Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:ERO

Did Phase 1 Drilling Success Just Shift Ero Copper's (TSX:ERO) Investment Narrative?

Simply Wall St

Reviewed by Simply Wall St

- Ero Copper recently announced the completion and results of Phase 1 drilling at its Furnas Copper-Gold Project in Brazil, confirming extension of high-grade copper-gold mineralization to greater depths than previously identified.

- This expansion of mineralized zones, along with updated resource estimates, underpins forthcoming economic studies and signals a strengthened project outlook for the company.

- Now, we’ll explore how the expanded high-grade mineralization at Furnas could reshape Ero Copper’s overall investment narrative.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Ero Copper Investment Narrative Recap

To own shares in Ero Copper, you need to believe the company can translate a track record of technical progress, like expanding high-grade copper-gold mineralization at Furnas, into consistent operational performance and financial returns. While the recent drill results at Furnas bolster long-term project potential and could support future resource estimates and economic assessments, they do not immediately resolve the central short-term catalyst: delivering reliable production growth and meeting revised output guidance after prior disappointments. Material execution risk in ramping up new capacity and controlling costs remains the core challenge to watch in the coming quarters.

Among recent developments, the announcement of early commercial production at the Tucumã operation, effective July 1, 2025, stands out. With approximately 6,400 tonnes of copper produced in Q2 and ramp-up on track, this directly relates to near-term catalysts around achieving and sustaining higher output levels across Ero Copper’s asset base, reinforcing the importance of execution discipline alongside exploration success at Furnas.

By contrast, investors should also be aware of ongoing risks tied to Ero’s history of downward production guidance revisions, as even robust drill results at Furnas won’t...

Read the full narrative on Ero Copper (it's free!)

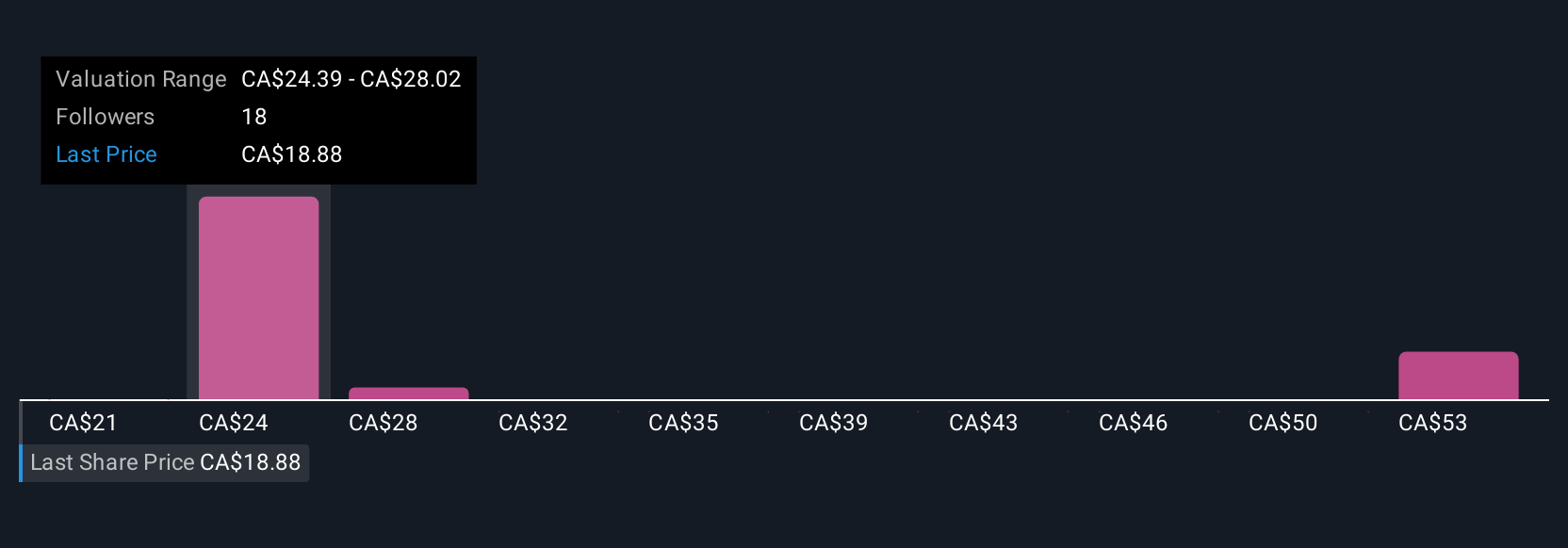

Ero Copper's narrative projects $996.0 million revenue and $298.7 million earnings by 2028. This requires 22.9% yearly revenue growth and a $156.0 million earnings increase from $142.7 million.

Uncover how Ero Copper's forecasts yield a CA$25.66 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Six private investors in the Simply Wall St Community peg Ero Copper’s fair value between CA$20.76 and CA$64.66, offering a wide range of outlooks. Consistent production growth remains a primary focus for many, with broader execution risk top of mind as you explore different perspectives on the company.

Explore 6 other fair value estimates on Ero Copper - why the stock might be worth over 2x more than the current price!

Build Your Own Ero Copper Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Ero Copper research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Ero Copper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ero Copper's overall financial health at a glance.

Searching For A Fresh Perspective?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Ero Copper might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:ERO

Ero Copper

Engages in the exploration, development, and production of mining projects in Brazil.

Undervalued with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor