Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:FRU

Exploring Cardinal Energy And 2 Other Emerging Small Caps with Strong Potential

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market shows resilience amid global tariff uncertainties, with the TSX recently gaining over 2%, small-cap stocks are capturing investor interest due to their potential for growth in a mixed economic landscape. In this environment, discovering promising small caps like Cardinal Energy involves identifying companies that can navigate inflationary pressures and leverage favorable fiscal and monetary policies to drive future success.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 4.89% | 13.46% | 20.23% | ★★★★★★ |

| Yellow Pages | NA | -11.96% | -15.73% | ★★★★★★ |

| Pinetree Capital | 0.24% | 59.68% | 61.83% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 9.16% | 15.11% | ★★★★★★ |

| Genesis Land Development | 46.48% | 30.46% | 55.37% | ★★★★★☆ |

| Itafos | 28.17% | 11.62% | 53.49% | ★★★★★☆ |

| Mako Mining | 8.59% | 38.81% | 59.80% | ★★★★★☆ |

| Corby Spirit and Wine | 59.18% | 8.79% | -5.67% | ★★★★☆☆ |

| Senvest Capital | 81.59% | -11.73% | -12.63% | ★★★★☆☆ |

| Dundee | 3.91% | -36.42% | 49.66% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

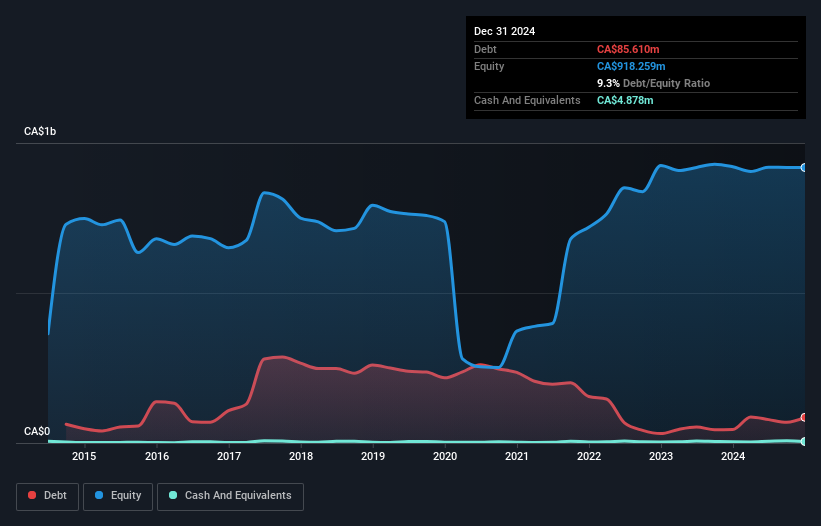

Cardinal Energy (TSX:CJ)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Cardinal Energy Ltd. is involved in acquiring, exploring, developing, optimizing, and producing petroleum and natural gas across Alberta, British Columbia, and Saskatchewan in Canada with a market cap of CA$972.44 million.

Operations: Cardinal Energy's primary revenue stream is derived from its oil and gas exploration and production segment, generating CA$497.38 million.

Cardinal Energy, a smaller player in the oil and gas sector, has shown impressive resilience with earnings growth of 4.6% over the past year, outpacing the industry's -22.4%. The company trades at a significant discount to its estimated fair value by 75.5%, suggesting potential upside for investors. Its debt management is commendable, with a reduction in debt-to-equity ratio from 29.5% to 9.3% over five years and an interest coverage ratio of 26x EBIT, indicating strong financial health despite forecasts of declining earnings by an average of 47.4% annually for the next three years.

- Navigate through the intricacies of Cardinal Energy with our comprehensive health report here.

Gain insights into Cardinal Energy's past trends and performance with our Past report.

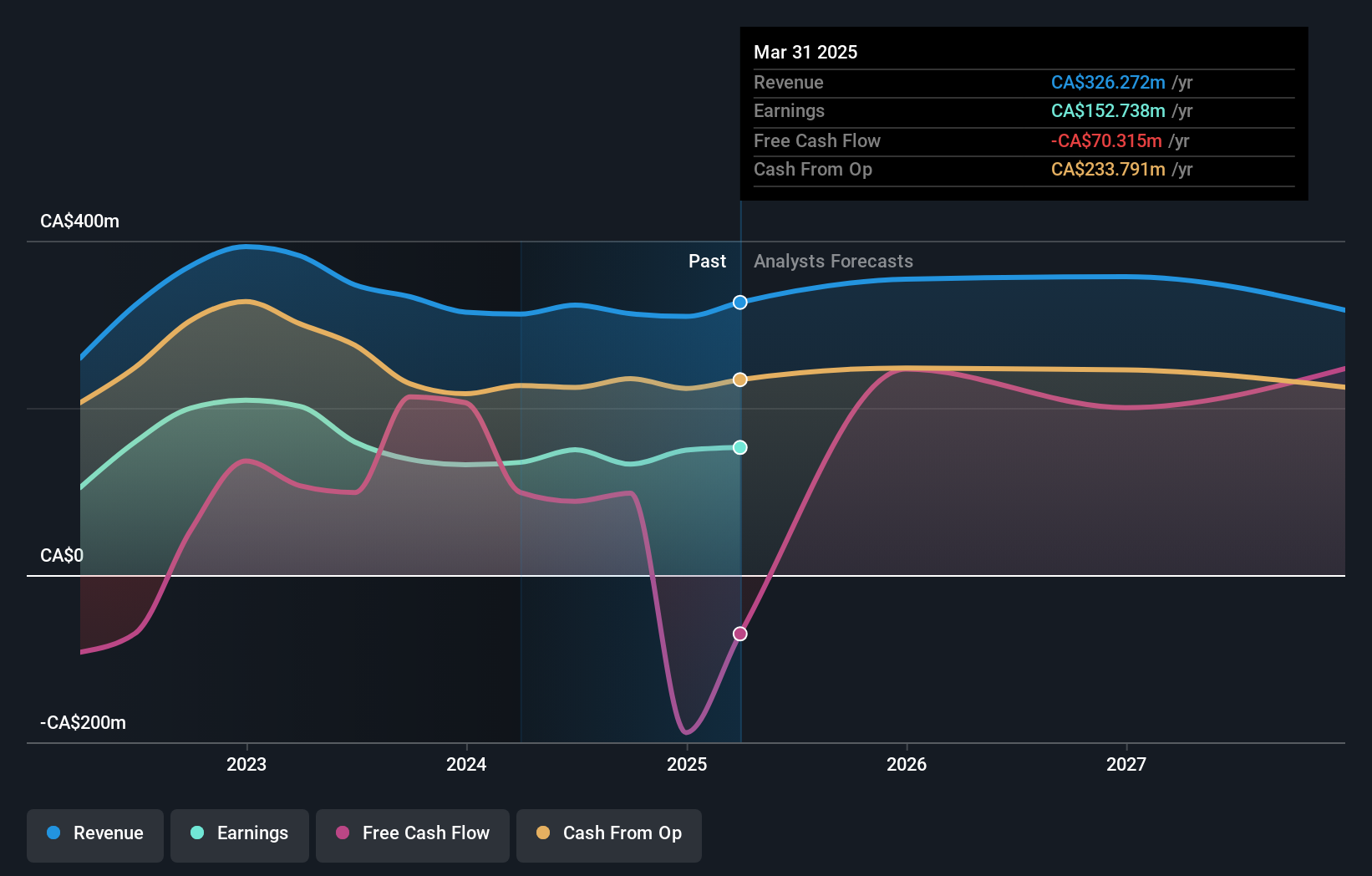

Freehold Royalties (TSX:FRU)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Freehold Royalties Ltd. focuses on acquiring and managing royalty interests in crude oil, natural gas, natural gas liquids, and potash properties across Canada and the United States, with a market cap of approximately CA$1.93 billion.

Operations: Revenue for Freehold Royalties is primarily generated from its oil and gas exploration and production segment, amounting to CA$309.48 million. The company's financial performance is characterized by a focus on maximizing returns from its royalty interests in the energy sector across North America.

Freehold Royalties has been making waves with its strategic moves and robust financials. Its net debt to equity ratio stands at a satisfactory 27.4%, showcasing prudent financial management over the past five years, despite an increase from 15.4%. The company reported earnings growth of 13% last year, outpacing the oil and gas industry's downturn of -22%. With EBIT covering interest payments by nearly 12 times, Freehold's strong position is further bolstered by recent production increases to over 15,000 boe/d. As it eyes acquisitions and boosts liquid production this year, Freehold seems poised for continued operational strength.

- Unlock comprehensive insights into our analysis of Freehold Royalties stock in this health report.

Examine Freehold Royalties' past performance report to understand how it has performed in the past.

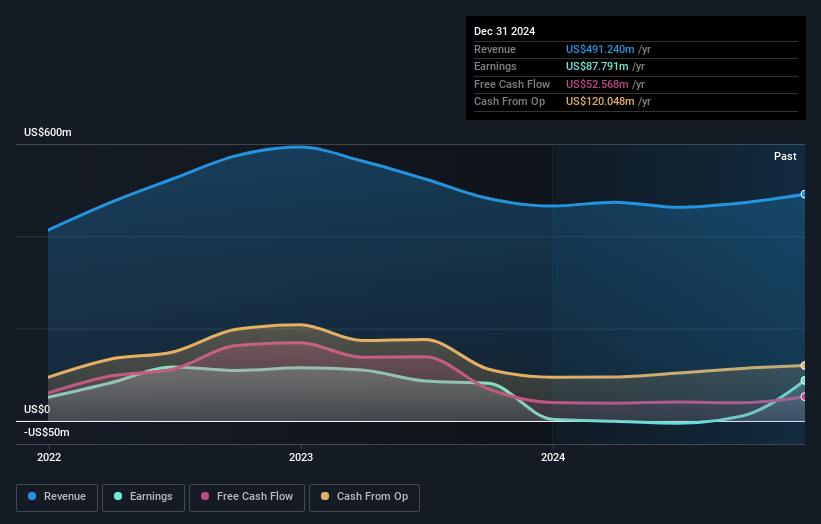

Itafos (TSXV:IFOS)

Simply Wall St Value Rating: ★★★★★☆

Overview: Itafos Inc. is a company that specializes in phosphate and specialty fertilizers, with a market capitalization of CA$423.43 million.

Operations: The company generates revenue primarily from its Conda segment, contributing $467.78 million, while the Arraias segment adds $23.46 million.

Itafos, a nimble player in the Canadian market, has demonstrated remarkable financial agility. Its earnings surged by 2173.8% last year, outpacing the chemicals industry average of -5.8%. The company’s debt to equity ratio improved significantly from 148.5% to 28.2% over five years, reflecting prudent financial management with interest payments well covered at 23 times EBIT. Trading at a substantial discount of 42.4% below estimated fair value and boasting high-quality earnings, Itafos also declared a special dividend following its Araxa project sale, highlighting robust cash flow with US$491 million in sales and US$87 million net income for 2024.

- Click to explore a detailed breakdown of our findings in Itafos' health report.

Gain insights into Itafos' historical performance by reviewing our past performance report.

Taking Advantage

- Unlock our comprehensive list of 37 TSX Undiscovered Gems With Strong Fundamentals by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:FRU

Freehold Royalties

Acquires and manages royalty interests in the crude oil, natural gas, natural gas liquids, and potash properties in Canada and the United States.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.0% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|5.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor