- Canada

- /

- Industrial REITs

- /

- TSX:NXR.UN

Exploring 3 Undervalued Small Caps On TSX With Insider Activity In Canada

Reviewed by Simply Wall St

The Canadian market has been navigating a period of economic moderation, with inflation rates stabilizing and the TSX showing modest gains of 3% this year. In this environment, small-cap stocks can offer unique opportunities for investors seeking growth potential, particularly when insider activity signals confidence in a company's prospects.

Top 10 Undervalued Small Caps With Insider Buying In Canada

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| First National Financial | 13.5x | 3.8x | 44.04% | ★★★★★☆ |

| Boston Pizza Royalties Income Fund | 11.8x | 7.6x | 34.06% | ★★★★★☆ |

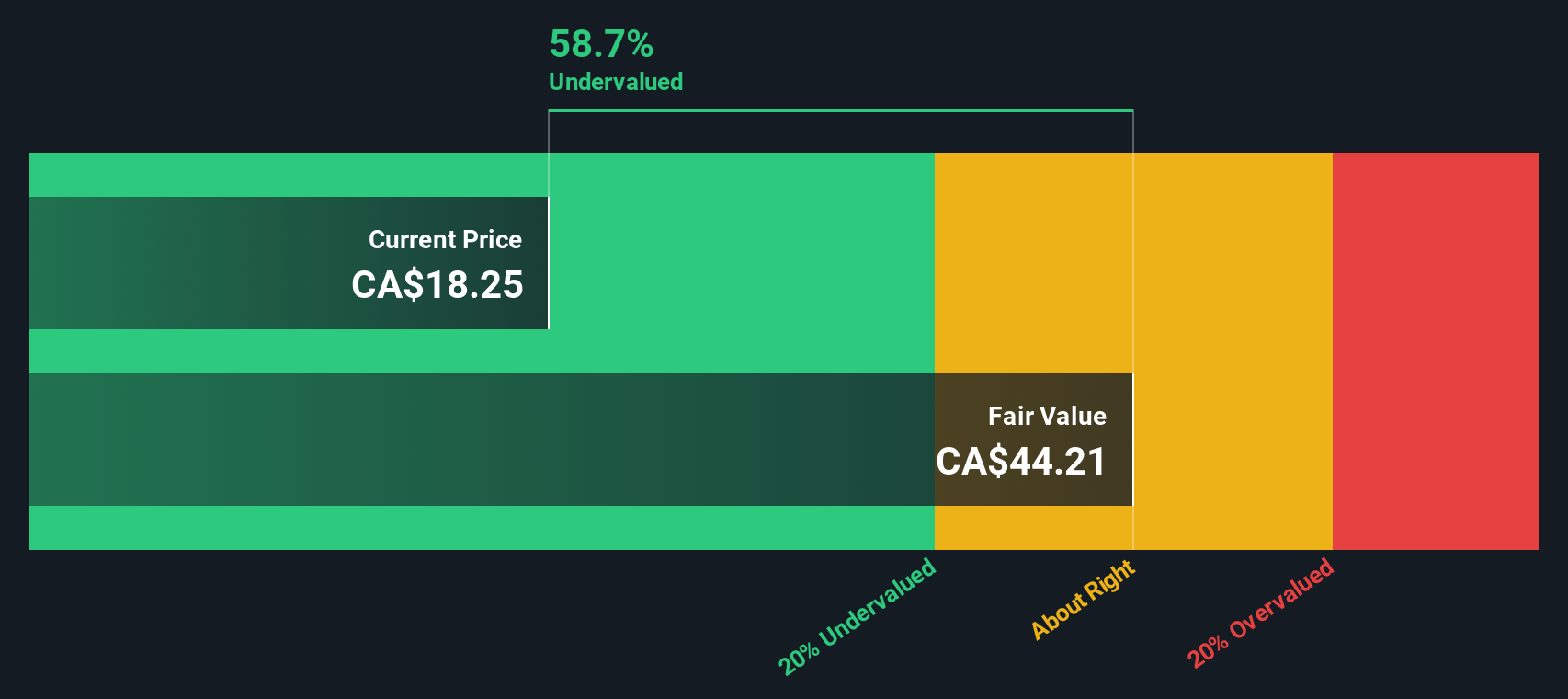

| Nexus Industrial REIT | 11.9x | 3.0x | 23.52% | ★★★★★☆ |

| Baytex Energy | NA | 0.8x | -119.13% | ★★★★☆☆ |

| Bonterra Energy | 5.1x | 0.6x | 30.62% | ★★★★☆☆ |

| Parex Resources | 3.9x | 0.9x | -18.43% | ★★★☆☆☆ |

| Primaris Real Estate Investment Trust | 20.0x | 3.2x | 47.11% | ★★★☆☆☆ |

| Calfrac Well Services | 12.0x | 0.2x | -39.18% | ★★★☆☆☆ |

| Saturn Oil & Gas | 1.9x | 0.6x | -65.86% | ★★★☆☆☆ |

| Minto Apartment Real Estate Investment Trust | NA | 5.4x | 14.29% | ★★★☆☆☆ |

Here's a peek at a few of the choices from the screener.

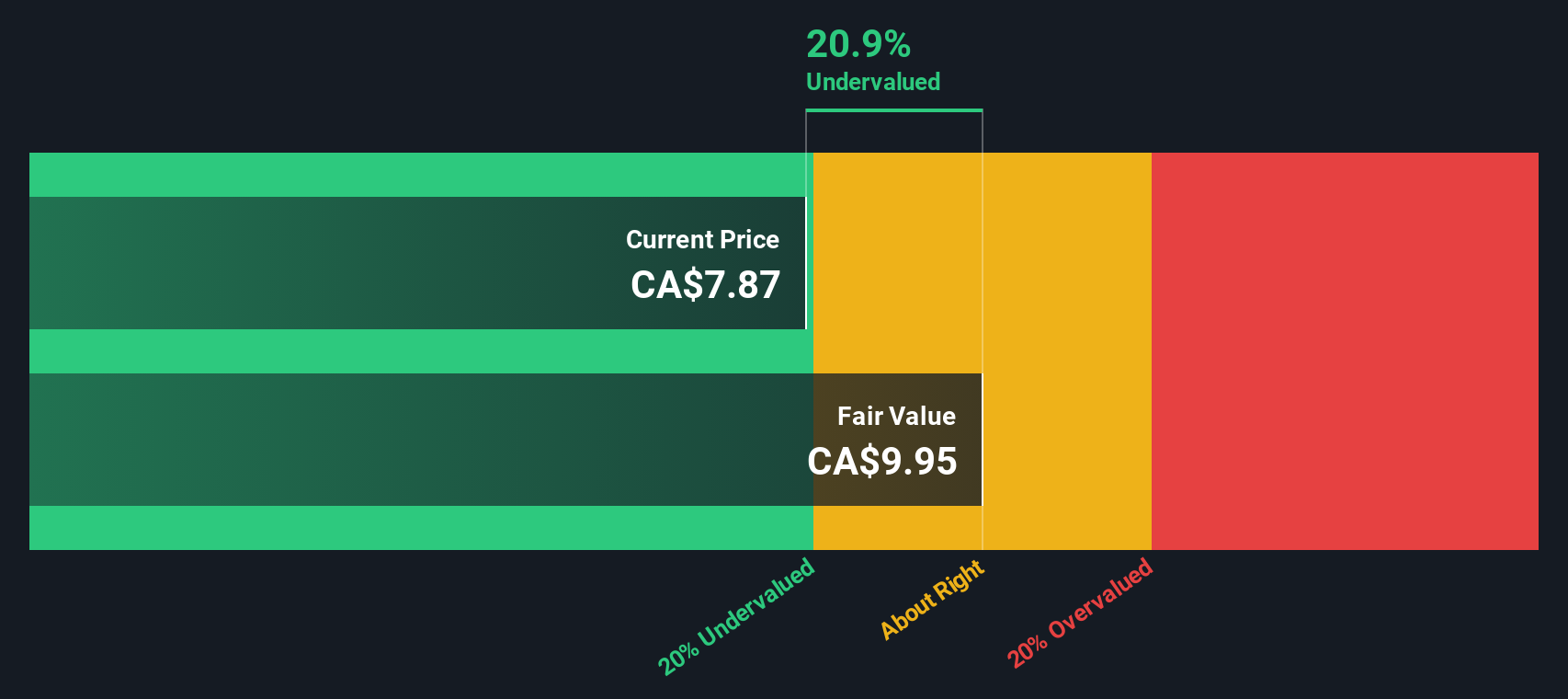

Baytex Energy (TSX:BTE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Baytex Energy is a Canadian company engaged in the exploration and production of oil and gas, with operations generating CA$3.36 billion in revenue.

Operations: The company generates revenue primarily from oil and gas exploration and production, with a recent gross profit margin of 68.54%. Costs include COGS at CA$1.06 billion and operating expenses at CA$2.35 billion for the latest period, impacting net income which stands at a loss of CA$350.76 million.

PE: -7.8x

Baytex Energy, a smaller Canadian energy player, is catching attention with its forecasted 30% annual earnings growth. The company recently announced a fixed-income offering with 7.375% senior unsecured notes due in 2032, highlighting their reliance on external funding. Production guidance for 2025 targets between 150,000 and 154,000 boe/d. Insider confidence is evident from recent share purchases within the past year. While risks exist due to funding strategies, growth potential remains significant in the energy sector's evolving landscape.

Flagship Communities Real Estate Investment Trust (TSX:MHC.UN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Flagship Communities Real Estate Investment Trust focuses on owning and operating manufactured housing communities, with a market capitalization of approximately $0.51 billion.

Operations: Flagship Communities Real Estate Investment Trust generates revenue primarily from residential real estate investments, with a recent quarterly revenue of $83.14 million. The gross profit margin has shown some fluctuations, most recently recorded at 66.08%. Operating expenses are a significant cost factor, with general and administrative expenses reaching $10.29 million in the latest period.

PE: 3.7x

Flagship Communities Real Estate Investment Trust, a smaller player in the Canadian market, faces challenges with earnings expected to decline by 46% annually over the next three years. Despite this, revenue is projected to grow nearly 9% per year. The REIT's financial position is strained, as interest payments aren't well covered by earnings and funding relies entirely on riskier external borrowing. Insider confidence remains low due to past shareholder dilution and no recent insider purchases. Consistent monthly dividends of US$0.0517 per unit highlight a commitment to returning value to shareholders amidst these challenges.

Nexus Industrial REIT (TSX:NXR.UN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Nexus Industrial REIT is a Canadian real estate investment trust focused on owning and managing a portfolio of industrial properties, with operations generating CA$172.86 million in revenue from its investment properties.

Operations: The company generates revenue primarily from investment properties, with a recent gross profit margin of 71.02%. Operating expenses have shown fluctuations, impacting net income margins over time. Notably, the net income margin reached 123.47% in March 2024 but fell to 25.07% by September 2024 due to increased non-operating expenses.

PE: 11.9x

Nexus Industrial REIT, a smaller player in the Canadian market, has caught attention with its insider confidence as they increased their holdings in the past year. Despite a dip in profit margins from 90.9% to 25.1%, earnings are projected to climb by 12% annually, hinting at potential growth. However, reliance on external borrowing poses risks as interest payments aren't fully covered by earnings. Recent dividend affirmations enhance its appeal for income-focused investors seeking steady cash flow.

- Take a closer look at Nexus Industrial REIT's potential here in our valuation report.

Assess Nexus Industrial REIT's past performance with our detailed historical performance reports.

Make It Happen

- Access the full spectrum of 26 Undervalued TSX Small Caps With Insider Buying by clicking on this link.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nexus Industrial REIT might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:NXR.UN

Nexus Industrial REIT

Nexus is a growth-oriented real estate investment trust focused on increasing unitholder value through the acquisition of industrial properties located in primary and secondary markets in Canada, and the ownership and management of its portfolio of properties.

Established dividend payer and good value.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)