Advertisement

Assessing Computer Modelling Group (TSX:CMG) Valuation After Board Refresh And Softer Earnings

Computer Modelling Group (TSX:CMG) is back on investors’ radar after a fresh board appointment in Christopher Wright. This was released alongside third quarter results that showed lower revenue and earnings and a reiterated focus on recurring revenue growth.

See our latest analysis for Computer Modelling Group.

Those earnings and dividend updates have landed against a weak price backdrop, with a 7 day share price return of 14.56% and a 30 day share price return of 20.90%. At the same time, the 1 year total shareholder return of 51.82% and 5 year total shareholder return of 25.47% point to pressure that recent board changes and recurring revenue plans may be trying to address.

If the recent board appointment has you thinking about where software and energy intersect, it could be worth scanning our list of 58 profitable AI stocks that aren't just burning cash for other ideas in this space.

With CMG’s share price under pressure, recent revenue softness, and a new director focused on growth, the key question is whether today’s valuation reflects only these headwinds or if markets are already pricing in future recovery.

Preferred P/E of 19x: Is it justified?

At a last close of CA$4.05, CMG trades on a P/E of 19x, which looks expensive relative to its direct peers but cheaper than the broader Canadian software group.

The P/E multiple compares the share price to earnings per share and is one of the quickest ways to see how much investors are paying for each dollar of profit. For a software and consulting business like CMG, where cash flow quality and recurring revenue matter a lot, the P/E provides a shorthand view of how the market is weighing those characteristics against current earnings.

Here, the tension is clear. CMG is described as expensive versus a specific peer set where the average P/E sits at 14.2x, yet it is described as better value versus the wider Canadian software industry average of 35x and also versus an estimated fair P/E of 24.9x. That indicates the market is not assigning a premium multiple, even though the company scores 5 out of 6 on valuation checks.

Explore the SWS fair ratio for Computer Modelling Group

Result: Price-to-Earnings of 19x (UNDERVALUED)

However, recent total shareholder returns over 1, 3 and 5 years, along with softer quarterly revenue and earnings, suggest sentiment could stay fragile if operational progress stalls.

Find out about the key risks to this Computer Modelling Group narrative.

Another view from the SWS DCF model

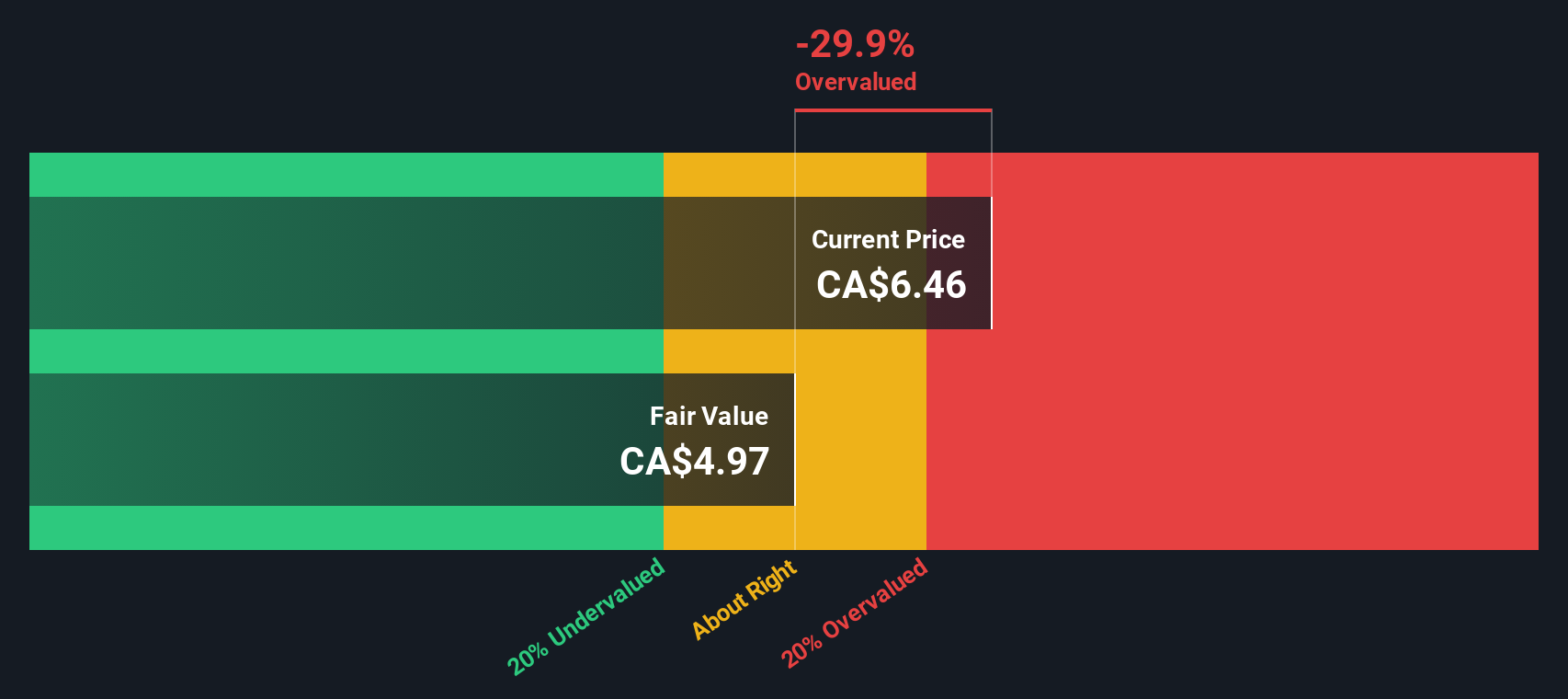

The P/E of 19x paints CMG as relatively cheap next to the broader Canadian software group, but our DCF model offers a stronger challenge. On that basis, CA$4.05 sits about 25% below an estimated fair value of CA$5.40, which hints at a wider potential gap. Could the market be underestimating future cash flows?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Computer Modelling Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 5 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Computer Modelling Group Narrative

If you see the numbers differently or prefer to stress test the assumptions yourself, you can build a custom view of CMG in just a few minutes, starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Computer Modelling Group.

Looking for more investment ideas?

If CMG has sharpened your thinking, do not stop here. Broaden your watchlist with a few focused ideas that match the kind of portfolio you want to build.

- Start with resilience and look at companies on our 7 resilient stocks with low risk scores to see which names currently score well on overall risk.

- Hunt for potential value by scanning the 5 high quality undervalued stocks and see which companies currently pair quality fundamentals with prices that may look appealing.

- Build a cash flow focused watchlist by reviewing our 7 dividend fortresses and see which companies are currently offering higher yields.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CMG

Computer Modelling Group

A software and consulting technology company, engages in the development and licensing of reservoir simulation and seismic interpretation software and related services.

Very undervalued with excellent balance sheet.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.557.6% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$56054.5% undervalued

61 followersusers have followed this narrative

4 commentsusers have commented on this narrative

29 likesusers have liked this narrative

TA

Talos on MindWalk Holdings ·

The Asymmetric TechBio Play: MindWalk Holdings and the Valuation Disconnect

Fair Value:US$8.2781.6% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

AntonioS on CAR Group ·

CAR Group. A wonderful compounding franchise at a fair-not-cheap price.

Fair Value:AU$3219.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GA

GaryB on Palantir Technologies ·

Palantir hits 52 week low.

Fair Value:US$274.861.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

North49_ on iShares - iShares MSCI South Korea ETF ·

EWY:US NYSE Arca iShares Msci South Korea ETF, an opportunity to diversify your tech investments.

Fair Value:US$273.4525.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.6% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

18 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7445.2% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75034.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

7 likesusers have liked this narrative