- Canada

- /

- Hospitality

- /

- TSX:QSP.UN

Investing in Restaurant Brands International Limited Partnership (TSE:QSP.UN) three years ago would have delivered you a 22% gain

Thanks in no small measure to Vanguard founder Jack Bogle, it's easy buy a low cost index fund, which should provide the average market return. But you can make better returns by buying undervalued shares. Notably, the Restaurant Brands International Limited Partnership (TSE:QSP.UN) share price has gained 10% in three years, which is better than the average market return. In contrast, the stock is actually down 0.6% in the last year, suggesting a lack of positive momentum.

With that in mind, it's worth seeing if the company's underlying fundamentals have been the driver of long term performance, or if there are some discrepancies.

Check out our latest analysis for Restaurant Brands International Limited Partnership

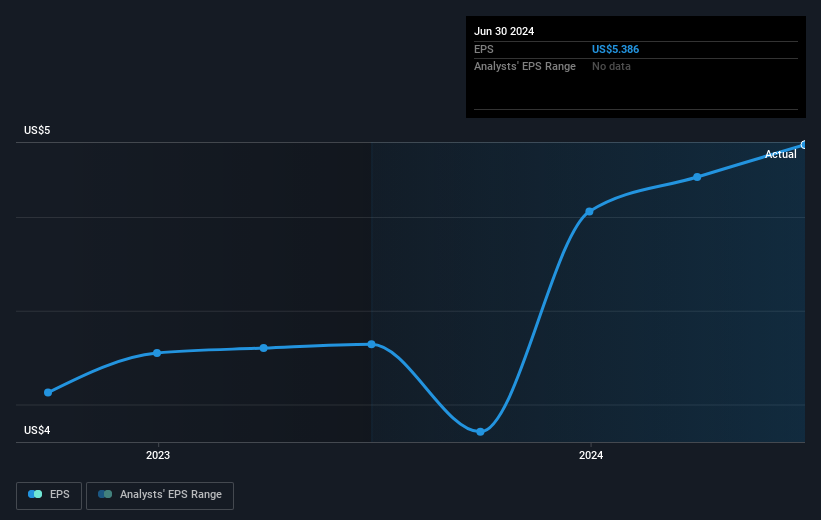

There is no denying that markets are sometimes efficient, but prices do not always reflect underlying business performance. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

Restaurant Brands International Limited Partnership was able to grow its EPS at 24% per year over three years, sending the share price higher. This EPS growth is higher than the 3% average annual increase in the share price. So it seems investors have become more cautious about the company, over time.

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

Before buying or selling a stock, we always recommend a close examination of historic growth trends, available here.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). The TSR incorporates the value of any spin-offs or discounted capital raisings, along with any dividends, based on the assumption that the dividends are reinvested. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. We note that for Restaurant Brands International Limited Partnership the TSR over the last 3 years was 22%, which is better than the share price return mentioned above. This is largely a result of its dividend payments!

A Different Perspective

Restaurant Brands International Limited Partnership provided a TSR of 2.6% over the last twelve months. But that return falls short of the market. On the bright side, that's still a gain, and it's actually better than the average return of 2% over half a decade This could indicate that the company is winning over new investors, as it pursues its strategy. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Even so, be aware that Restaurant Brands International Limited Partnership is showing 2 warning signs in our investment analysis , you should know about...

For those who like to find winning investments this free list of undervalued companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Canadian exchanges.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:QSP.UN

Restaurant Brands International Limited Partnership

Operates and franchises quick service restaurants in the United States and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Community Narratives