- Canada

- /

- Oil and Gas

- /

- TSX:POU

Is Paramount Resources (TSX:POU) Undervalued After Its Recent Share Price Pullback?

Reviewed by Simply Wall St

Paramount Resources (TSX:POU) has quietly pulled back this week, with the stock down about 4% over the past day and 7% over the past week, despite strong 1 year gains.

See our latest analysis for Paramount Resources.

That pullback sits against a much stronger backdrop, with the 1 year total shareholder return above 55% and the 5 year total shareholder return above 1,100%. This suggests long term momentum remains firmly intact even as short term share price sentiment cools.

If this kind of volatility has you thinking beyond a single energy name, it could be a good moment to explore fast growing stocks with high insider ownership as potential new ideas for your watchlist.

With growth stalling this year and the share price already sitting above analyst targets, investors now face a key question: Is Paramount quietly undervalued on its long term assets, or is the market already pricing in future gains?

Price-to-Earnings of 2.5x: Is it justified?

On a price-to-earnings multiple of just 2.5x at a last close of CA$23.67, Paramount Resources looks deeply discounted relative to both the wider Canadian market and its oil and gas peers.

The price-to-earnings ratio compares what investors pay today with the company’s current earnings, making it a central yardstick for mature, profitable energy producers whose cash flows are closely tied to commodity cycles.

With earnings up more than 280% over the past year and return on equity above 50%, such a low multiple suggests the market is heavily discounting the durability of recent profits rather than paying up for them.

Against an industry average P/E of 14.8x and a peer average of 37.9x, Paramount’s 2.5x multiple stands out as aggressively cheap. It also trades at roughly half the estimated fair price-to-earnings ratio of 5x, a level the market could move toward if it gains confidence in future earnings.

Explore the SWS fair ratio for Paramount Resources

Result: Price-to-earnings of 2.5x (UNDERVALUED).

However, sustained revenue and earnings declines, alongside the share price trading above analyst targets, could limit upside if commodity conditions or execution disappoint.Find out about the key risks to this Paramount Resources narrative.

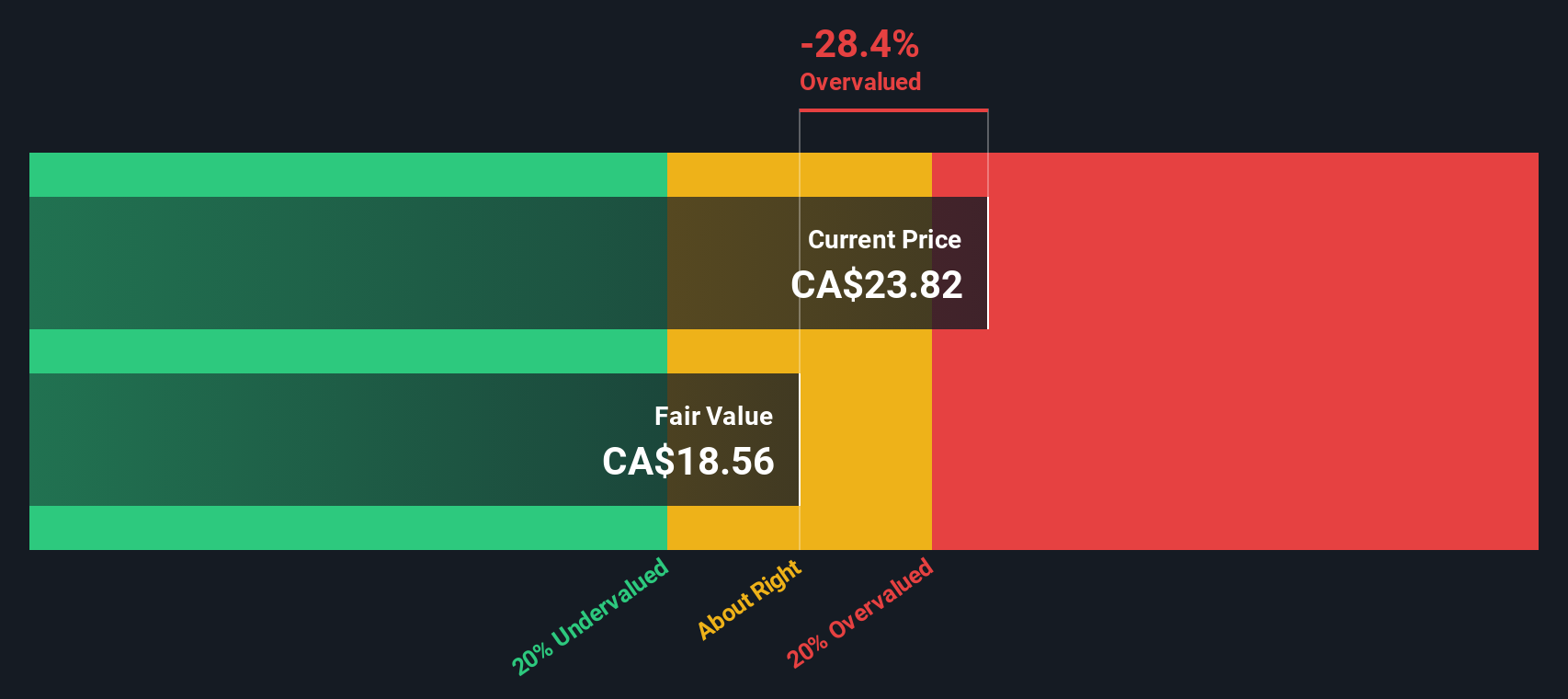

Another View on Value

Our SWS DCF model tells a different story. On this view, Paramount looks overvalued, with the share price around CA$23.67 versus an estimated fair value near CA$18.51. If cash flows normalise, are investors paying up today for profits that may prove temporary?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Paramount Resources for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 915 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Paramount Resources Narrative

If you see the story differently, or want to dig into the numbers yourself, you can easily build your own view in just a few minutes: Do it your way.

A great starting point for your Paramount Resources research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, you could scan other opportunities on Simply Wall Street that may sharpen your portfolio and help uncover your next standout winner.

- Consider potential multi-baggers early by focusing on these 3633 penny stocks with strong financials with solid fundamentals and room to scale.

- Explore the next wave of innovation by targeting these 25 AI penny stocks that influence how industries use automation and data.

- Review these 13 dividend stocks with yields > 3% that combine attractive yields with sustainable payout profiles to strengthen your income stream.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:POU

Paramount Resources

An energy company, explores for and develops conventional and unconventional petroleum and natural gas reserves and resources in Canada.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)