Advertisement

The Canadian stock market has been experiencing a robust year, with the TSX up over 17%, reflecting a growing economy and favorable central bank policies. In this thriving environment, growth companies with high insider ownership stand out as they often indicate strong confidence from those who know the business best, potentially aligning well with ongoing market trends.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Vox Royalty (TSX:VOXR) | 11.8% | 70.7% |

| Almonty Industries (TSX:AII) | 17.7% | 117.6% |

| goeasy (TSX:GSY) | 21.2% | 16.6% |

| Alvopetro Energy (TSXV:ALV) | 19.4% | 76.5% |

| VersaBank (TSX:VBNK) | 13.3% | 30.4% |

| Aya Gold & Silver (TSX:AYA) | 10.2% | 71.4% |

| Aritzia (TSX:ATZ) | 18.9% | 59.7% |

| Ivanhoe Mines (TSX:IVN) | 12.3% | 69.8% |

| Allied Gold (TSX:AAUC) | 17.7% | 70.7% |

| Medicenna Therapeutics (TSX:MDNA) | 15.3% | 57.2% |

Let's explore several standout options from the results in the screener.

Allied Gold (TSX:AAUC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Allied Gold Corporation, along with its subsidiaries, is involved in the exploration and production of mineral deposits in Africa and has a market cap of CA$1.30 billion.

Operations: The company's revenue segments include $142.03 million from the Agbaou Mine, $193.93 million from the Bonikro Mine, and $391.07 million from the Sadiola Mine.

Insider Ownership: 17.7%

Earnings Growth Forecast: 70.7% p.a.

Allied Gold Corporation has demonstrated significant insider confidence, with substantial insider buying over the past three months. The company's revenue is forecast to grow at 20.2% annually, outpacing the Canadian market's growth rate. Despite recent shareholder dilution, Allied Gold is trading at a good value relative to peers and industry standards. Recent developments include a CAD 192.2 million follow-on equity offering and an ambitious expansion of the Sadiola Gold Mine, indicating strategic growth initiatives underway.

- Navigate through the intricacies of Allied Gold with our comprehensive analyst estimates report here.

- The analysis detailed in our Allied Gold valuation report hints at an deflated share price compared to its estimated value.

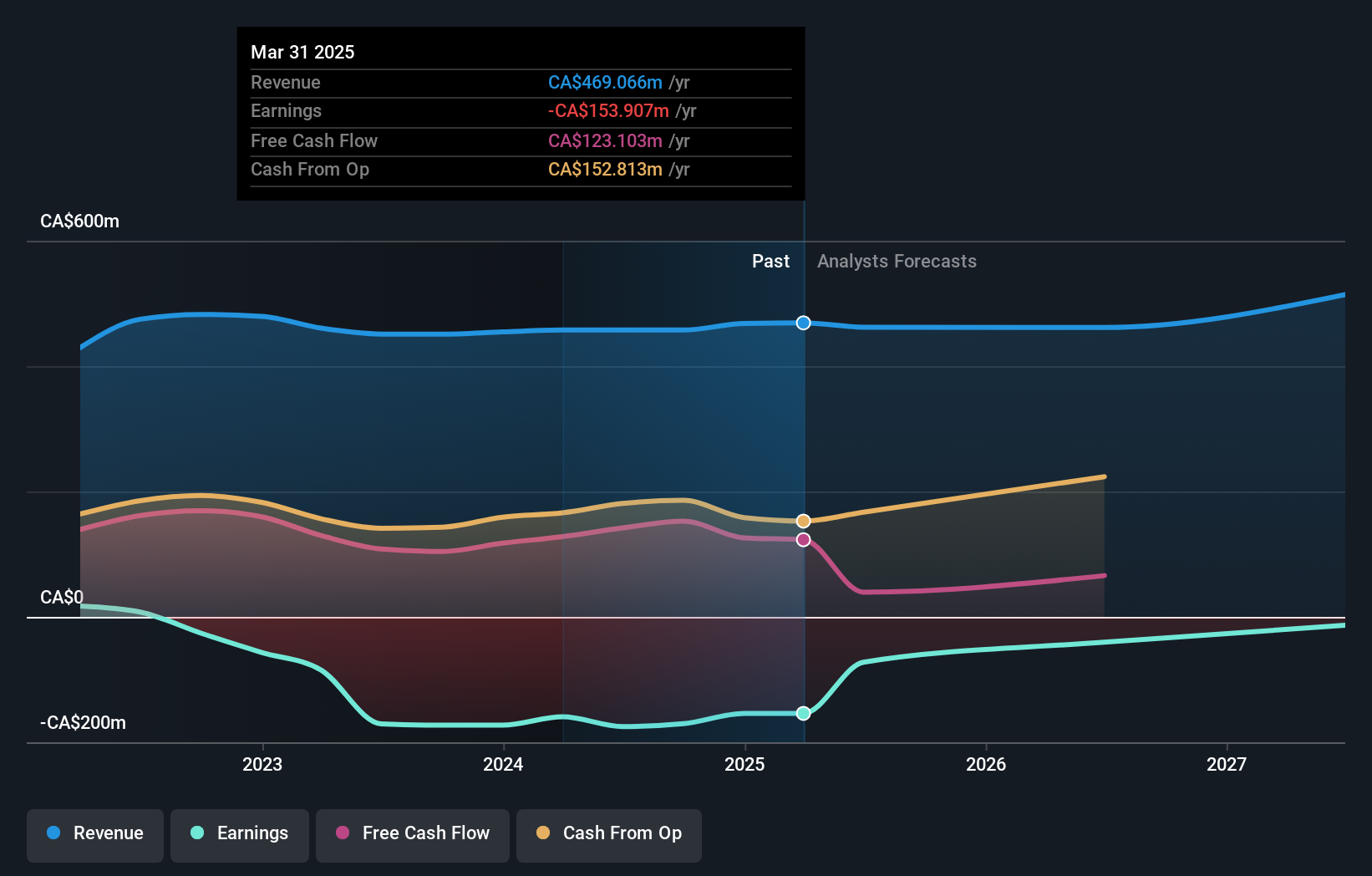

Colliers International Group (TSX:CIGI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Colliers International Group Inc. offers commercial real estate and investment management services to corporate and institutional clients across various regions, with a market cap of CA$10.33 billion.

Operations: The company's revenue is derived from several segments: Americas ($2.59 billion), Asia Pacific ($614.55 million), Investment Management ($496.42 million), and Europe, Middle East & Africa (EMEA) ($734.93 million).

Insider Ownership: 14.1%

Earnings Growth Forecast: 20.8% p.a.

Colliers International Group showcases insider confidence with more shares bought than sold recently. The company reported a significant turnaround in profitability, with net income of US$36.72 million in Q2 2024 compared to a loss the previous year. Revenue growth is projected at 10.4% annually, surpassing the Canadian market average of 7.3%. However, shareholders experienced dilution over the past year, and debt coverage remains an area for improvement despite robust earnings forecasts.

- Click to explore a detailed breakdown of our findings in Colliers International Group's earnings growth report.

- Upon reviewing our latest valuation report, Colliers International Group's share price might be too optimistic.

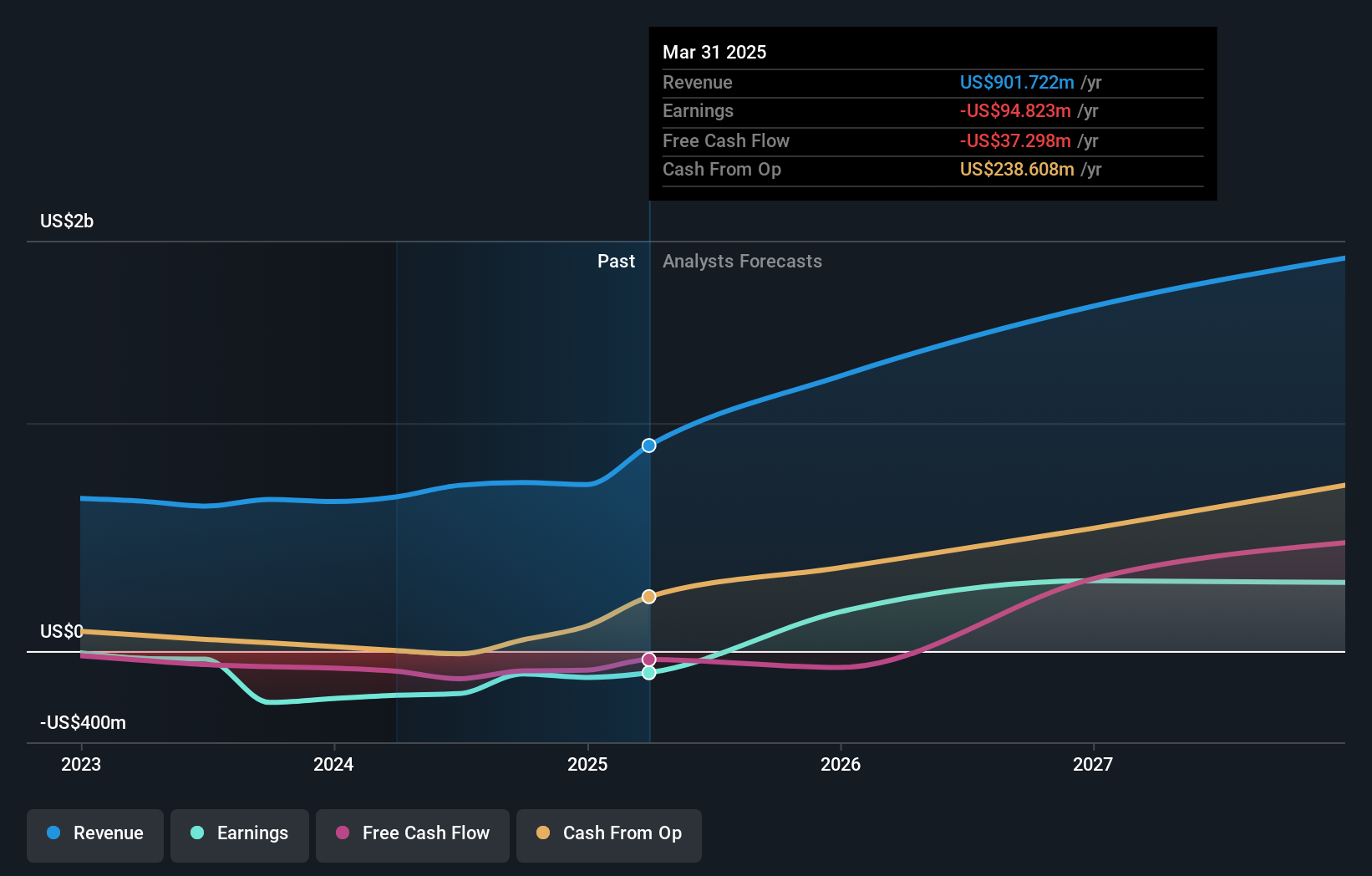

Dye & Durham (TSX:DND)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dye & Durham Limited offers cloud-based software and technology solutions for law firms, financial service institutions, sole-practitioner law firms, and government organizations across Canada, Australia, South Africa, Ireland, and the United Kingdom with a market cap of CA$1.29 billion.

Operations: The company generates revenue of CA$457.70 million from its Internet Software & Services segment.

Insider Ownership: 14.9%

Earnings Growth Forecast: 121.3% p.a.

Dye & Durham is navigating a complex landscape with activist shareholders challenging its leadership and strategic direction. Despite this, the company is forecasted to achieve profitability within three years, exceeding market growth expectations. Trading at 23.8% below estimated fair value and at a lower EBITDA multiple compared to peers, it presents potential upside if management issues are resolved. However, past shareholder dilution and ongoing activist pressures highlight governance concerns that may impact future performance.

- Click here to discover the nuances of Dye & Durham with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Dye & Durham is trading behind its estimated value.

Where To Now?

- Discover the full array of 35 Fast Growing TSX Companies With High Insider Ownership right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:DND

Dye & Durham

Provides cloud-based software and technology solutions for law firms, financial service institutions, sole-practitioner law firms, and government organizations in Canada, Australia, South Africa, Ireland, and the United Kingdom.

Good value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor