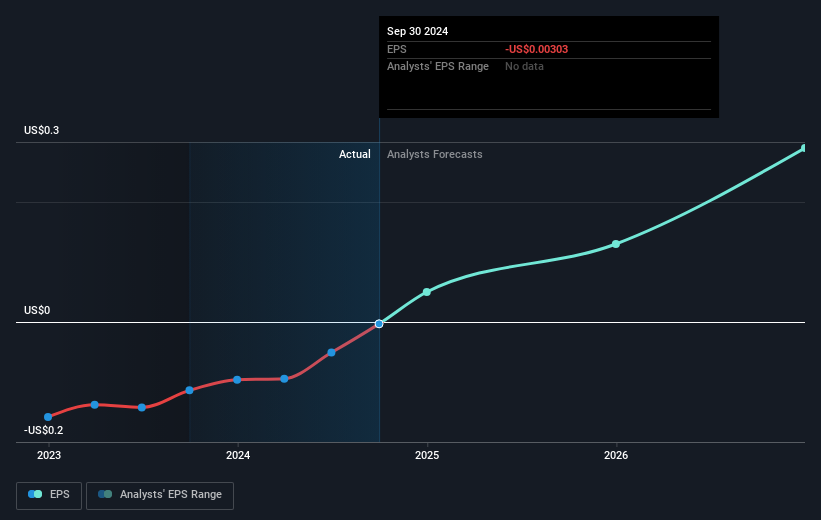

We feel now is a pretty good time to analyse Intermap Technologies Corporation's (TSE:IMP) business as it appears the company may be on the cusp of a considerable accomplishment. Intermap Technologies Corporation, a geospatial intelligence company, provides various geospatial solutions and analytics in the United States, Canada, the Asia Pacific, and Europe. The CA$108m market-cap company posted a loss in its most recent financial year of US$3.7m and a latest trailing-twelve-month loss of US$130k shrinking the gap between loss and breakeven. Many investors are wondering about the rate at which Intermap Technologies will turn a profit, with the big question being “when will the company breakeven?” We've put together a brief outline of industry analyst expectations for the company, its year of breakeven and its implied growth rate.

Intermap Technologies is bordering on breakeven, according to some Canadian Software analysts. They expect the company to post a final loss in 2024, before turning a profit of US$8.6m in 2025. Therefore, the company is expected to breakeven roughly a year from now or less! How fast will the company have to grow to reach the consensus forecasts that anticipate breakeven by 2025? Working backwards from analyst estimates, it turns out that they expect the company to grow 111% year-on-year, on average, which signals high confidence from analysts. Should the business grow at a slower rate, it will become profitable at a later date than expected.

Given this is a high-level overview, we won’t go into details of Intermap Technologies' upcoming projects, however, take into account that generally a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

Check out our latest analysis for Intermap Technologies

One thing we would like to bring into light with Intermap Technologies is its debt-to-equity ratio of over 2x. Generally, the rule of thumb is debt shouldn’t exceed 40% of your equity, which in this case, the company has significantly overshot. Note that a higher debt obligation increases the risk in investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on Intermap Technologies, so if you are interested in understanding the company at a deeper level, take a look at Intermap Technologies' company page on Simply Wall St. We've also compiled a list of relevant factors you should further research:

- Valuation: What is Intermap Technologies worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Intermap Technologies is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Intermap Technologies’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:IMP

Intermap Technologies

A geospatial intelligence company, provides various geospatial solutions and analytics in the United States, the Asia Pacific, and Europe.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0775.1% undervalued

139 followersusers have followed this narrative

1 commentusers have commented on this narrative

22 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

KO

Kouj on CSL ·

CSL: The Dip Is the Opportunity

Fair Value:AU$1559.3% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

GA

GavrielH on DHT Holdings ·

DHT Holdings, inc: Strait of Hormuz Risk Amidst US-Israel vs Iran Tensions Spikes VLCC Rates.

Fair Value:US$3653.2% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

Recently Updated Narratives

MD

mdebaugh14 on ManpowerGroup ·

Consensus has confused a cyclical trough for a structural decline

Fair Value:US$45.1942.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on Eagle Plains Resources ·

A Case For Eagle Plains Resources CAD$ 2.50 (base case) - CAD$ 5.00 (bull case)

Fair Value:CA$2.591.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MD

mdebaugh14 on Bath & Body Works ·

Bath & Body Works is a dominant, high-quality consumer brand with near-perfect business economics, temporarily depressed by a demand trough

Fair Value:US$37.0547.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.378.4% undervalued

53 followersusers have followed this narrative

3 commentsusers have commented on this narrative

29 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9822.7% undervalued

44 followersusers have followed this narrative

0 commentsusers have commented on this narrative

33 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59633.6% undervalued

1310 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

Trending Discussion

DA

daqui_luis on Corticeira Amorim S.G.P.S ·

Great analysis on a great and solid company with a dominant position in the Cork Market.

1

|0