Advertisement

- Canada

- /

- Interactive Media and Services

- /

- TSX:MDF

Shareholders May Be Wary Of Increasing mdf commerce inc.'s (TSE:MDF) CEO Compensation Package

Key Insights

- mdf commerce's Annual General Meeting to take place on 19th of September

- CEO Luc Filiatreault's total compensation includes salary of CA$465.3k

- The total compensation is 37% higher than the average for the industry

- mdf commerce's three-year loss to shareholders was 50% while its EPS was down 57% over the past three years

mdf commerce inc. (TSE:MDF) has not performed well recently and CEO Luc Filiatreault will probably need to up their game. At the upcoming AGM on 19th of September, shareholders can hear from the board including their plans for turning around performance. It would also be an opportunity for shareholders to influence management through voting on company resolutions such as executive remuneration, which could impact the firm significantly. From our analysis, we think CEO compensation may need a review in light of the recent performance.

See our latest analysis for mdf commerce

How Does Total Compensation For Luc Filiatreault Compare With Other Companies In The Industry?

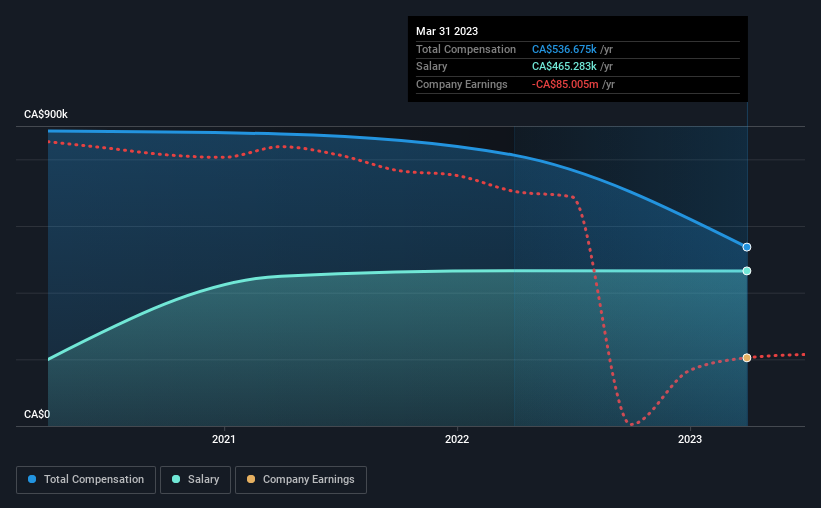

According to our data, mdf commerce inc. has a market capitalization of CA$149m, and paid its CEO total annual compensation worth CA$537k over the year to March 2023. We note that's a decrease of 34% compared to last year. Notably, the salary which is CA$465.3k, represents most of the total compensation being paid.

On comparing similar-sized companies in the Canadian Interactive Media and Services industry with market capitalizations below CA$271m, we found that the median total CEO compensation was CA$392k. Hence, we can conclude that Luc Filiatreault is remunerated higher than the industry median. Furthermore, Luc Filiatreault directly owns CA$276k worth of shares in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CA$465k | CA$465k | 87% |

| Other | CA$71k | CA$347k | 13% |

| Total Compensation | CA$537k | CA$813k | 100% |

On an industry level, around 87% of total compensation represents salary and 13% is other remuneration. mdf commerce is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

mdf commerce inc.'s Growth

mdf commerce inc. has reduced its earnings per share by 57% a year over the last three years. In the last year, its revenue is up 7.8%.

The decline in EPS is a bit concerning. The fairly low revenue growth fails to impress given that the EPS is down. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has mdf commerce inc. Been A Good Investment?

The return of -50% over three years would not have pleased mdf commerce inc. shareholders. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Along with the business performing poorly, shareholders have suffered with poor share price returns on their investments, suggesting that there's little to no chance of them being in favor of a CEO pay raise. At the upcoming AGM, management will get a chance to explain how they plan to get the business back on track and address the concerns from investors.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 2 warning signs (and 1 which can't be ignored) in mdf commerce we think you should know about.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:MDF

mdf commerce

Through its subsidiaries, provides software as a service (SaaS) solutions for consumers and businesses in Canada, the United States, Europe, Asia, and internationally.

Adequate balance sheet and overvalued.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor