Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:CR

Analysts Have Just Cut Their Crew Energy Inc. (TSE:CR) Revenue Estimates By 10%

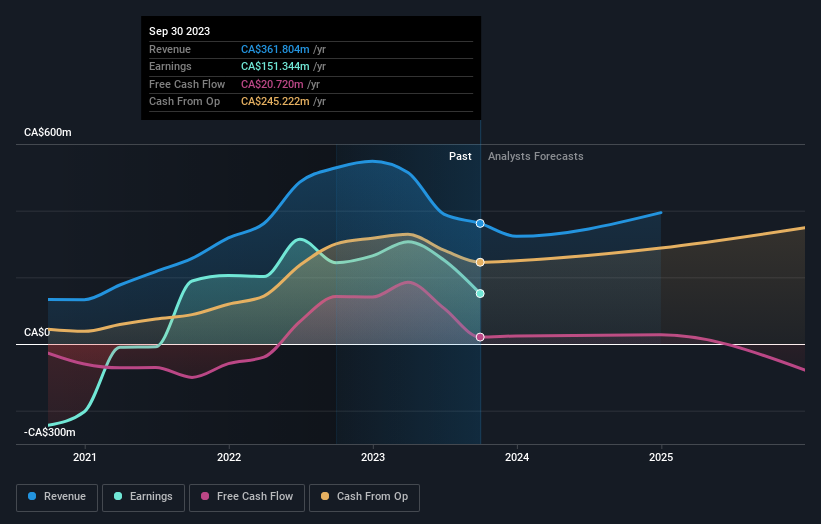

The latest analyst coverage could presage a bad day for Crew Energy Inc. (TSE:CR), with the analysts making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic.

After this downgrade, Crew Energy's three analysts are now forecasting revenues of CA$394m in 2024. This would be a notable 8.9% improvement in sales compared to the last 12 months. Statutory earnings per share are supposed to descend 12% to CA$0.86 in the same period. Prior to this update, the analysts had been forecasting revenues of CA$438m and earnings per share (EPS) of CA$0.87 in 2024. Indeed we can see that the consensus opinion has undergone some fundamental changes following the recent consensus updates, with a measurable cut to revenues and some minor tweaks to earnings numbers.

See our latest analysis for Crew Energy

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that Crew Energy's revenue growth is expected to slow, with the forecast 7.1% annualised growth rate until the end of 2024 being well below the historical 23% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 5.3% annually. Even after the forecast slowdown in growth, it seems obvious that Crew Energy is also expected to grow faster than the wider industry.

The Bottom Line

The most obvious conclusion from this consensus update is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Crew Energy after today.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Crew Energy going out to 2024, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:CR

Crew Energy

Engages in the acquisition, exploration, development, and production of crude oil, natural gas, and natural gas liquids (NGL) in Canada.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor