Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:FRU

We Wouldn't Be Too Quick To Buy Freehold Royalties Ltd. (TSE:FRU) Before It Goes Ex-Dividend

Readers hoping to buy Freehold Royalties Ltd. (TSE:FRU) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date is usually set to be one business day before the record date which is the cut-off date on which you must be present on the company's books as a shareholder in order to receive the dividend. The ex-dividend date is important as the process of settlement involves two full business days. So if you miss that date, you would not show up on the company's books on the record date. Accordingly, Freehold Royalties investors that purchase the stock on or after the 28th of September will not receive the dividend, which will be paid on the 16th of October.

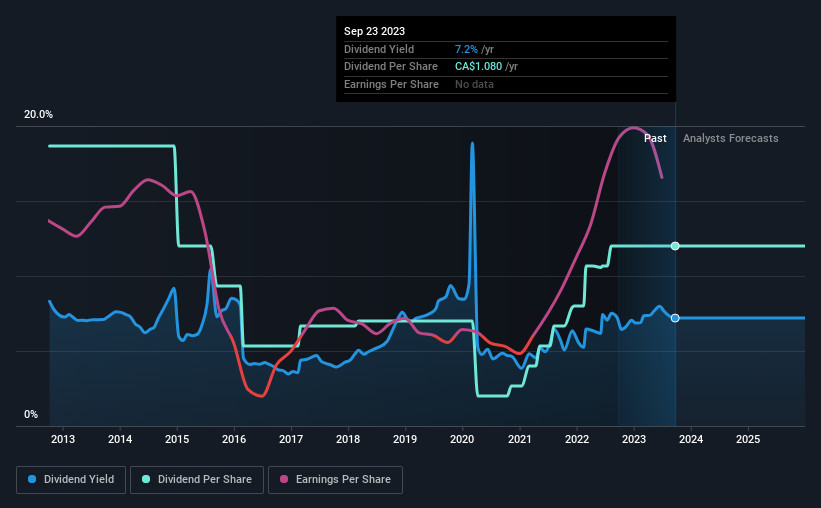

The company's upcoming dividend is CA$0.09 a share, following on from the last 12 months, when the company distributed a total of CA$1.08 per share to shareholders. Based on the last year's worth of payments, Freehold Royalties stock has a trailing yield of around 7.2% on the current share price of CA$15.01. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! We need to see whether the dividend is covered by earnings and if it's growing.

Check out our latest analysis for Freehold Royalties

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Freehold Royalties paid out 101% of its earnings, which is more than we're comfortable with, unless there are mitigating circumstances. A useful secondary check can be to evaluate whether Freehold Royalties generated enough free cash flow to afford its dividend. Freehold Royalties paid out more free cash flow than it generated - 162%, to be precise - last year, which we think is concerningly high. It's hard to consistently pay out more cash than you generate without either borrowing or using company cash, so we'd wonder how the company justifies this payout level.

As Freehold Royalties's dividend was not well covered by either earnings or cash flow, we would be concerned that this dividend could be at risk over the long term.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. It's encouraging to see Freehold Royalties has grown its earnings rapidly, up 59% a year for the past five years. Earnings per share have been growing rapidly, but the company is paying out an uncomfortably high percentage of its earnings as dividends. Generally, when a company is growing this quickly and paying out all of its earnings as dividends, it can suggest either that the company is borrowing heavily to fund its growth, or that earnings growth is likely to slow due to lack of reinvestment.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Freehold Royalties's dividend payments per share have declined at 4.3% per year on average over the past 10 years, which is uninspiring. Freehold Royalties is a rare case where dividends have been decreasing at the same time as earnings per share have been improving. It's unusual to see, and could point to unstable conditions in the core business, or more rarely an intensified focus on reinvesting profits.

Final Takeaway

Has Freehold Royalties got what it takes to maintain its dividend payments? Earnings per share have been growing, despite the company paying out a concerningly high percentage of its earnings and cashflow. We struggle to see how a company paying out so much of its earnings and cash flow will be able to sustain its dividend in a downturn, or reinvest enough into its business to continue growing earnings without borrowing heavily. Overall it doesn't look like the most suitable dividend stock for a long-term buy and hold investor.

Although, if you're still interested in Freehold Royalties and want to know more, you'll find it very useful to know what risks this stock faces. Our analysis shows 2 warning signs for Freehold Royalties and you should be aware of them before buying any shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:FRU

Freehold Royalties

Acquires and manages royalty interests in the crude oil, natural gas, natural gas liquids, and potash properties in Canada and the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor