Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:PPL

Will Pembina Pipeline's (TSX:PPL) Billion-Dollar Export Expansion Redefine Its Long-Term Growth Narrative?

Simply Wall St

Reviewed by Simply Wall St

- Earlier this week, Pembina Pipeline announced over C$1 billion in conventional pipeline expansions secured by long-term contracts, along with a C$145 million upgrade to its Prince Rupert Terminal to strengthen propane export capabilities to Asia.

- This marks a significant move to capture rising demand in Asian markets, but also raises near-term risks around capital outlays and margin pressures from increased competition.

- To assess the impact of Pembina's major pipeline investment, we'll explore how scaling export capacity could alter the company's long-term earnings outlook.

Find companies with promising cash flow potential yet trading below their fair value.

Pembina Pipeline Investment Narrative Recap

To invest in Pembina Pipeline, you need confidence in the company’s ability to capitalize on export demand and successfully manage large-scale, capital-intensive projects. The recent C$1 billion pipeline expansions and Prince Rupert Terminal upgrade could increase export earnings potential, but in the short term, project spending and heightened competition are the main factors most likely to sway shares; at present, the direct impact on the company’s largest near-term catalyst, securing new long-term export contracts, appears moderate.

Of recent developments, the long-term tolling agreement announced with AltaGas Ltd. closely connects to Pembina’s export ambitions highlighted in this week’s expansion news. By locking in 30,000 barrels per day of liquids export capacity, Pembina strengthens revenue visibility and utilization rates, which supports the thesis that access to international markets remains a critical earnings driver. Yet, unlike the project growth story, investors should also be aware that rising competition and evolving rate structures could directly affect margins if...

Read the full narrative on Pembina Pipeline (it's free!)

Pembina Pipeline's narrative projects CA$8.1 billion revenue and CA$1.9 billion earnings by 2028. This requires 0.0% yearly revenue growth and a CA$0.2 billion earnings increase from CA$1.7 billion.

Uncover how Pembina Pipeline's forecasts yield a CA$58.06 fair value, a 10% upside to its current price.

Exploring Other Perspectives

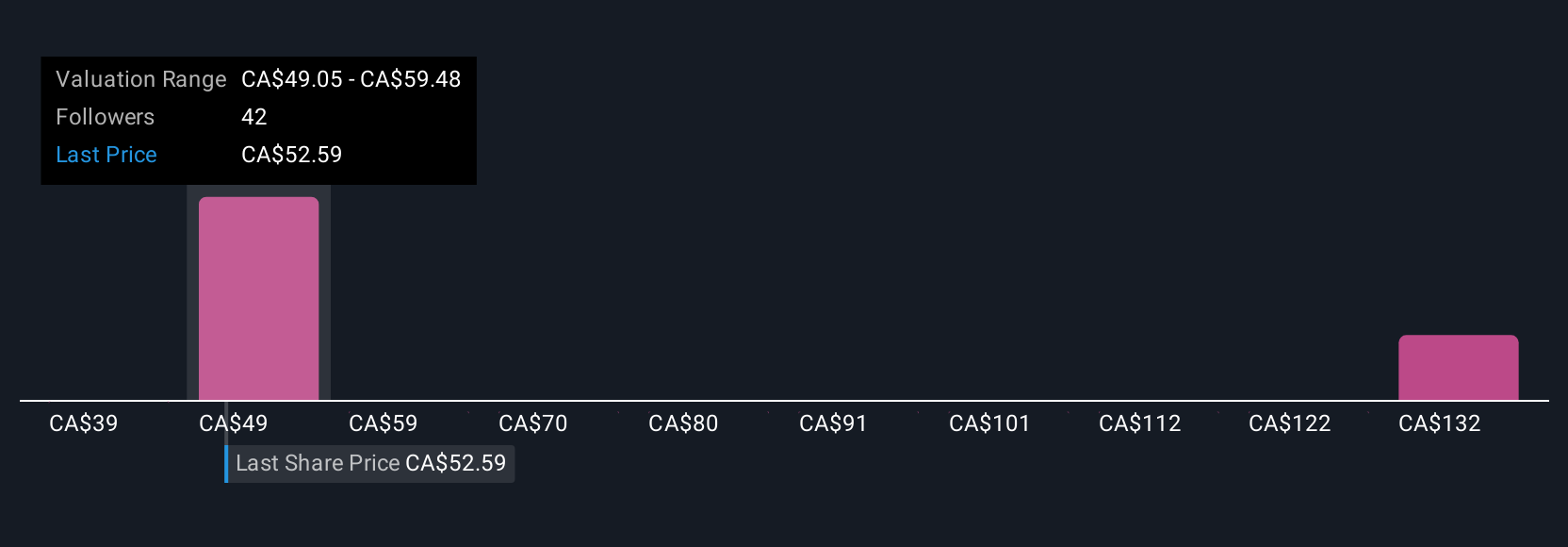

Seven Simply Wall St Community members provided fair value estimates for Pembina’s shares, with values spanning from C$38.63 to C$142.11. While you review these diverse viewpoints, keep in mind that elevated capital expenditures may strain near-term financial flexibility and influence the company’s long-range earnings profile.

Explore 7 other fair value estimates on Pembina Pipeline - why the stock might be worth 27% less than the current price!

Build Your Own Pembina Pipeline Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Pembina Pipeline research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Pembina Pipeline research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Pembina Pipeline's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 11 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:PPL

Average dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|74.9% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|35.1% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|1.5% undervalued

BL

Community Contributor