Advertisement

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Macro Enterprises Inc. (CVE:MCR) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Macro Enterprises

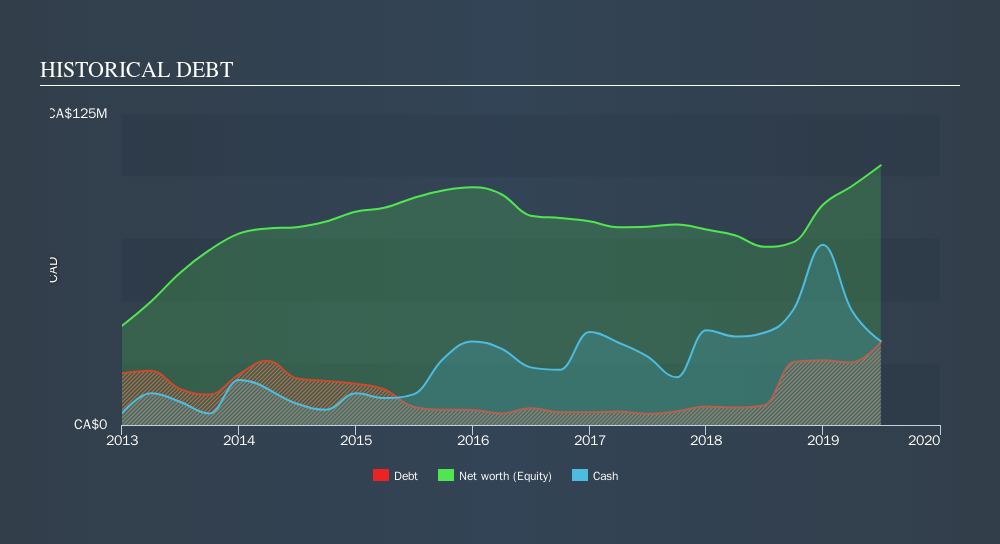

How Much Debt Does Macro Enterprises Carry?

The image below, which you can click on for greater detail, shows that at June 2019 Macro Enterprises had debt of CA$33.2m, up from CA$7.85m in one year. But it also has CA$33.7m in cash to offset that, meaning it has CA$569.0k net cash.

A Look At Macro Enterprises's Liabilities

According to the last reported balance sheet, Macro Enterprises had liabilities of CA$86.7m due within 12 months, and liabilities of CA$46.0m due beyond 12 months. Offsetting these obligations, it had cash of CA$33.7m as well as receivables valued at CA$87.8m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CA$11.2m.

Of course, Macro Enterprises has a market capitalization of CA$124.8m, so these liabilities are probably manageable. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. While it does have liabilities worth noting, Macro Enterprises also has more cash than debt, so we're pretty confident it can manage its debt safely.

Although Macro Enterprises made a loss at the EBIT level, last year, it was also good to see that it generated CA$49m in EBIT over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Macro Enterprises can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Macro Enterprises may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last year, Macro Enterprises saw substantial negative free cash flow, in total. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Summing up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Macro Enterprises has CA$569.0k in net cash. So we don't have any problem with Macro Enterprises's use of debt. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Macro Enterprises's earnings per share history for free.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSXV:MCR

Macro Enterprises

Macro Enterprises Inc. provides pipeline and facilities construction and maintenance services to the oil and gas industry in western Canada.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor