- Canada

- /

- Metals and Mining

- /

- TSX:SKE

Skeena Resources (TSX:SKE): How Does Its Valuation Stack Up After Major Equity Raise for Eskay Creek?

Reviewed by Kshitija Bhandaru

Skeena Resources (TSX:SKE) just wrapped up a significant follow-on equity offering, raising CAD 125 million to help drive progress at its flagship Eskay Creek project and support broader company initiatives.

See our latest analysis for Skeena Resources.

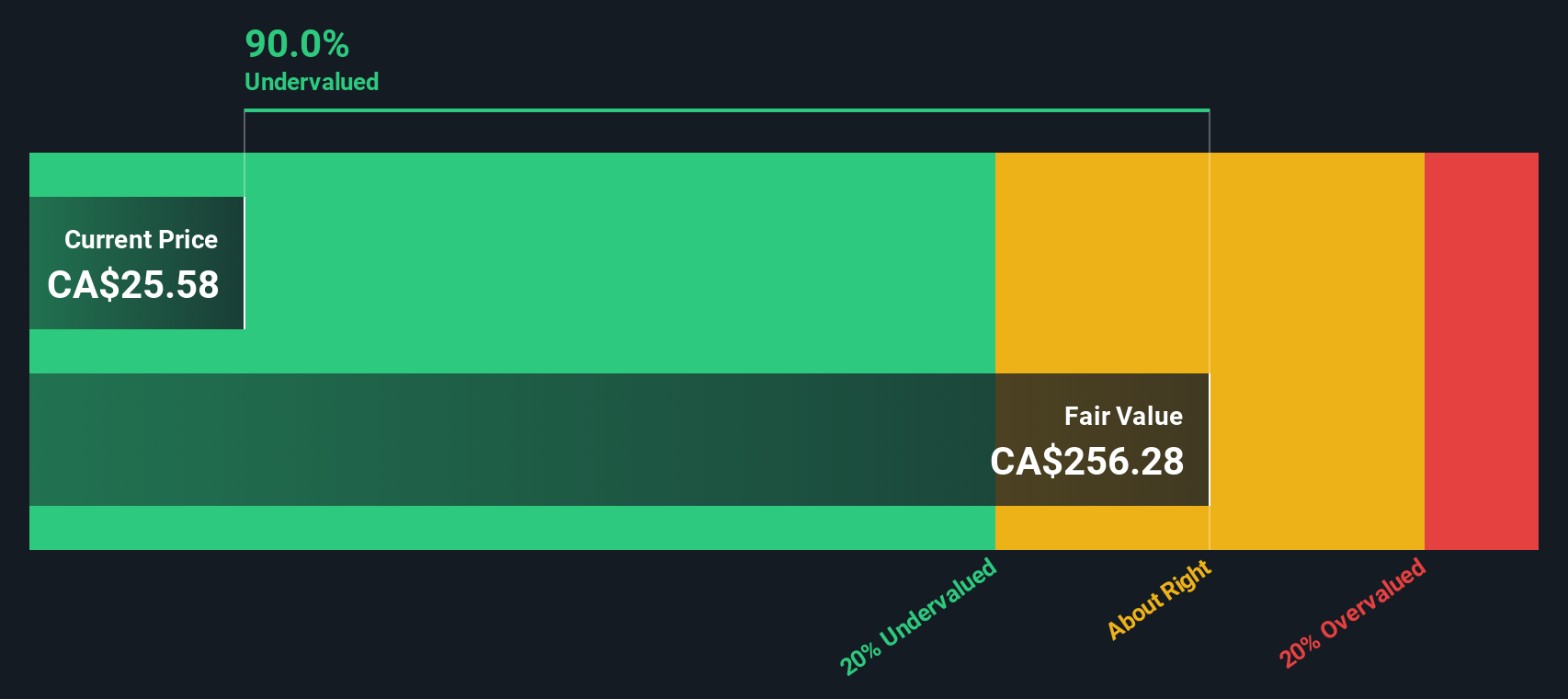

Skeena Resources’ successful capital raise comes amid growing optimism around its Eskay Creek project. The company’s 1-year total shareholder return has soared 110%, and momentum is clearly building. The latest share price sits at $25.58, reflecting renewed confidence and a strong long-term track record.

If Skeena’s momentum has you curious about what else investors are watching, this is a perfect time to discover fast growing stocks with high insider ownership

The question now is whether Skeena’s recent surge still leaves room for upside, or if the stock’s impressive performance means the market has already priced in all of its growth potential. Is there a real buying opportunity here, or has future success already been accounted for?

Price-to-Book of 26.1x: Is it justified?

Skeena Resources trades at a price-to-book ratio of 26.1x, a level that stands in stark contrast to its peers and the overall industry. The most recent share price of $25.58 significantly exceeds sector benchmarks, raising questions on whether this premium is supported by fundamentals or market enthusiasm.

The price-to-book ratio measures how much investors are willing to pay for each dollar of a company's net assets. For exploration and mining companies like Skeena, this multiple can reflect optimism about future discoveries, resources, or project development. However, such a high figure compared to industry averages could suggest exuberant expectations or a disconnect from underlying asset values.

Specifically, Skeena’s ratio is much higher than the Canadian Metals and Mining industry average of 2.7x and the peer average of 3.4x. This gap signals that investors are pricing in substantial future success, far beyond what comparable companies receive. If the market were to re-evaluate sector multiples or company-specific outlooks, there could be a meaningful realignment in valuation levels.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Book of 26.1x (OVERVALUED)

However, with no revenue and persistent net losses, investor optimism could falter if progress at Eskay Creek stalls or if broader metals markets weaken.

Find out about the key risks to this Skeena Resources narrative.

Another View: The DCF Model Perspective

While Skeena’s price-to-book ratio paints the picture of a premium-priced stock, our DCF model takes a different approach. It estimates the company’s fair value at CA$256.27, which is dramatically higher than the current trading price of CA$25.58. This suggests the stock may actually be undervalued rather than expensive.

Which of these signals will prove more accurate as things progress for Skeena?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Skeena Resources for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Skeena Resources Narrative

If you see things differently or want to dive deeper on your own, you can shape your own analysis in just a few minutes. Do it your way

A great starting point for your Skeena Resources research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors always keep an eye out for new opportunities beyond the obvious. Don’t miss your chance to get ahead and build a resilient portfolio using handpicked stock screeners on Simply Wall St.

- Tap into fast-growing profits by checking out these 18 dividend stocks with yields > 3%, which is backed by strong yields and a history of rewarding income-focused investors.

- Unlock early-stage potential in technology breakthroughs as you review these 25 AI penny stocks, positioned for artificial intelligence leadership and next-level innovation.

- Ride the momentum of digital assets by exploring these 79 cryptocurrency and blockchain stocks, dedicated to blockchain pioneers shaping tomorrow’s financial landscape.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:SKE

Skeena Resources

Engages in the exploration and development of mineral properties in Canada.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion