Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:CG

Discovering Canada's Undiscovered Gems in October 2024

Simply Wall St

Reviewed by Simply Wall St

The Canadian market has shown robust performance, with a 1.4% increase in the last week and a remarkable 28% rise over the past year, while earnings are projected to grow by 16% annually. In this thriving environment, identifying stocks that combine strong fundamentals with growth potential can uncover hidden opportunities for investors.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 15.28% | 7.58% | ★★★★★★ |

| Santacruz Silver Mining | 14.30% | 49.04% | 63.44% | ★★★★★★ |

| Taiga Building Products | NA | 6.05% | 10.50% | ★★★★★★ |

| Grown Rogue International | 24.92% | 43.35% | 67.95% | ★★★★★☆ |

| Mako Mining | 22.90% | 38.12% | 54.79% | ★★★★★☆ |

| Pizza Pizza Royalty | 15.66% | 3.64% | 3.95% | ★★★★☆☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

| Dundee | 5.93% | -38.65% | 39.44% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

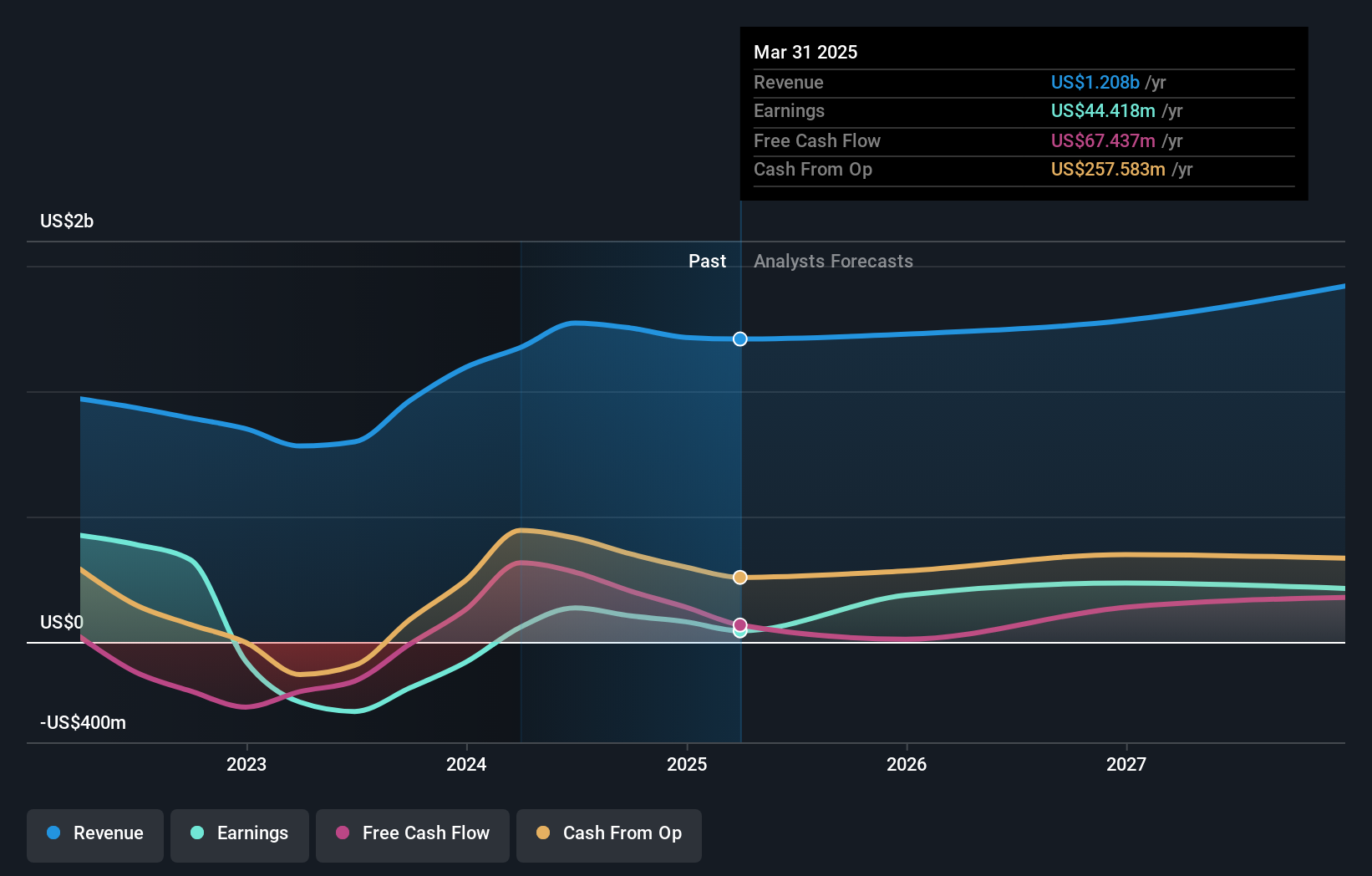

Centerra Gold (TSX:CG)

Simply Wall St Value Rating: ★★★★★★

Overview: Centerra Gold Inc. is a mining company focused on the acquisition, exploration, development, and operation of gold and copper properties across North America, Turkey, and other international locations with a market capitalization of CA$2.18 billion.

Operations: Centerra Gold generates revenue primarily from its Öksüt, Molybdenum, and Mount Milligan segments, contributing $603.31 million, $239.65 million, and $429.08 million respectively.

Centerra Gold, a notable contender in the mining sector, has recently turned profitable, showcasing high-quality earnings and trading at 55% below its fair value estimate. The company reported a net income of US$37.67 million in Q2 2024, reversing from a net loss of US$39.68 million the previous year. Moreover, Centerra is debt-free and has reduced its debt from five years ago when it had a debt-to-equity ratio of 4.2%. Recent buybacks saw them repurchase over 3.58 million shares for US$21.9 million this year, reflecting confidence in their financial health and growth prospects.

- Click here and access our complete health analysis report to understand the dynamics of Centerra Gold.

Examine Centerra Gold's past performance report to understand how it has performed in the past.

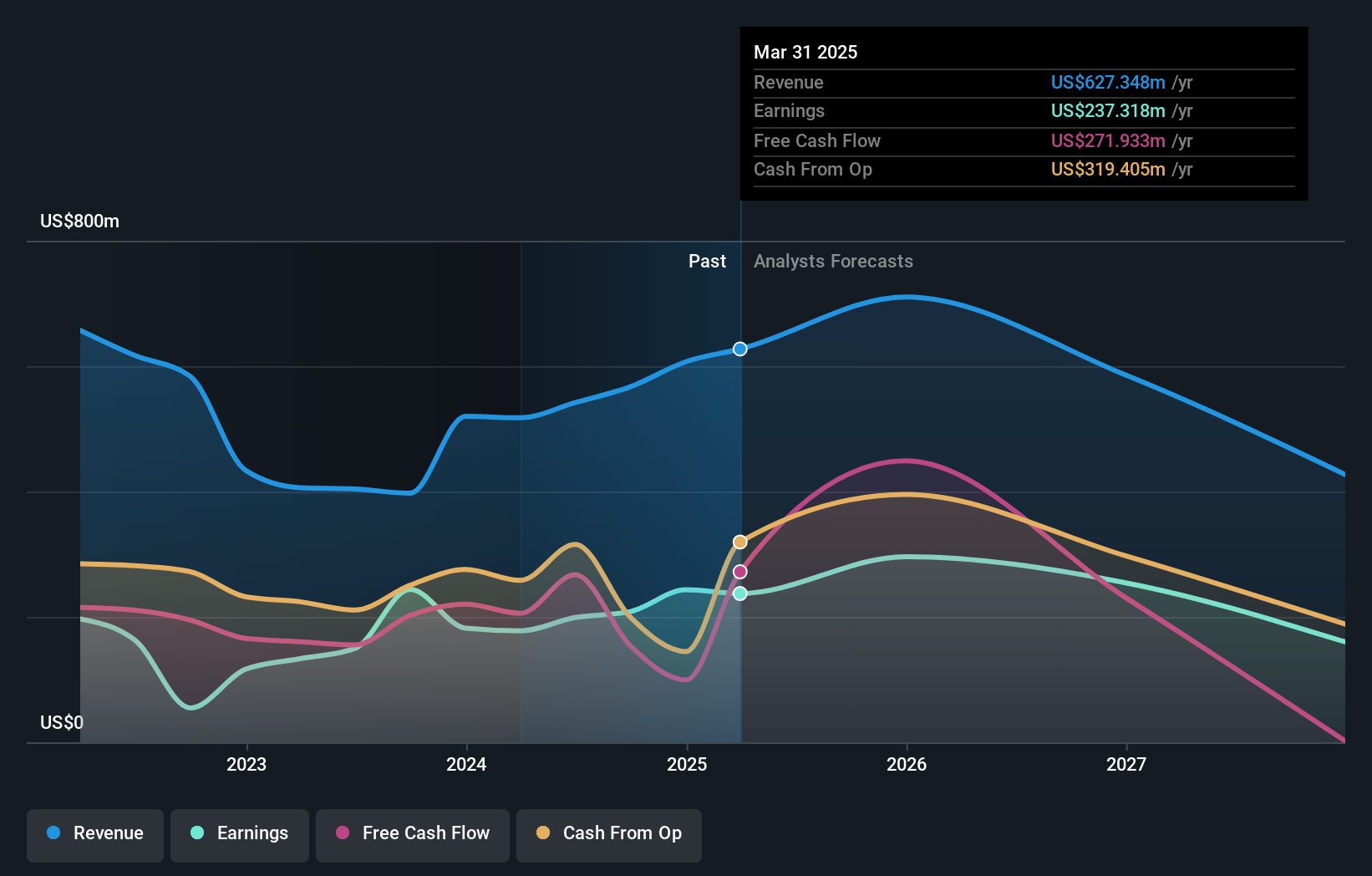

Dundee Precious Metals (TSX:DPM)

Simply Wall St Value Rating: ★★★★★★

Overview: Dundee Precious Metals Inc. is a gold mining company involved in the acquisition, exploration, development, mining, and processing of precious metals with a market cap of CA$2.60 billion.

Operations: Dundee Precious Metals generates revenue primarily from its Ada Tepe and Chelopech segments, contributing $237.16 million and $304.68 million, respectively.

Dundee Precious Metals, a nimble player in the mining sector, shines with its debt-free status and robust earnings growth of 33.1% over the past year, outpacing industry norms. It trades at a tempting 23.7% below estimated fair value, suggesting potential upside for investors eyeing undervalued opportunities. Recent buybacks totaling $26.4 million for 3.15 million shares underscore management's confidence in its trajectory. The company's strategic advancements at Coka Rakita project aim to bolster long-term prospects with promising high-grade gold finds and ongoing feasibility studies targeting completion by early 2025, setting the stage for future production milestones by 2028.

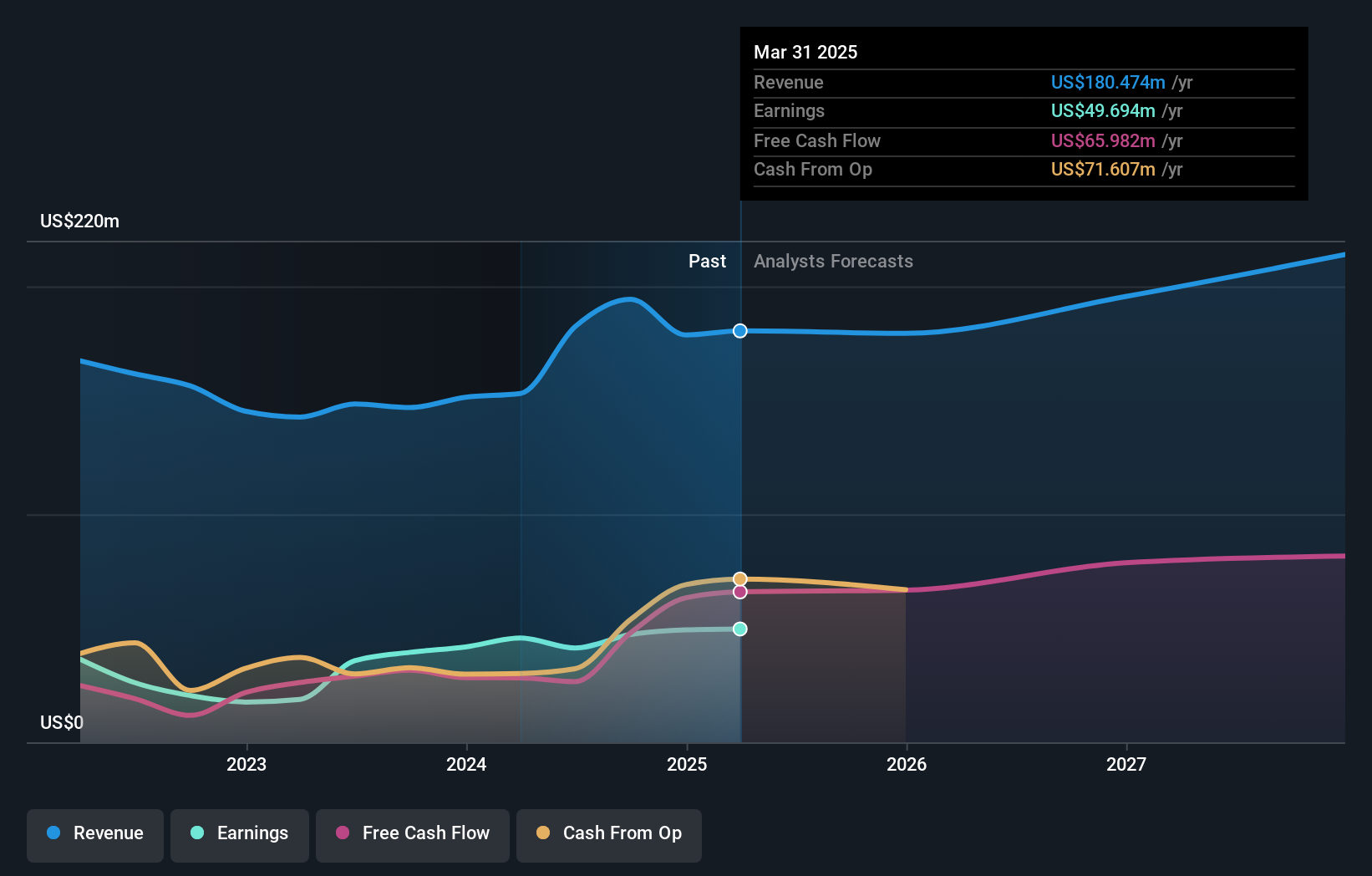

Sprott (TSX:SII)

Simply Wall St Value Rating: ★★★★★☆

Overview: Sprott Inc. is a publicly owned asset management holding company with a market capitalization of approximately CA$1.67 billion.

Operations: Sprott Inc. generates revenue primarily from exchange-listed products, contributing $120.16 million, and managed equities and private strategies, which contribute $31.76 million and $31.19 million respectively. The company's financial performance is impacted by segment adjustments amounting to -$0.75 million.

Sprott, a notable player in Canada's financial scene, has shown robust earnings growth of 15.6% over the past year, surpassing the Capital Markets industry's 13.2%. Despite this positive trend, its debt to equity ratio has risen from 6.1 to 9.2 over five years, which might raise some eyebrows among cautious investors. The company reported second-quarter revenue of US$47.99 million but saw a dip in net income to US$13.36 million from US$17.72 million last year; nevertheless, interest payments are comfortably covered by EBIT at a multiple of 19.7x, showcasing solid financial health and resilience amidst market challenges.

- Navigate through the intricacies of Sprott with our comprehensive health report here.

Gain insights into Sprott's historical performance by reviewing our past performance report.

Turning Ideas Into Actions

- Embark on your investment journey to our 52 TSX Undiscovered Gems With Strong Fundamentals selection here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CG

Centerra Gold

Engages in the acquisition, exploration, development, and operation of gold and copper properties in North America, Turkey, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor