- Canada

- /

- Metals and Mining

- /

- TSX:K

Is It Too Late to Consider Kinross Gold After Its 176% Rally?

Reviewed by Bailey Pemberton

- If you are wondering whether Kinross Gold is still a smart buy after its huge run, or if you are turning up late to the party, this breakdown is designed to help you figure out what the current price really implies.

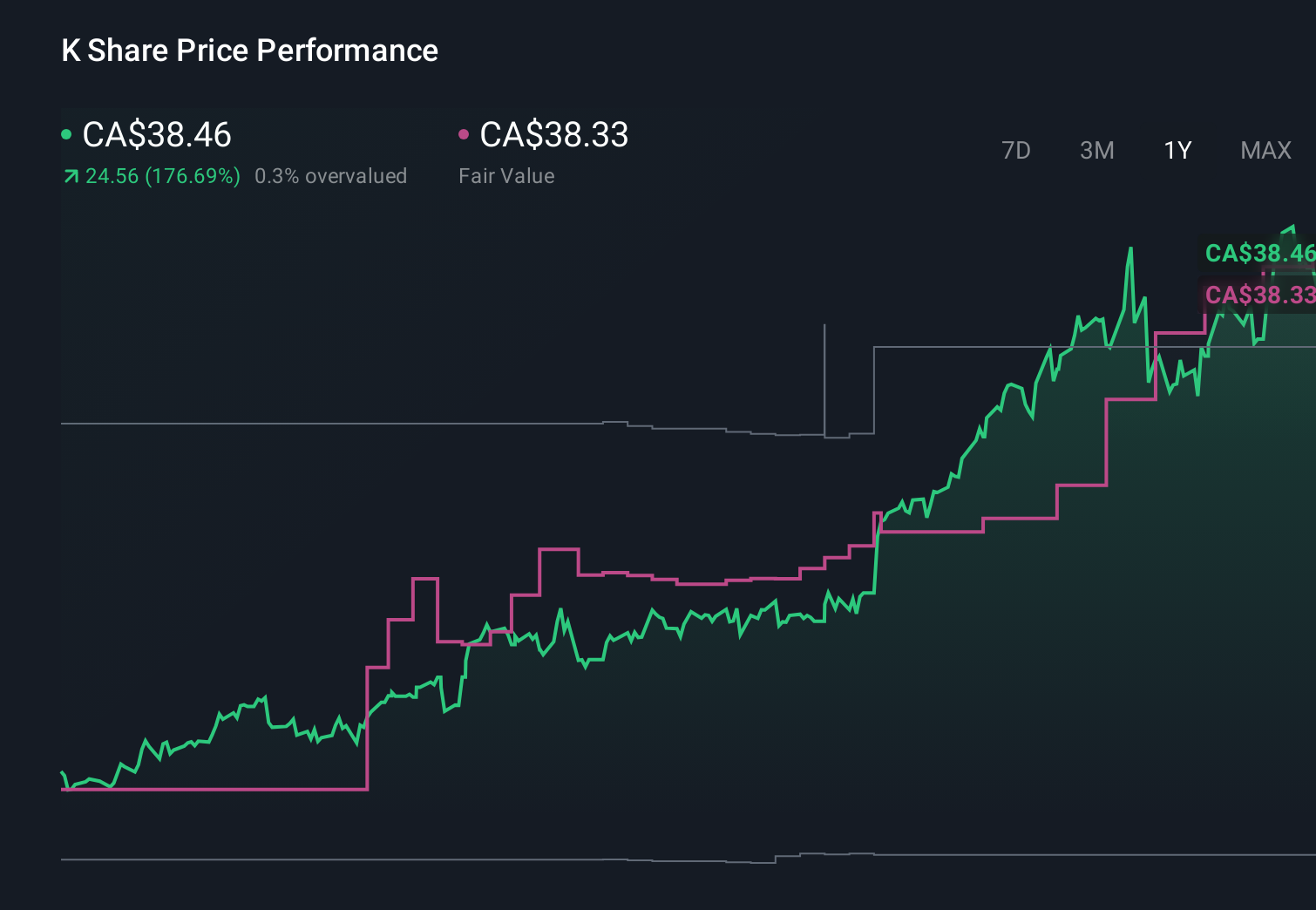

- The stock has climbed about 3.0% over the last week, 10.8% over the last month and 176.0% year to date, with a 177.1% gain over the past year and more than 600% over three years reshaping how the market views its prospects and risk profile.

- Recent moves in gold prices and shifting expectations around interest rate cuts have reignited investor interest in gold producers, putting names like Kinross back in the spotlight. In addition, sector wide attention on capital discipline and balance sheet strength has helped re rate miners that can show they are running efficiently and returning cash to shareholders.

- Despite those big gains, Kinross currently scores just 2/6 on our undervaluation checks. This suggests the story is a bit more nuanced than simply calling it cheap or expensive. Next we will walk through different valuation approaches, then finish with another way to think about what the market is really pricing in.

Kinross Gold scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Kinross Gold Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business is worth by projecting its future cash flows and then discounting them back to today to reflect risk and the time value of money.

Kinross Gold generated about $1.87 billion of free cash flow over the last twelve months, providing a solid starting point for the valuation. Analysts supply detailed forecasts for the next few years. Beyond that, Simply Wall St extrapolates a gradual slowdown in growth, with projected free cash flow declining to around $0.78 billion by 2035 as the company matures and growth normalizes.

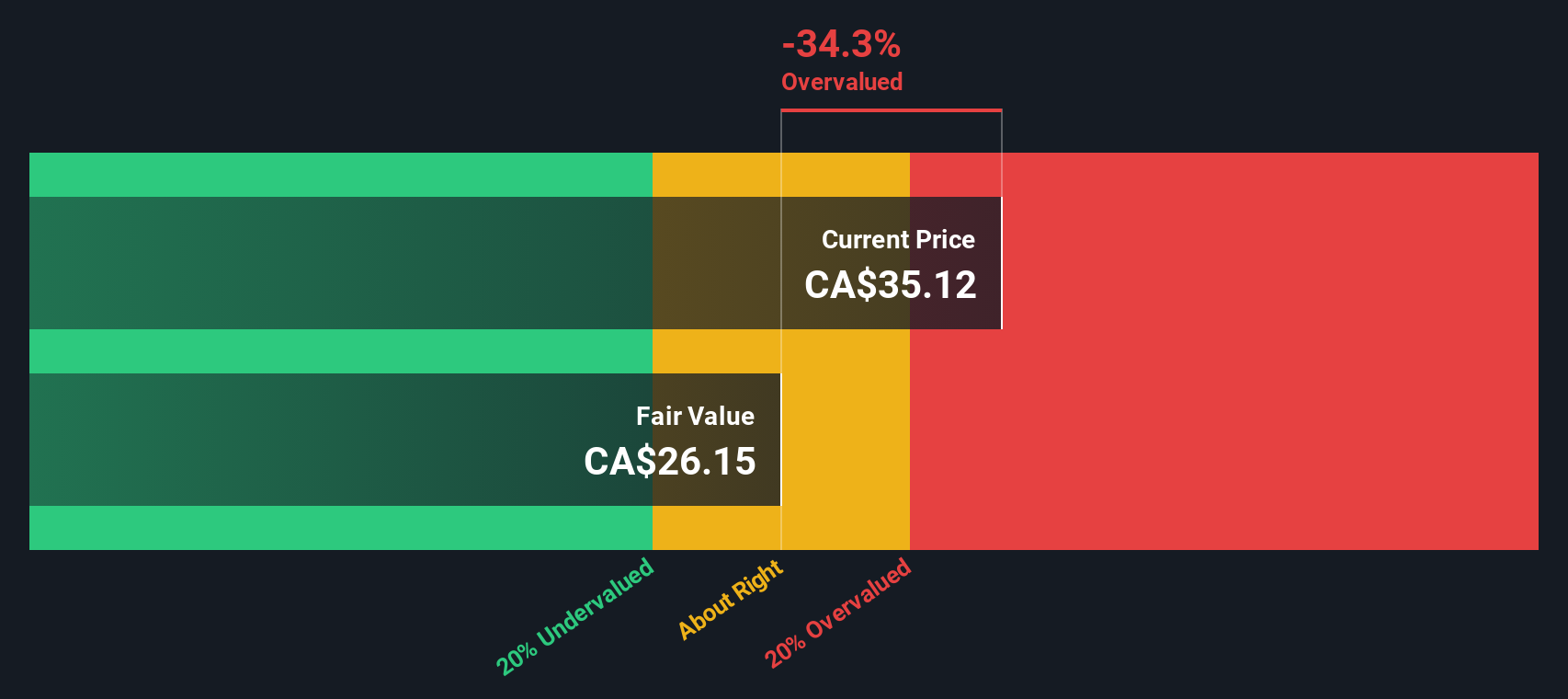

When all of those projected cash flows are discounted back to today using a 2 Stage Free Cash Flow to Equity model, the estimated intrinsic value comes out to roughly $23.54 per share. Compared with the current market price, this implies Kinross is about 67.1% overvalued on a DCF basis, so the recent share price surge appears to be running well ahead of the underlying cash flow outlook.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Kinross Gold may be overvalued by 67.1%. Discover 904 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: Kinross Gold Price vs Earnings

For a profitable company like Kinross, the price to earnings, or PE, ratio is a useful way to gauge how much investors are willing to pay for each dollar of current earnings. In general, faster growth and lower risk justify a higher PE, while slower growth, more cyclical earnings or higher uncertainty usually deserve a lower, more conservative multiple.

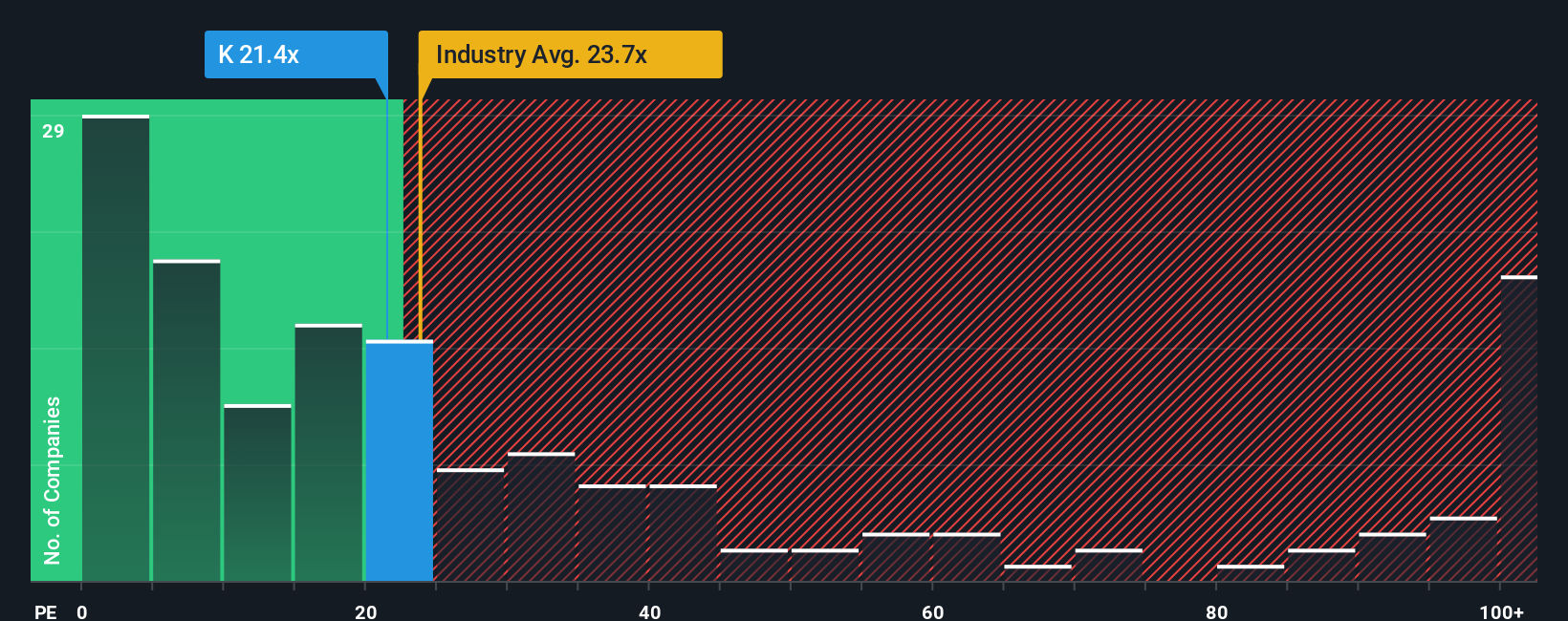

Kinross currently trades on a PE of about 19.6x, which is slightly below the broader Metals and Mining industry average of around 21.7x and well below its peer group average of roughly 40.0x. At first glance, that discount could suggest some value, but simple comparisons like this do not fully capture company specific growth prospects, profitability or risk.

To address that, Simply Wall St uses a proprietary Fair Ratio, which estimates what a reasonable PE should be after considering Kinross Gold’s earnings growth outlook, margins, risk profile, size and industry. For Kinross, the Fair Ratio is 19.6x, almost identical to where the stock currently trades. Because this approach is tailored to the company’s own fundamentals rather than generic peer averages, it provides a more precise gauge of value, and it indicates that Kinross is trading very close to fair value on an earnings multiple basis.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1447 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Kinross Gold Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page that lets you tell the story behind your numbers. It links your view of Kinross Gold’s future revenue, earnings and margins to a forecast, a fair value, and then a clear view on how that fair value compares to today’s price. All of this updates automatically as new news or earnings arrive. For example, one investor might build a bullish Kinross Narrative around resilient gold prices, expanding margins and strong buybacks that supports a fair value close to about CA$38 per share. A more cautious investor could focus on cost inflation, political risk and softer long term production to justify a much lower fair value closer to CA$10. Both perspectives can coexist. The key is that each investor has an explicit, dynamic story that directly connects what they believe about the business to a concrete price they are willing to pay.

Do you think there's more to the story for Kinross Gold? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Kinross Gold might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:K

Kinross Gold

Engages in the acquisition, exploration, and development of gold properties principally in the United States, Brazil, Chile, Canada, and Mauritania.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026