Advertisement

- Canada

- /

- Paper and Forestry Products

- /

- TSX:WFG

Why You Might Be Interested In West Fraser Timber Co. Ltd. (TSE:WFT) For Its Upcoming Dividend

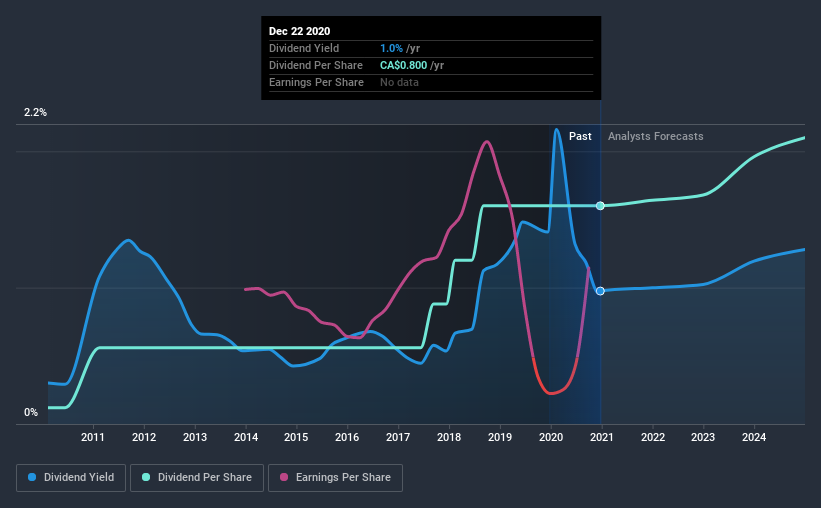

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see West Fraser Timber Co. Ltd. (TSE:WFT) is about to trade ex-dividend in the next four days. Investors can purchase shares before the 28th of December in order to be eligible for this dividend, which will be paid on the 12th of January.

West Fraser Timber's next dividend payment will be CA$0.20 per share, on the back of last year when the company paid a total of CA$0.80 to shareholders. Last year's total dividend payments show that West Fraser Timber has a trailing yield of 1.0% on the current share price of CA$82.06. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

See our latest analysis for West Fraser Timber

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. That's why it's good to see West Fraser Timber paying out a modest 26% of its earnings. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. What's good is that dividends were well covered by free cash flow, with the company paying out 7.8% of its cash flow last year.

It's positive to see that West Fraser Timber's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Fortunately for readers, West Fraser Timber's earnings per share have been growing at 12% a year for the past five years. The company has managed to grow earnings at a rapid rate, while reinvesting most of the profits within the business. Fast-growing businesses that are reinvesting heavily are enticing from a dividend perspective, especially since they can often increase the payout ratio later.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the last 10 years, West Fraser Timber has lifted its dividend by approximately 30% a year on average. It's exciting to see that both earnings and dividends per share have grown rapidly over the past few years.

The Bottom Line

Should investors buy West Fraser Timber for the upcoming dividend? West Fraser Timber has been growing earnings at a rapid rate, and has a conservatively low payout ratio, implying that it is reinvesting heavily in its business; a sterling combination. West Fraser Timber looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

On that note, you'll want to research what risks West Fraser Timber is facing. To that end, you should learn about the 2 warning signs we've spotted with West Fraser Timber (including 1 which is concerning).

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade West Fraser Timber, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if West Fraser Timber might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:WFG

West Fraser Timber

A diversified wood products company, engages in manufacturing, selling, marketing, and distributing lumber, engineered wood products, pulp, newsprint, wood chips, and other residuals and renewable energy.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|2.3% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|40.4% undervalued

TR

Community Contributor