Advertisement

Acasti Pharma (CVE:ACST) Is In A Strong Position To Grow Its Business

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

Given this risk, we thought we'd take a look at whether Acasti Pharma (CVE:ACST) shareholders should be worried about its cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

Check out our latest analysis for Acasti Pharma

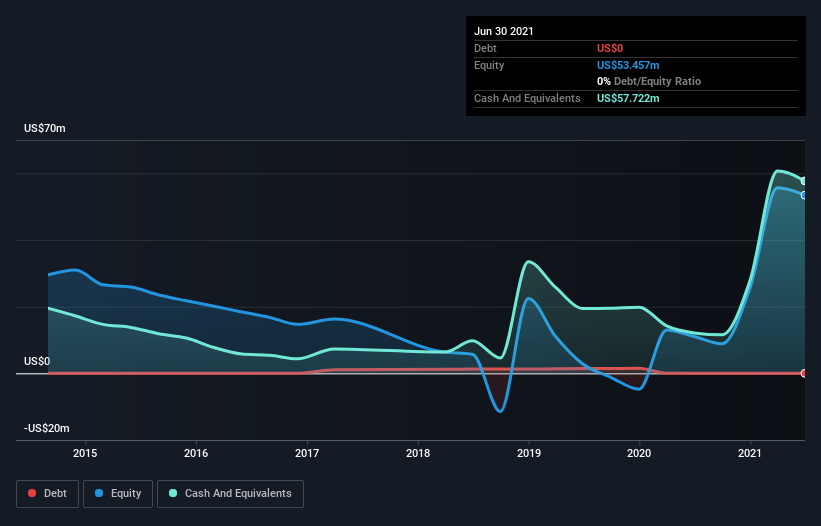

How Long Is Acasti Pharma's Cash Runway?

A company's cash runway is calculated by dividing its cash hoard by its cash burn. Acasti Pharma has such a small amount of debt that we'll set it aside, and focus on the US$58m in cash it held at June 2021. In the last year, its cash burn was US$14m. Therefore, from June 2021 it had 4.2 years of cash runway. Notably, however, analysts think that Acasti Pharma will break even (at a free cash flow level) before then. In that case, it may never reach the end of its cash runway. The image below shows how its cash balance has been changing over the last few years.

How Is Acasti Pharma's Cash Burn Changing Over Time?

Whilst it's great to see that Acasti Pharma has already begun generating revenue from operations, last year it only produced US$196k, so we don't think it is generating significant revenue, at this point. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. While it hardly paints a picture of imminent growth, the fact that it has reduced its cash burn by 35% over the last year suggests some degree of prudence. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Easily Can Acasti Pharma Raise Cash?

Even though it has reduced its cash burn recently, shareholders should still consider how easy it would be for Acasti Pharma to raise more cash in the future. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Acasti Pharma's cash burn of US$14m is about 14% of its US$94m market capitalisation. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

How Risky Is Acasti Pharma's Cash Burn Situation?

As you can probably tell by now, we're not too worried about Acasti Pharma's cash burn. For example, we think its cash runway suggests that the company is on a good path. Its cash burn relative to its market cap wasn't quite as good, but was still rather encouraging! It's clearly very positive to see that analysts are forecasting the company will break even fairly soon. After considering a range of factors in this article, we're pretty relaxed about its cash burn, since the company seems to be in a good position to continue to fund its growth. Taking a deeper dive, we've spotted 4 warning signs for Acasti Pharma you should be aware of, and 2 of them can't be ignored.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies insiders are buying, and this list of stocks growth stocks (according to analyst forecasts)

If you’re looking to trade a wide range of investments, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSXV:ACST

Acasti Pharma

Engages in the development and commercialization of pharmaceutical products for rare and orphan diseases in Canada.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|43.6% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|36.4% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|28.4% undervalued

MA

Community Contributor