Advertisement

CGI Valuation After Share Price Pullback and New Digital Transformation Contracts

Reviewed by Bailey Pemberton

- If you have been wondering whether CGI is quietly turning into a value opportunity after a rough stretch, you are not alone. That is exactly what we are going to unpack.

- The stock is up 2.6% over the last week and 1.2% over the last month, but it still sits around 18.9% lower year to date and 19.7% below where it was a year ago, despite posting 3 year and 5 year gains of 10.6% and 33.1%.

- Recent headlines have focused on CGI expanding its digital transformation and IT services footprint through new contracts and partnerships, reinforcing its role as a long term tech infrastructure partner for governments and enterprises. Investors are weighing whether this contract momentum is enough to justify a re rating after the share price pullback.

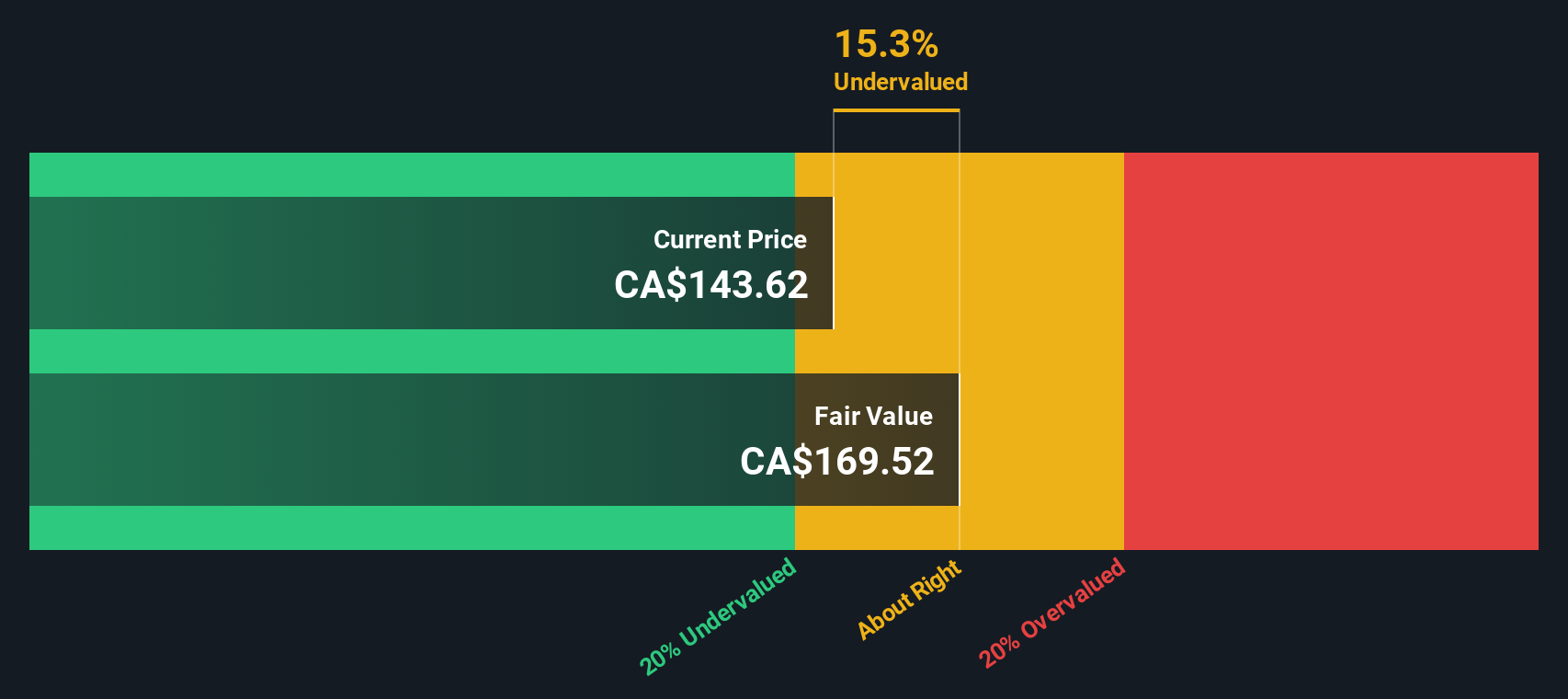

- On our valuation checks CGI scores a 5 out of 6 on being undervalued. You can see the breakdown in this valuation score, which sets the stage for comparing different valuation methods and then circling back at the end to another way to think about what the stock may be worth.

Approach 1: CGI Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting its future cash flows and then discounting those projections back to today in CA$ terms.

For CGI, the latest twelve month Free Cash Flow is about CA$1.83 billion. Analysts provide detailed forecasts for the next few years, and beyond that Simply Wall St extrapolates the trend to build a longer runway for the model. Under this two stage Free Cash Flow to Equity approach, CGI is projected to be generating roughly CA$2.21 billion in Free Cash Flow in 10 years time, reflecting steady but not explosive growth as the business matures.

When all those projected cash flows are discounted back to today, the model arrives at an intrinsic value of about CA$148.05 per share. Compared with the current share price, this implies the stock is trading at roughly a 13.7% discount, indicating that investors may not be fully pricing in CGI’s future cash generation.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CGI is undervalued by 13.7%. Track this in your watchlist or portfolio, or discover 906 more undervalued stocks based on cash flows.

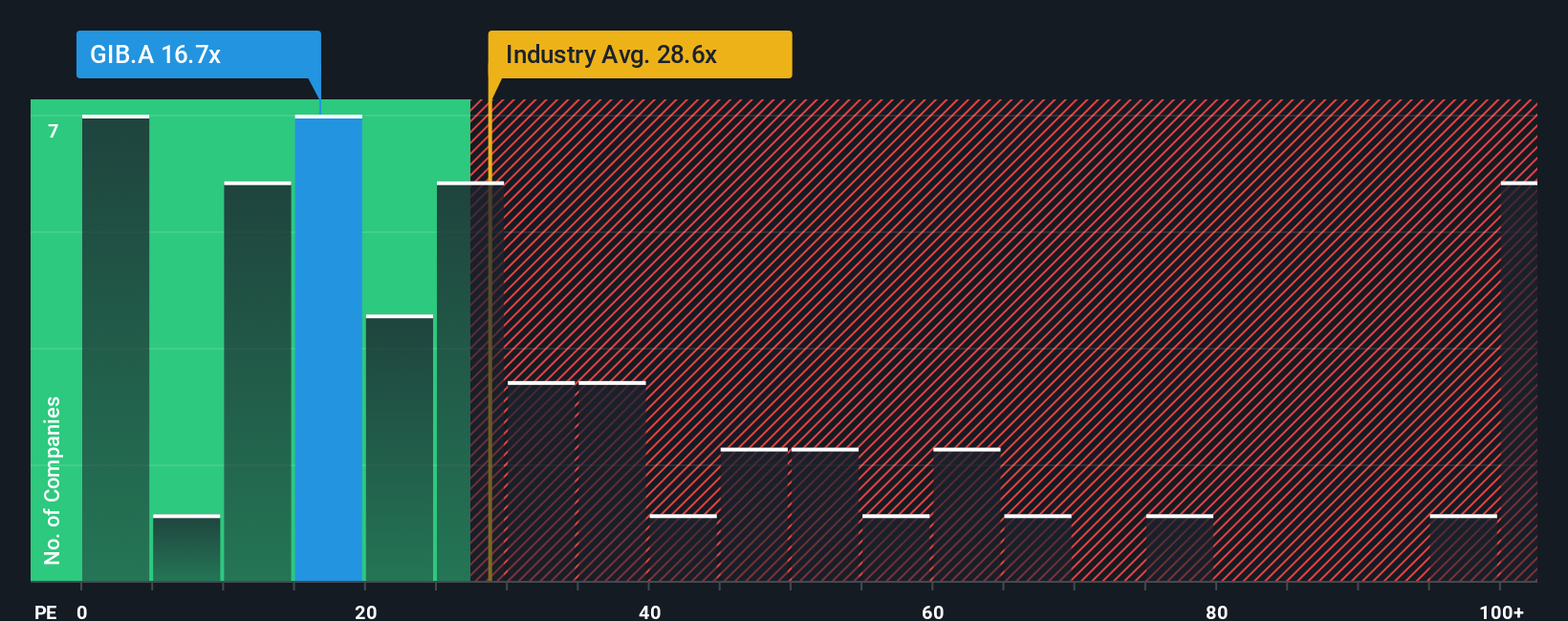

Approach 2: CGI Price vs Earnings

For a consistently profitable business like CGI, the Price to Earnings (PE) ratio is a useful way to gauge how much investors are willing to pay for each dollar of current earnings. In general, companies with stronger growth prospects and lower perceived risk can justify a higher PE, while slower-growing or riskier firms tend to trade on lower multiples.

CGI currently trades on a PE of about 16.7x, which sits below the broader IT industry average of roughly 21.4x and well under the approximate 44.6x multiple seen across its peer group. Simply Wall St also calculates a proprietary Fair Ratio of around 29.4x for CGI, which is the PE level that would be expected given its earnings growth outlook, profitability, industry, market cap and specific risk profile.

This Fair Ratio goes a step beyond simple peer or industry comparisons because it adjusts for the company’s own fundamentals rather than assuming that all IT stocks deserve the same multiple. With CGI trading at 16.7x versus a Fair Ratio of 29.4x, the shares appear meaningfully undervalued on an earnings-based view.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your CGI Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you attach your own story about CGI’s future to concrete numbers like revenue growth, margins, earnings and fair value. You can then compare that Fair Value with today’s Price to decide whether to buy, hold or sell. The Narrative automatically refreshes as new news or earnings land. For example, one investor might build a bullish CGI Narrative around accelerating AI adoption, rising margins and a fair value closer to CA$185. Another might focus on macro and integration risks, slower growth and a fair value nearer CA$137. By seeing these different, dynamically updated perspectives side by side, you can quickly judge which story and valuation best matches your own view and risk tolerance.

Do you think there's more to the story for CGI? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:GIB.A

CGI

Provides information technology and business process services in Western and Southern Europe, the United States, Canada, Scandinavia, Northwest and Central-East Europe, the United Kingdom, Australia, Germany, Finland, Poland, Baltics, and the Asia Pacific.

Very undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$471.5% undervalued

41 followersusers have followed this narrative

0 commentsusers have commented on this narrative

9 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17037.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38032.7% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7442.9% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

Recently Updated Narratives

DC

DCA_rules on Micron Technology ·

Micron Technology (MU): Riding the AI Supercycle to a $100B+ Revenue Horizon and Historic 40%+ Net Profit Margins

Fair Value:US$1.25k17.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AS

AstrisCorporateAdvisory on Aoyama Zaisan Networks CompanyLimited ·

Preparing for re-acceleration in FY12/27

Fair Value:JP¥1.31k0.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Freegold Ventures ·

Freegold Ventures, Eric Sprott is Betting Big on This 31 Moz Alaska Gold Beast

Fair Value:CA$33.0196.4% undervalued

15 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.2% undervalued

122 followersusers have followed this narrative

2 commentsusers have commented on this narrative

35 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9718.0% undervalued

56 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1926.1% undervalued

45 followersusers have followed this narrative

0 commentsusers have commented on this narrative

18 likesusers have liked this narrative