Advertisement

- Canada

- /

- Consumer Finance

- /

- TSX:GSY

Why goeasy (TSX:GSY) Is Down 5.0% After Rising Revenue Paired With Sharply Lower Net Income

Simply Wall St

Reviewed by Sasha Jovanovic

- goeasy Ltd. reported its third quarter 2025 results, showing revenue of C$440.22 million, up from C$383.2 million a year earlier, but with net income falling to C$33.09 million from C$84.94 million in the same period last year; the company also announced a quarterly dividend of C$1.46 per share payable in January 2026.

- This mix of revenue growth alongside a sharp drop in net income and earnings per share highlights a divergence between top-line momentum and bottom-line pressures for the company.

- We'll examine how the rise in revenue but lower net income may influence goeasy's investment outlook and operational challenges.

Find companies with promising cash flow potential yet trading below their fair value.

goeasy Investment Narrative Recap

To be a shareholder in goeasy, you need to believe in the continued strong demand for non-prime credit and the company's ability to grow its loan portfolio, despite regulatory headwinds and operational challenges. The latest news, revenue growth but a sharp drop in net income, puts even more focus on how goeasy manages rising credit losses and regulatory rate pressures. While the revenue boost supports the main growth catalyst, the impact on the biggest risk, shrinking margins and profitability due to increased loan loss provisions, is material and warrants close attention.

Of the recent announcements, the most relevant is the third quarter earnings release, which showed revenue up to C$440.22 million but net income falling to C$33.09 million. This result directly informs both the company’s biggest growth catalyst, expanding the non-prime lending market, and the challenge it faces from higher credit losses and stricter rate caps, which could further impact future earnings and operational flexibility.

However, investors should be aware that despite revenue growth, the rising costs related to credit losses could…

Read the full narrative on goeasy (it's free!)

goeasy's outlook anticipates CA$2.7 billion in revenue and CA$476.3 million in earnings by 2028. This is based on an annual revenue growth rate of 48.7% and an earnings increase of CA$191.6 million from the current CA$284.7 million.

Uncover how goeasy's forecasts yield a CA$223.30 fair value, a 82% upside to its current price.

Exploring Other Perspectives

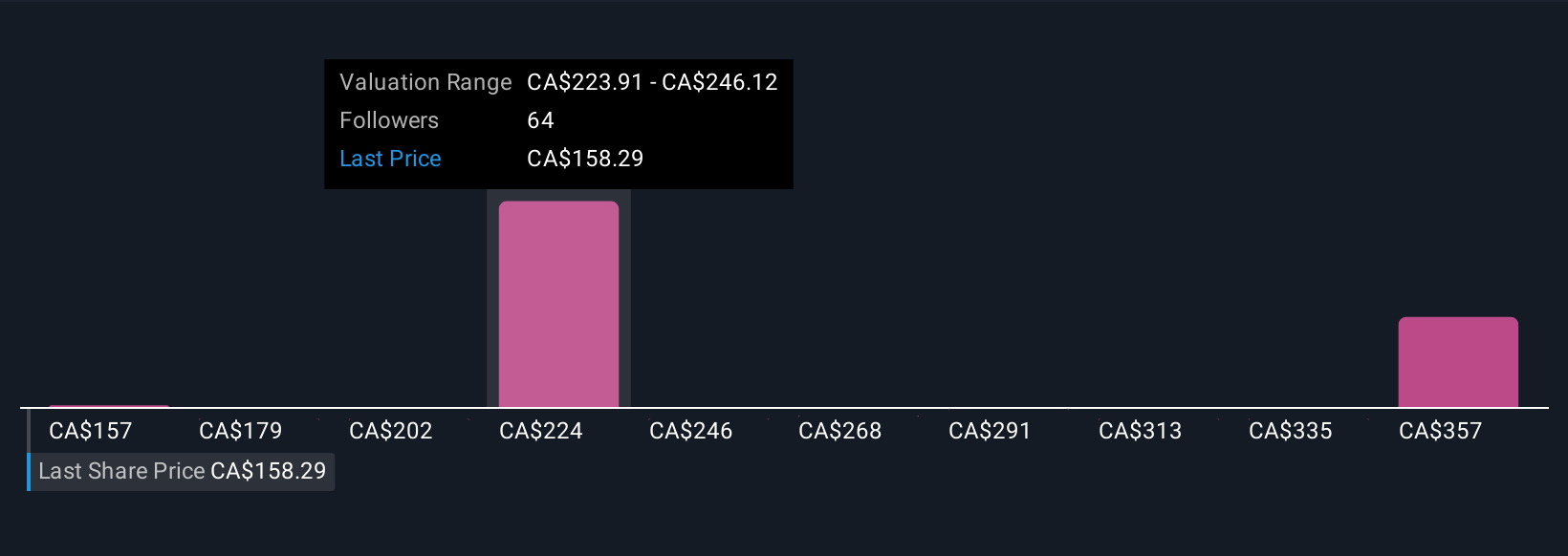

Simply Wall St Community members produced 12 fair value estimates for goeasy, spanning from C$157 to C$388 per share. Persistent margin pressure from credit losses remains a critical factor that could sway future valuations, so consider how opinions differ widely before forming your own view.

Explore 12 other fair value estimates on goeasy - why the stock might be worth just CA$157.27!

Build Your Own goeasy Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your goeasy research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free goeasy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate goeasy's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- AI is about to change healthcare. These 31 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:GSY

goeasy

Provides non-prime leasing and lending services under the easyhome, easyfinancial, and LendCare brands to consumers in Canada.

Exceptional growth potential, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor