- Canada

- /

- Energy Services

- /

- TSX:TVK

TSX Growth Companies With High Insider Ownership March 2025

Reviewed by Simply Wall St

In 2025, the Canadian stock market has experienced volatility, with diversification emerging as a key theme amidst softened growth outlooks and broader market uncertainty. In this context, growth companies with high insider ownership can be appealing to investors seeking stability and potential upside, as these firms often reflect strong management confidence and alignment with shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Propel Holdings (TSX:PRL) | 36.5% | 35.8% |

| Robex Resources (TSXV:RBX) | 25.6% | 141.5% |

| Allied Gold (TSX:AAUC) | 17.7% | 85.1% |

| Vox Royalty (TSX:VOXR) | 12% | 83.3% |

| West Red Lake Gold Mines (TSXV:WRLG) | 13.5% | 76.8% |

| NTG Clarity Networks (TSXV:NCI) | 38.2% | 27.6% |

| goeasy (TSX:GSY) | 21.6% | 15.4% |

| Aritzia (TSX:ATZ) | 17.6% | 41.1% |

| Burcon NutraScience (TSX:BU) | 16.4% | 152.2% |

| CHAR Technologies (TSXV:YES) | 10.8% | 63% |

Here's a peek at a few of the choices from the screener.

goeasy (TSX:GSY)

Simply Wall St Growth Rating: ★★★★★☆

Overview: goeasy Ltd. operates in Canada, offering non-prime leasing and lending services through its easyhome, easyfinancial, and LendCare brands, with a market cap of CA$2.45 billion.

Operations: The company's revenue is derived from its Easyhome segment, contributing CA$152.88 million, and its Easyfinancial segment, generating CA$1.37 billion.

Insider Ownership: 21.6%

goeasy Ltd. demonstrates strong growth potential with revenue forecasted to grow at 27.7% annually, outpacing the Canadian market. Recent insider activity shows substantial buying, indicating confidence in its prospects. The recent appointment of Dan Rees as CEO brings valuable financial expertise from Scotiabank, potentially enhancing goeasy's strategic initiatives and operational efficiencies. While earnings are projected to grow at 15.4% per year, the dividend is not well covered by free cash flows despite a recent increase to $5.84 per share annually.

- Dive into the specifics of goeasy here with our thorough growth forecast report.

- Our comprehensive valuation report raises the possibility that goeasy is priced lower than what may be justified by its financials.

North American Construction Group (TSX:NOA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: North American Construction Group Ltd. offers mining and heavy civil construction services across the resource development and industrial construction sectors in Australia, Canada, and the United States, with a market cap of CA$688.82 million.

Operations: North American Construction Group Ltd.'s revenue segments focus on providing services in the mining and heavy civil construction industries within resource development and industrial construction sectors across Australia, Canada, and the United States.

Insider Ownership: 11.1%

North American Construction Group exhibits growth potential with earnings forecasted to grow significantly at 41.67% annually, surpassing the Canadian market average. Despite a recent decline in profit margins and net income, analysts anticipate a substantial price increase of 57.3%. However, insider activity shows significant selling over the past quarter. The company's dividend yield of 2.03% is not well covered by free cash flows, raising concerns about its sustainability amidst high debt interest obligations.

- Click here and access our complete growth analysis report to understand the dynamics of North American Construction Group.

- The analysis detailed in our North American Construction Group valuation report hints at an deflated share price compared to its estimated value.

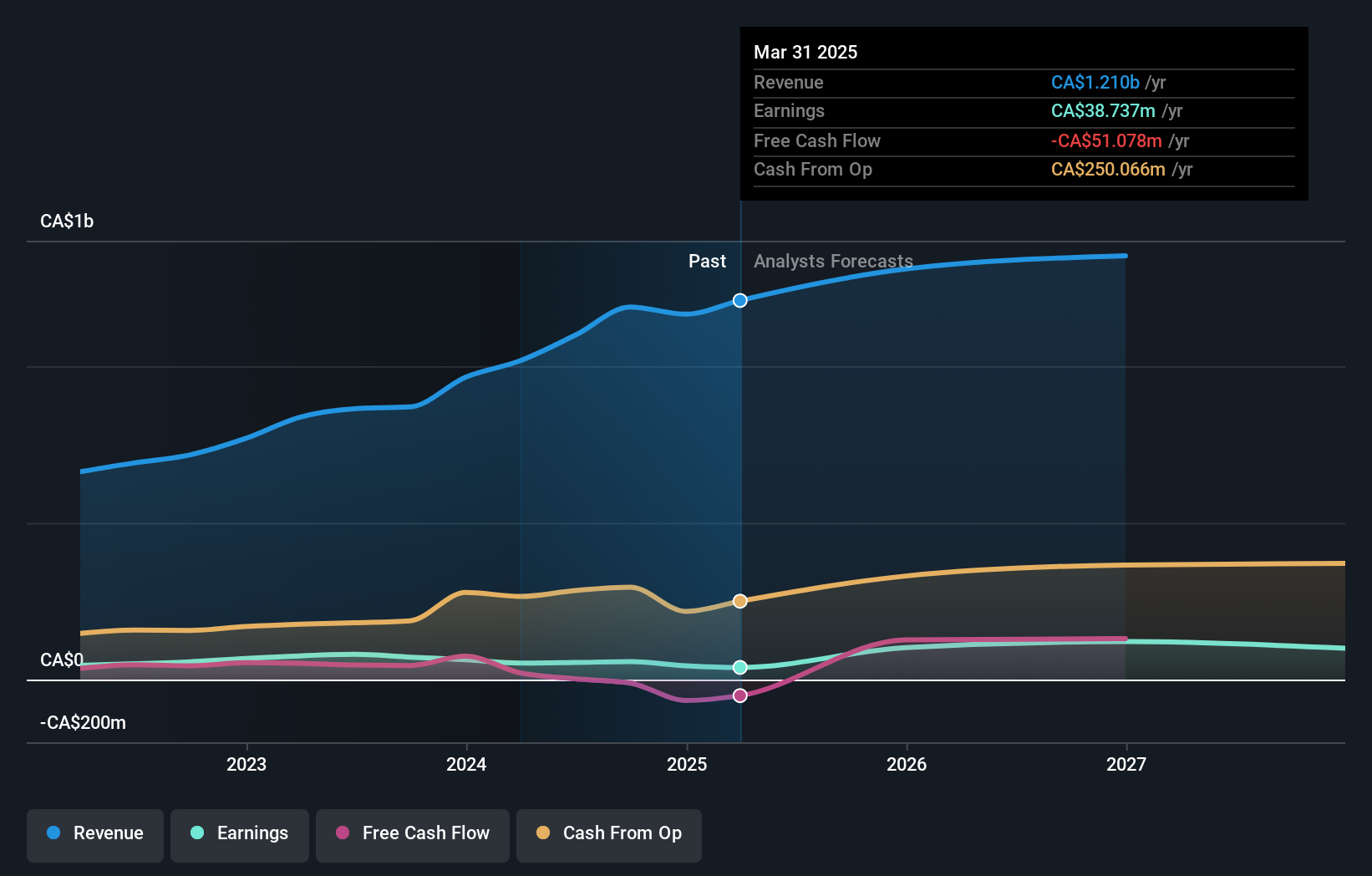

TerraVest Industries (TSX:TVK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: TerraVest Industries Inc. manufactures and sells goods and services across various sectors including agriculture, mining, energy, chemicals, utilities, transportation, and construction in Canada, the United States, and internationally with a market cap of CA$2.75 billion.

Operations: The company's revenue is derived from several segments, including CA$202.65 million from Service, CA$97.26 million from Processing Equipment, CA$280.72 million from Compressed Gas Equipment, and CA$341.95 million from HVAC and Containment Equipment.

Insider Ownership: 21%

TerraVest Industries demonstrates strong growth potential, with revenue and earnings forecasted to grow significantly at 38.8% and 30.6% per year respectively, outpacing the Canadian market averages. Recent earnings showed a substantial increase in net income to C$28.74 million from C$17.38 million year-over-year, alongside a quarterly dividend of C$0.175 per share declared for April 2025. The stock trades slightly below its estimated fair value with no significant insider trading activity reported recently.

- Delve into the full analysis future growth report here for a deeper understanding of TerraVest Industries.

- In light of our recent valuation report, it seems possible that TerraVest Industries is trading beyond its estimated value.

Seize The Opportunity

- Dive into all 35 of the Fast Growing TSX Companies With High Insider Ownership we have identified here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade TerraVest Industries, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TerraVest Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TVK

TerraVest Industries

Manufactures and sells goods and services to agriculture, mining, energy production and distribution, chemical, utilities, transportation and construction, and other markets in Canada, the United States, and internationally.

Flawless balance sheet with high growth potential.