- Canada

- /

- Metals and Mining

- /

- TSX:OGD

Orbit Garant Drilling Inc. (TSE:OGD) Shares Fly 41% But Investors Aren't Buying For Growth

Orbit Garant Drilling Inc. (TSE:OGD) shareholders would be excited to see that the share price has had a great month, posting a 41% gain and recovering from prior weakness. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 24% over that time.

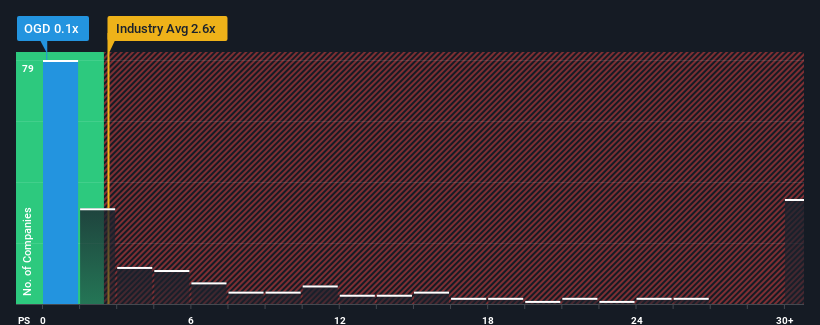

Although its price has surged higher, Orbit Garant Drilling's price-to-sales (or "P/S") ratio of 0.1x might still make it look like a strong buy right now compared to the wider Metals and Mining industry in Canada, where around half of the companies have P/S ratios above 2.6x and even P/S above 15x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

View our latest analysis for Orbit Garant Drilling

How Orbit Garant Drilling Has Been Performing

Orbit Garant Drilling hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. The P/S ratio is probably low because investors think this poor revenue performance isn't going to get any better. If you still like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Keen to find out how analysts think Orbit Garant Drilling's future stacks up against the industry? In that case, our free report is a great place to start.Is There Any Revenue Growth Forecasted For Orbit Garant Drilling?

Orbit Garant Drilling's P/S ratio would be typical for a company that's expected to deliver very poor growth or even falling revenue, and importantly, perform much worse than the industry.

Retrospectively, the last year delivered a frustrating 9.9% decrease to the company's top line. However, a few very strong years before that means that it was still able to grow revenue by an impressive 44% in total over the last three years. Although it's been a bumpy ride, it's still fair to say the revenue growth recently has been more than adequate for the company.

Turning to the outlook, the next year should generate growth of 5.1% as estimated by the sole analyst watching the company. Meanwhile, the rest of the industry is forecast to expand by 10%, which is noticeably more attractive.

In light of this, it's understandable that Orbit Garant Drilling's P/S sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Bottom Line On Orbit Garant Drilling's P/S

Orbit Garant Drilling's recent share price jump still sees fails to bring its P/S alongside the industry median. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that Orbit Garant Drilling maintains its low P/S on the weakness of its forecast growth being lower than the wider industry, as expected. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

There are also other vital risk factors to consider and we've discovered 2 warning signs for Orbit Garant Drilling (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

If you're unsure about the strength of Orbit Garant Drilling's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:OGD

Orbit Garant Drilling

Provides mineral drilling services in Canada, the United States, Central and South America, and West Africa.

Adequate balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives