- Canada

- /

- Food and Staples Retail

- /

- TSX:NWC

3 Canadian Dividend Stocks On TSX Yielding Up To 6.2%

Reviewed by Simply Wall St

Over the last 7 days, the Canadian market has risen by 1.0%, contributing to a remarkable 22% increase over the past year, with earnings forecasted to grow by 15% annually. In this thriving environment, dividend stocks offering attractive yields can be appealing for investors seeking both income and potential growth.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 6.64% | ★★★★★★ |

| Labrador Iron Ore Royalty (TSX:LIF) | 7.86% | ★★★★★☆ |

| Olympia Financial Group (TSX:OLY) | 7.17% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 5.14% | ★★★★★☆ |

| Enghouse Systems (TSX:ENGH) | 3.35% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 4.13% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 8.62% | ★★★★★☆ |

| Sun Life Financial (TSX:SLF) | 4.12% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.40% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.08% | ★★★★★☆ |

Click here to see the full list of 30 stocks from our Top TSX Dividend Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

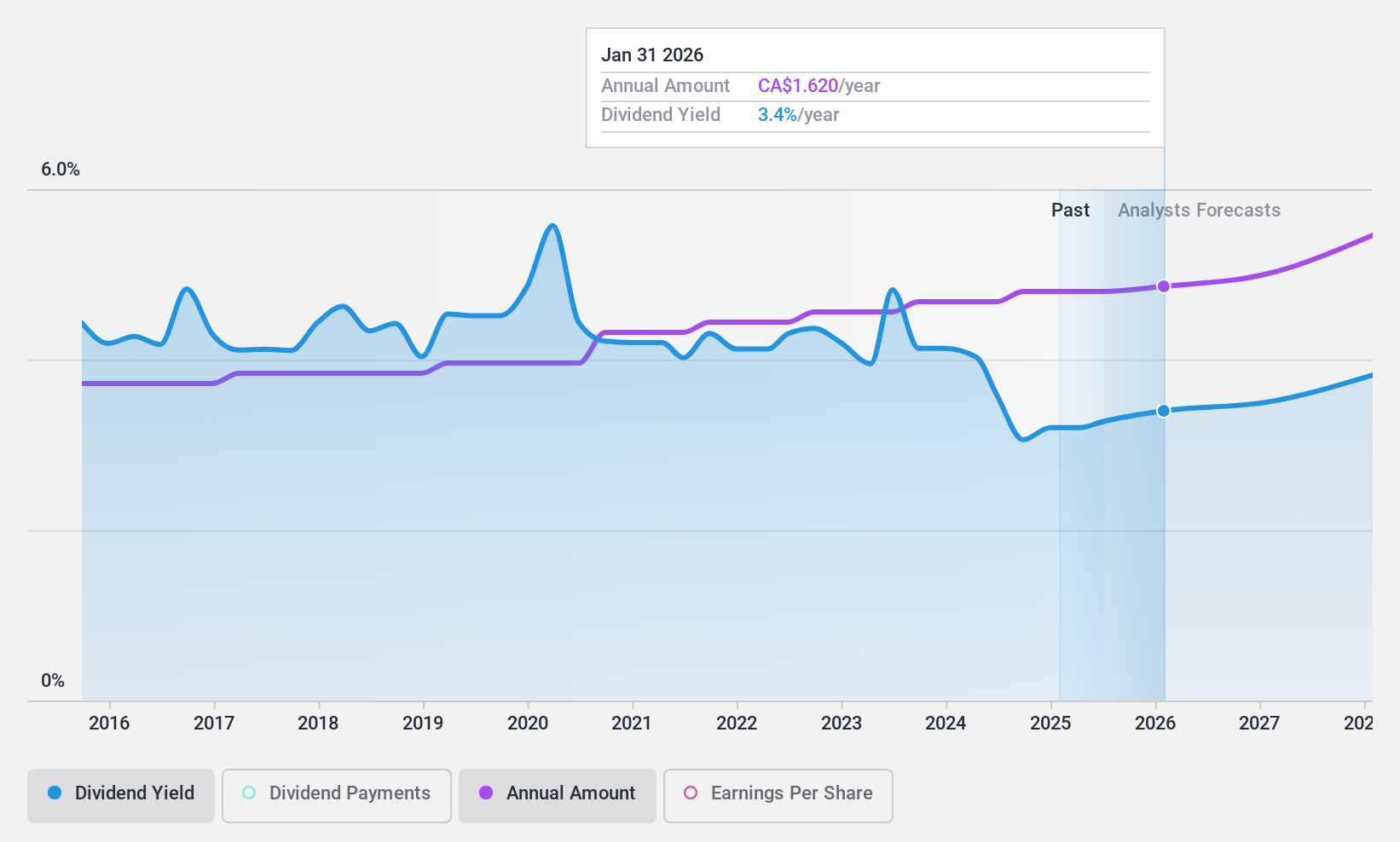

Canadian Natural Resources (TSX:CNQ)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Canadian Natural Resources Limited engages in the acquisition, exploration, development, production, marketing, and sale of crude oil, natural gas, and natural gas liquids (NGLs), with a market cap of approximately CA$105.91 billion.

Operations: Canadian Natural Resources Limited's revenue segments include Oil Sands Mining and Upgrading at CA$16.47 billion, Exploration and Production - North America at CA$18.15 billion, Midstream and Refining at CA$983 million, Exploration and Production - North Sea at CA$522 million, and Exploration and Production - Offshore Africa at CA$492 million.

Dividend Yield: 4.1%

Canadian Natural Resources offers a dividend yield of 4.08%, which is lower than the top 25% of Canadian dividend payers, but it maintains strong coverage with a payout ratio of 56.1% and cash payout ratio of 42.5%. The company has consistently increased dividends over the past decade, recently announcing a 7% increase to $0.5625 per share payable in January 2025. Earnings have shown modest growth, supporting stable and reliable dividend payments.

- Delve into the full analysis dividend report here for a deeper understanding of Canadian Natural Resources.

- Our comprehensive valuation report raises the possibility that Canadian Natural Resources is priced lower than what may be justified by its financials.

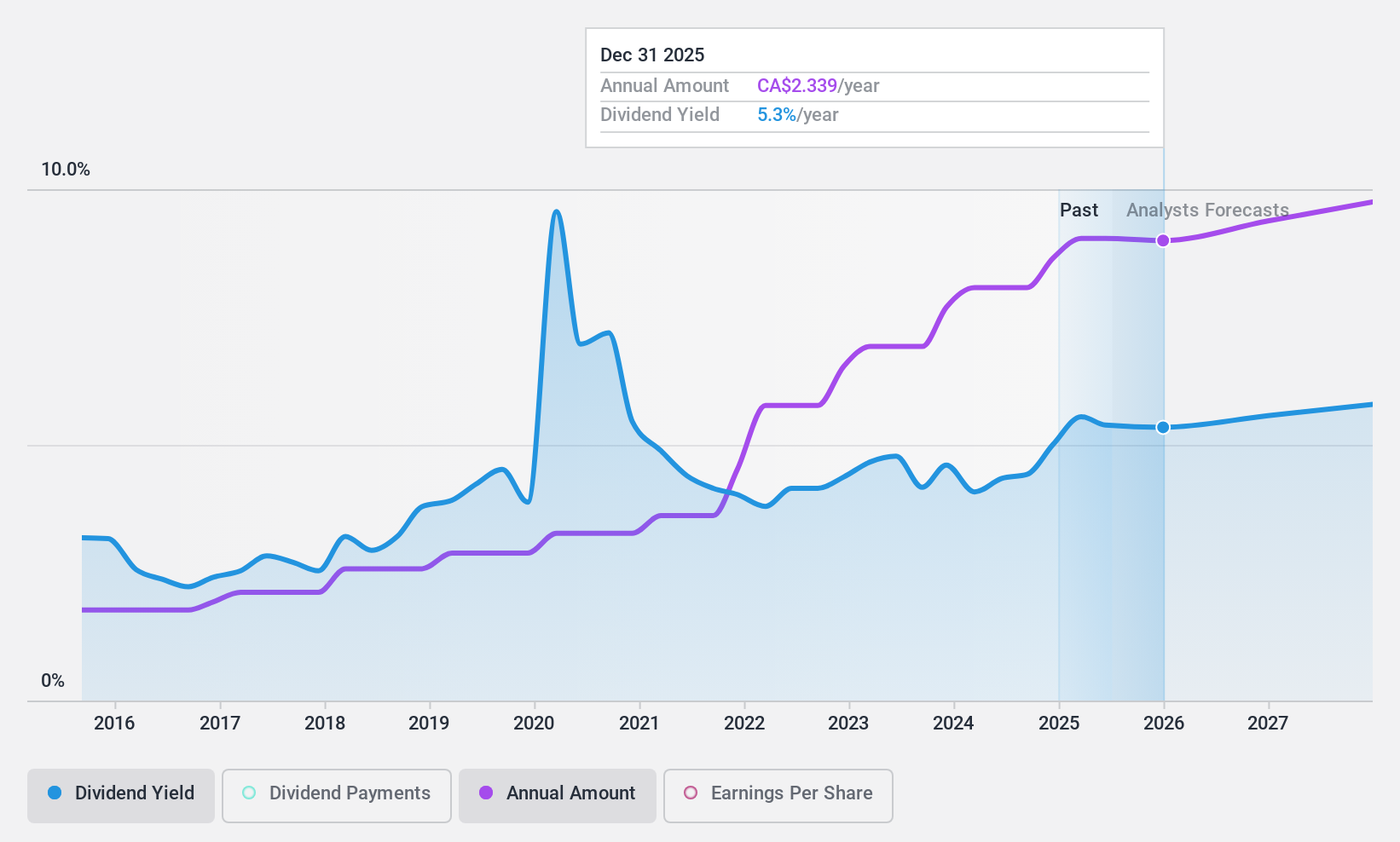

North West (TSX:NWC)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: The North West Company Inc. operates retail stores offering food and everyday products in rural and urban communities across northern Canada, rural Alaska, the South Pacific, and the Caribbean, with a market cap of CA$2.53 billion.

Operations: The North West Company Inc.'s revenue is primarily derived from its operations as a retailer of food and everyday products and services, generating CA$2.52 billion.

Dividend Yield: 3.1%

North West Company has a stable dividend history, with payments growing steadily over the past decade. Recent earnings showed modest growth, supporting its dividend sustainability with a payout ratio of 56.2% and cash payout ratio of 72.9%. Despite trading below estimated fair value, North West's dividend yield of 3.07% is lower than top-tier Canadian payers. A recent increase to CAD 0.40 per share reflects ongoing commitment to shareholders, though insider selling raises cautionary flags.

- Dive into the specifics of North West here with our thorough dividend report.

- The analysis detailed in our North West valuation report hints at an deflated share price compared to its estimated value.

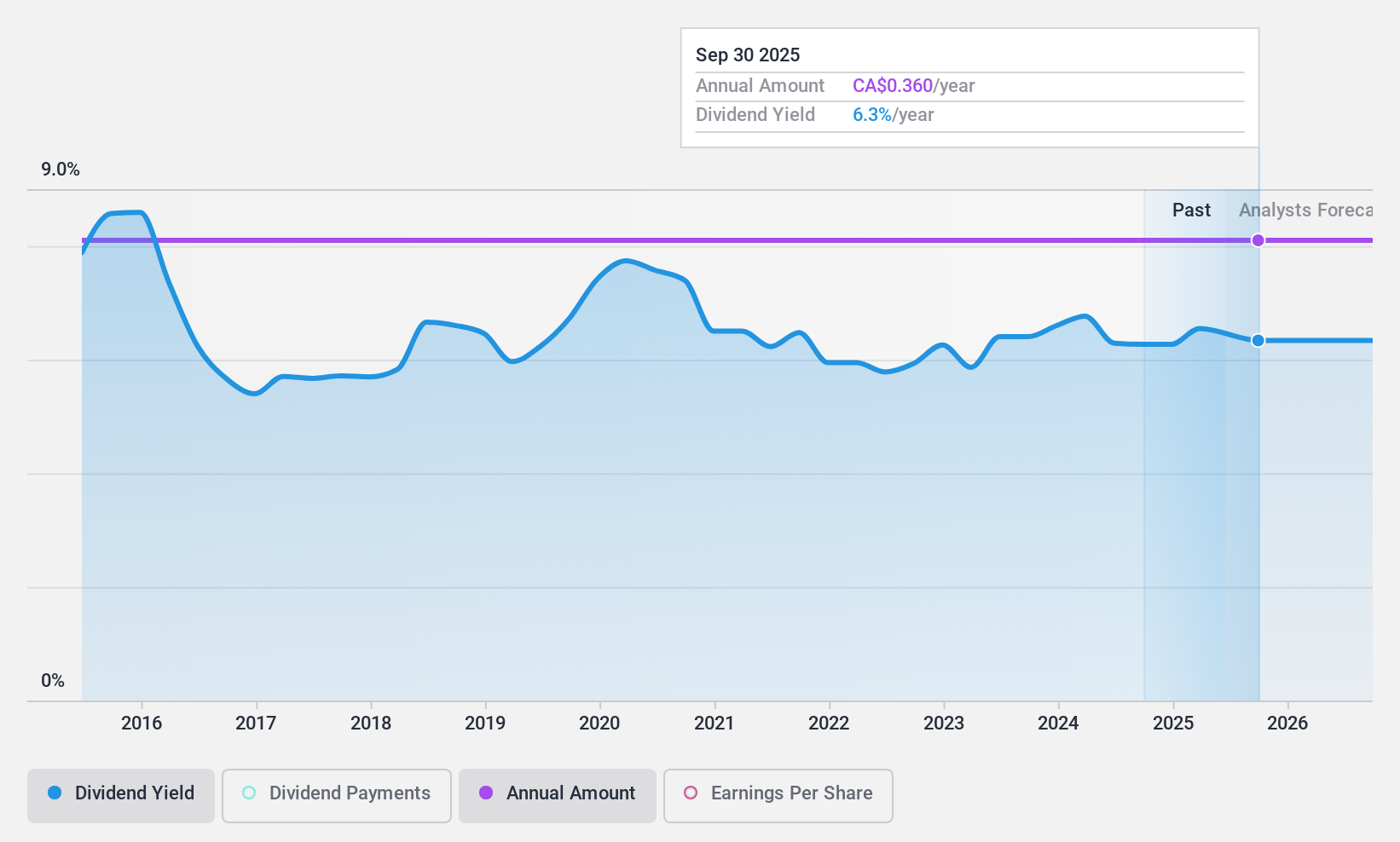

Rogers Sugar (TSX:RSI)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Rogers Sugar Inc. is involved in the refining, packaging, marketing, and distribution of sugar and maple products across Canada, the United States, Europe, and internationally with a market cap of CA$729.13 million.

Operations: Rogers Sugar Inc.'s revenue is comprised of CA$981.45 million from sugar and CA$225.32 million from maple products.

Dividend Yield: 6.2%

Rogers Sugar offers a high dividend yield at 6.25%, placing it among the top Canadian payers. However, its dividends are not covered by free cash flow, raising sustainability concerns despite a payout ratio of 86%. The company's earnings have declined recently, with net income falling to C$7.38 million in Q3 2024 from C$14.18 million the previous year. Additionally, shareholder dilution and volatile dividend history further complicate its appeal as a reliable dividend stock.

- Take a closer look at Rogers Sugar's potential here in our dividend report.

- In light of our recent valuation report, it seems possible that Rogers Sugar is trading behind its estimated value.

Key Takeaways

- Click here to access our complete index of 30 Top TSX Dividend Stocks.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if North West might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:NWC

North West

Through its subsidiaries, engages in the retail of food and everyday products and services to rural communities and urban neighborhood markets in northern Canada, rural Alaska, the South Pacific, and the Caribbean.

Flawless balance sheet established dividend payer.