Advertisement

The Canadian market has been experiencing a robust year, with the TSX climbing over 17%, reflecting a broader trend of economic growth, favorable central bank policies, and increasing corporate profits. In this context of market strength and optimism, discovering lesser-known stocks that exhibit strong fundamentals and potential for growth can be particularly rewarding for investors seeking to diversify their portfolios.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 15.28% | 7.58% | ★★★★★★ |

| Santacruz Silver Mining | 14.30% | 49.04% | 63.44% | ★★★★★★ |

| Taiga Building Products | NA | 6.05% | 10.50% | ★★★★★★ |

| Grown Rogue International | 24.92% | 43.35% | 67.95% | ★★★★★☆ |

| Mako Mining | 22.90% | 38.12% | 54.79% | ★★★★★☆ |

| Pizza Pizza Royalty | 15.66% | 3.64% | 3.95% | ★★★★☆☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

| Dundee | 5.93% | -38.65% | 39.44% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Centerra Gold (TSX:CG)

Simply Wall St Value Rating: ★★★★★★

Overview: Centerra Gold Inc. is a gold mining company involved in the acquisition, exploration, development, and operation of gold and copper properties across North America, Turkey, and internationally, with a market capitalization of approximately CA$2.18 billion.

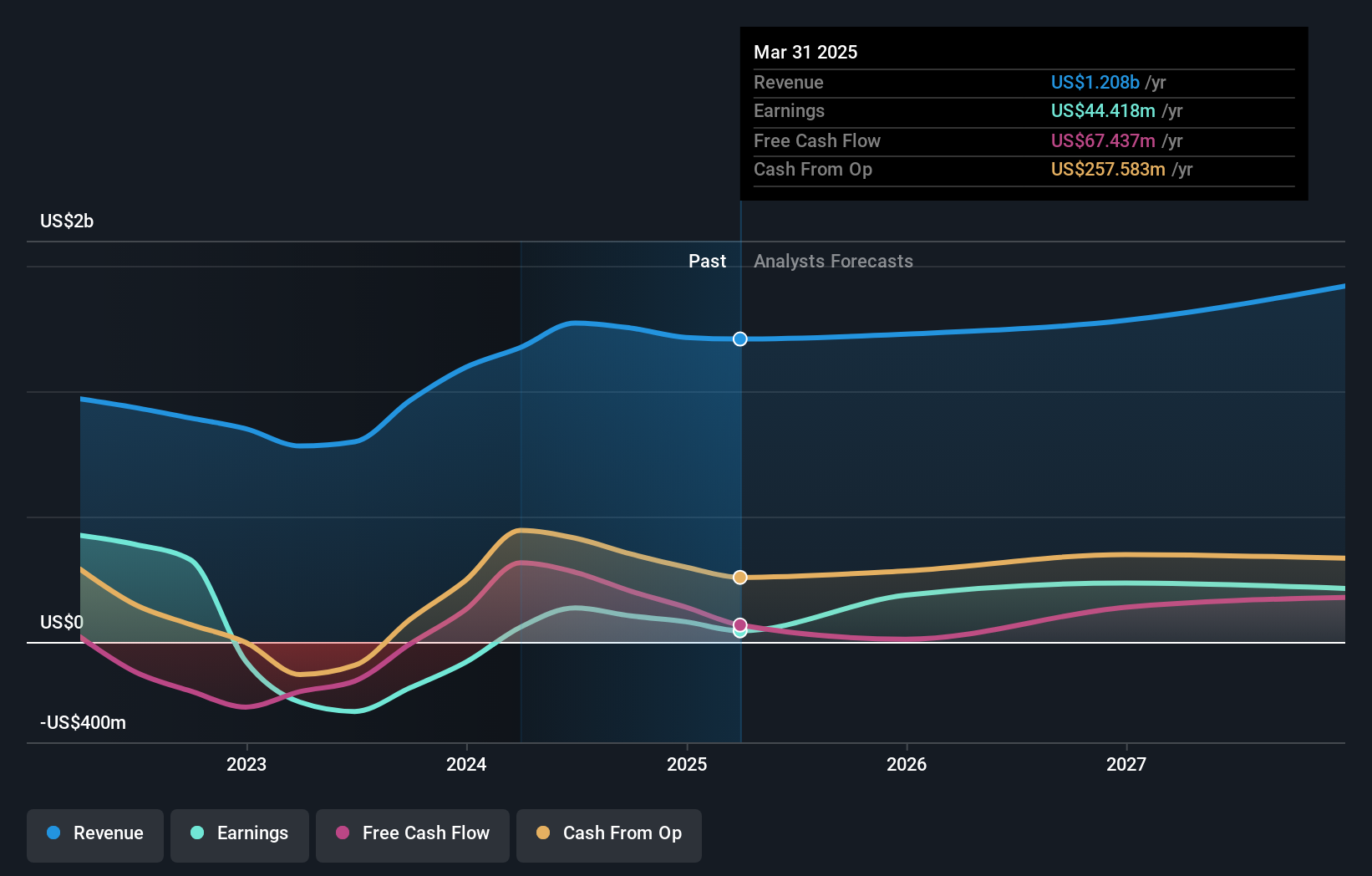

Operations: Centerra Gold generates revenue primarily from its Öksüt, Molybdenum, and Mount Milligan segments, with contributions of $603.31 million, $239.65 million, and $429.08 million respectively. The company's financial performance is influenced by its cost structure and market conditions affecting these segments.

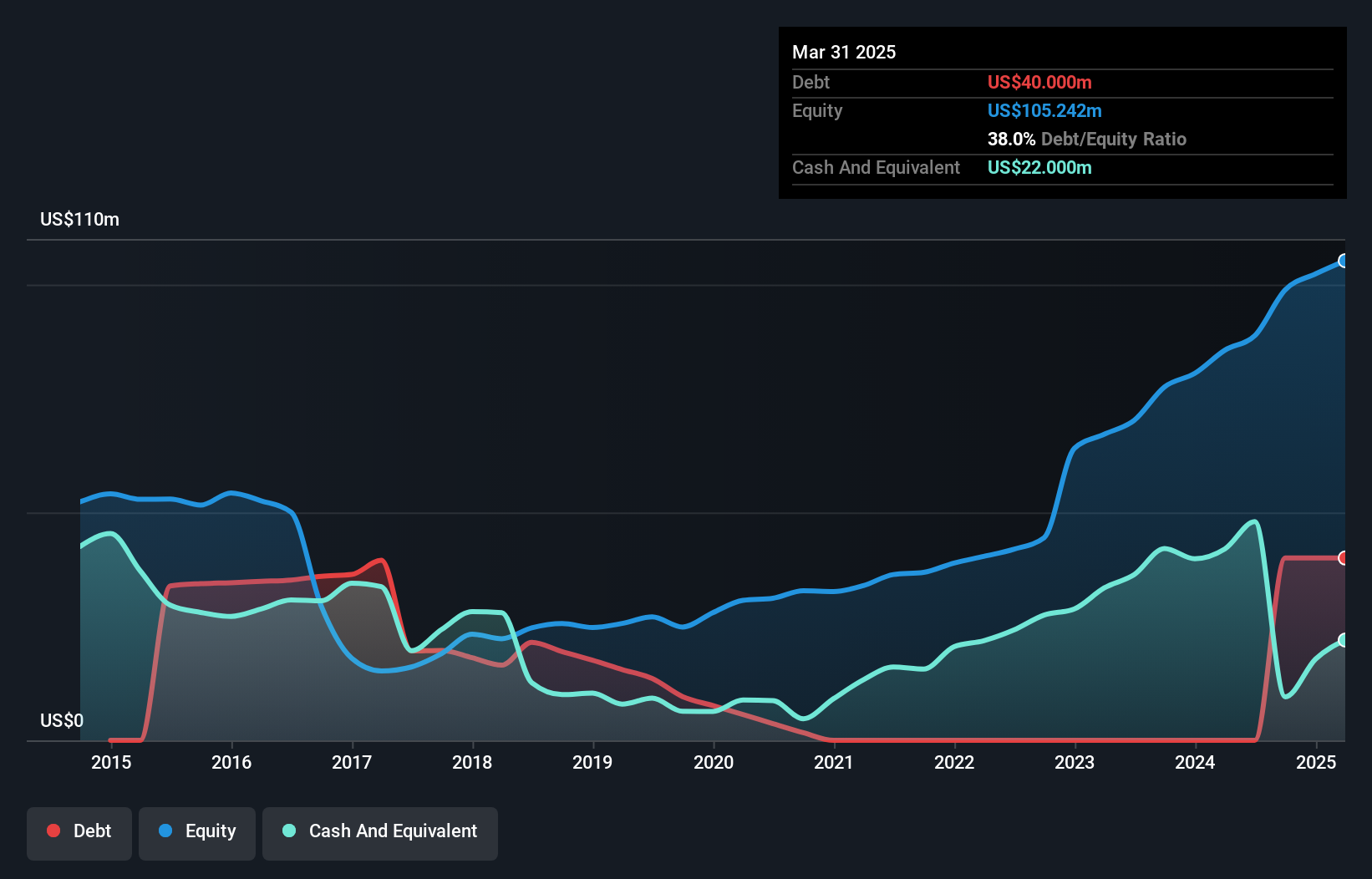

Centerra Gold, a notable player in the mining sector, is navigating its path with no debt on its books, contrasting with a 4.2% debt-to-equity ratio five years ago. The company trades at 53.1% below its estimated fair value, suggesting potential upside compared to industry peers. Recent financials show a turnaround with net income of US$104 million for the first half of 2024 versus a loss last year and earnings per share reaching US$0.49 from continuing operations. Despite significant insider selling recently, it has repurchased over 3 million shares for US$21.9 million this year, indicating confidence in its valuation prospects despite forecasted earnings decline by an average of 6.1% annually over the next three years.

- Get an in-depth perspective on Centerra Gold's performance by reading our health report here.

Review our historical performance report to gain insights into Centerra Gold's's past performance.

Cipher Pharmaceuticals (TSX:CPH)

Simply Wall St Value Rating: ★★★★★★

Overview: Cipher Pharmaceuticals Inc. is a specialty pharmaceutical company based in Canada with a market capitalization of CA$421.70 million.

Operations: Cipher Pharmaceuticals generates revenue primarily from its specialty pharmaceuticals segment, amounting to CA$22.16 million.

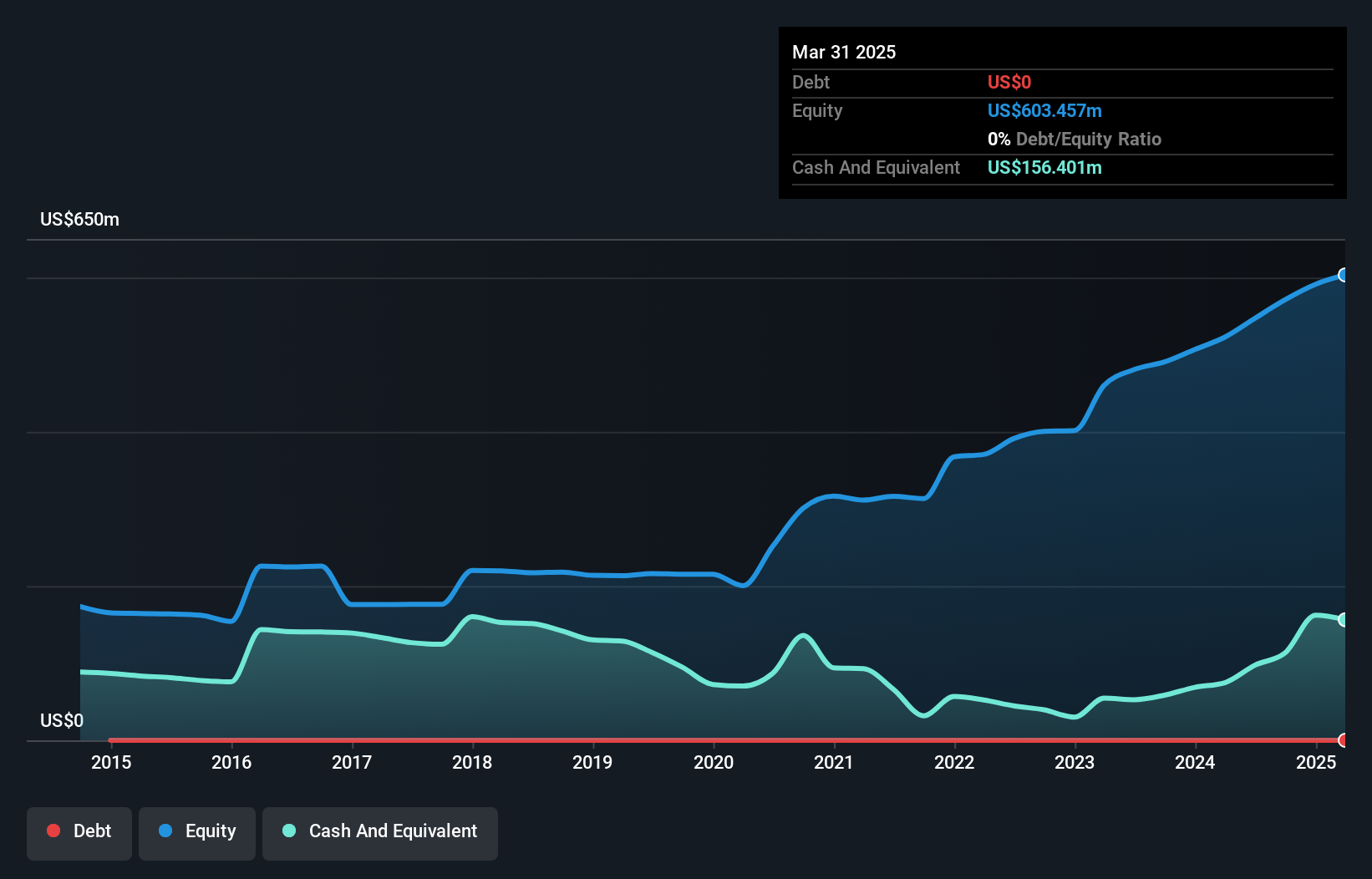

Cipher Pharmaceuticals, a small yet intriguing player in the Canadian market, showcases a debt-free status which is quite appealing. Over the past five years, it has managed to eliminate its debt from a 50.1% debt-to-equity ratio, highlighting financial discipline. Despite facing negative earnings growth of -19.4% last year, this figure fares better than the industry average of -40.8%. The company trades at 60.7% below its estimated fair value and maintains high-quality earnings with free cash flow positivity evident in recent figures like US$16.89 million as of October 2024. Recent leadership changes could steer future growth opportunities effectively.

MAG Silver (TSX:MAG)

Simply Wall St Value Rating: ★★★★★★

Overview: MAG Silver Corp. is involved in the development and exploration of precious metal properties in Canada, with a market capitalization of CA$2.54 billion.

Operations: MAG Silver Corp. generates revenue primarily through the development and exploration of precious metal properties. The company has a market capitalization of CA$2.54 billion, reflecting its valuation in the financial markets.

MAG Silver, a nimble player in the mining sector, has showcased impressive growth with earnings surging 94% over the past year, outpacing its industry peers. The company is debt-free and has maintained this status for five years, highlighting financial prudence. Recent production results from Juanicipio show increased outputs across silver (4.89 million oz), gold (10,801 oz), lead (10.66 million lb), and zinc (16.76 million lb) compared to last year’s figures. Despite these robust metrics, future earnings are predicted to dip by 7% annually over the next three years, suggesting potential headwinds ahead for MAG Silver's profitability trajectory.

- Navigate through the intricacies of MAG Silver with our comprehensive health report here.

Understand MAG Silver's track record by examining our Past report.

Key Takeaways

- Investigate our full lineup of 51 TSX Undiscovered Gems With Strong Fundamentals right here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CPH

Cipher Pharmaceuticals

Operates as a specialty pharmaceutical company in Canada.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% undervalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|45.0% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.4% undervalued

TI

Community Contributor