- Canada

- /

- Oil and Gas

- /

- TSX:ARX

ARC Resources (TSX:ARX) Confirms Dividend and Announces Major Share Buyback, Signaling Strong Financial Health

Reviewed by Simply Wall St

ARC Resources(TSX:ARX) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a strong operational performance with Q2 production reaching 330,000 BOE per day, and a significant undervaluation based on discounted cash flow analysis. In the discussion that follows, we will explore ARC Resources' core advantages, critical issues, potential growth strategies, and key risks to provide a comprehensive overview of the company's current business situation.

Navigate through the intricacies of ARC Resources with our comprehensive report here.

Strengths: Core Advantages Driving Sustained Success For ARC Resources

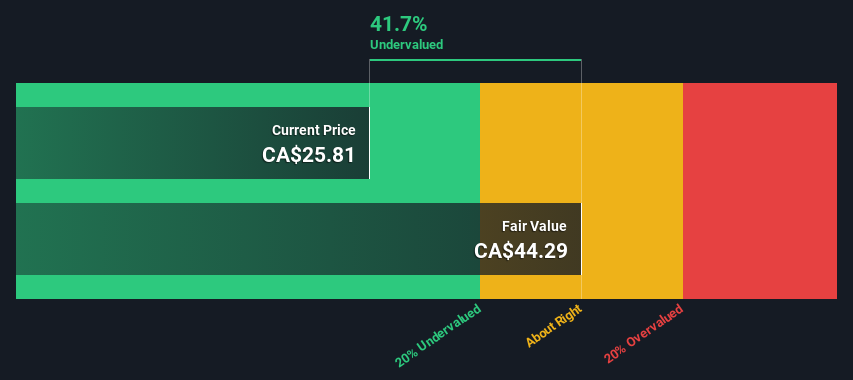

ARC Resources has demonstrated strong operational performance, with Q2 production reaching 330,000 BOE per day, aligning with the upper end of guidance. This highlights the company's execution capabilities. The team’s efficiency in completing major turnarounds on schedule and within budget further underscores their operational excellence. Additionally, the innovative well design in Upper Montney has reduced the full cycle breakeven to approximately CA$1.10 per Mcf, enhancing cost efficiency. Financially, ARC has returned 115% of free cash flow to shareholders through share repurchases and dividends, indicating strong financial management. Notably, ARX is currently trading at CA$22.46, significantly below its estimated fair value of CA$66.94, indicating that it is undervalued based on discounted cash flow analysis. This suggests a strong market positioning and potential for significant upside.

To dive deeper into how ARC Resources's valuation metrics are shaping its market position, check out our detailed analysis of ARC Resources's Valuation.

Weaknesses: Critical Issues Affecting ARC Resources's Performance and Areas For Growth

ARC Resources faces notable challenges. The company's production in Q2 was 330,000 BOEs per day, which is expected to be the lowest for the year, indicating a potential issue in maintaining production levels. Natural gas prices have been low, averaging CA$1.40 at AECO in Canada and CA$1.90 at Henry Hub in the U.S., impacting revenue. Additionally, net debt increased slightly to CA$1.5 billion as capital investments and dividends exceeded cash flow. Comparatively, while ARC's Price-To-Earnings Ratio (11.5x) is better than the peer average (18.1x) and the Canadian Oil and Gas industry average (11.7x), the company’s current net profit margins of 22.2% are lower than last year’s 34.5%, indicating a decline in profitability.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

ARC Resources has several opportunities to leverage for growth. The upcoming Attachie Phase 1 project, expected to come online later this year, represents a significant positive change for the company. This expansion could substantially increase production capacity and revenue. Additionally, the anticipated ramp-up of LNG Canada will drive a material increase in natural gas demand, presenting a lucrative market opportunity. Strategic partnerships, such as the new framework agreement exempting ARC from the disturbance cap for Attachie, further enhance its operational flexibility and potential for growth. These initiatives, coupled with a forecasted earnings growth of 23.7% per year, position ARC to capitalize on emerging market opportunities effectively.

To gain deeper insights into ARC Resources's historical performance, explore our detailed analysis of past performance.

Threats: Key Risks and Challenges That Could Impact ARC Resources's Success

ARC Resources faces several external threats that could impact its success. Market volatility, particularly the challenging near-term outlook for AECO, poses a significant risk. Competitive pressures are also evident, with the company not meeting total cycle returns below CA$1 per Mcf. Regulatory risks remain a concern, as ARC’s inclusion in a pilot program is tied to its commitment to responsible energy production, which could impose additional compliance costs. Additionally, the company's dividend track record has been unstable, with payments being volatile over the past 10 years. This instability, coupled with lower profit margins compared to the previous year, could affect investor confidence and long-term financial stability.

Conclusion

ARC Resources is well-positioned for future growth, driven by its strong operational performance and innovative cost-saving measures, such as the advanced well design in Upper Montney. While facing challenges like low natural gas prices and increased net debt, the company has significant opportunities ahead, including the Attachie Phase 1 project and the anticipated rise in natural gas demand from LNG Canada. These growth prospects, coupled with ARC Resources trading at CA$22.46, significantly below its estimated fair value of CA$66.94, suggest a compelling investment opportunity. However, investors should remain cautious of market volatility, regulatory risks, and the company's historically unstable dividend payments, which could impact long-term financial stability and investor confidence.

Turning Ideas Into Actions

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

If you're looking to trade ARC Resources, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSX:ARX

ARC Resources

Engages in the acquiring and developing crude oil, natural gas, condensate, and natural gas liquids in Canada.

Proven track record with adequate balance sheet.

Market Insights

Community Narratives