Advertisement

- Canada

- /

- Food and Staples Retail

- /

- TSX:EMP.A

Why You Might Be Interested In Empire Company Limited (TSE:EMP.A) For Its Upcoming Dividend

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that Empire Company Limited (TSE:EMP.A) is about to go ex-dividend in just 2 days. If you purchase the stock on or after the 12th of July, you won't be eligible to receive this dividend, when it is paid on the 31st of July.

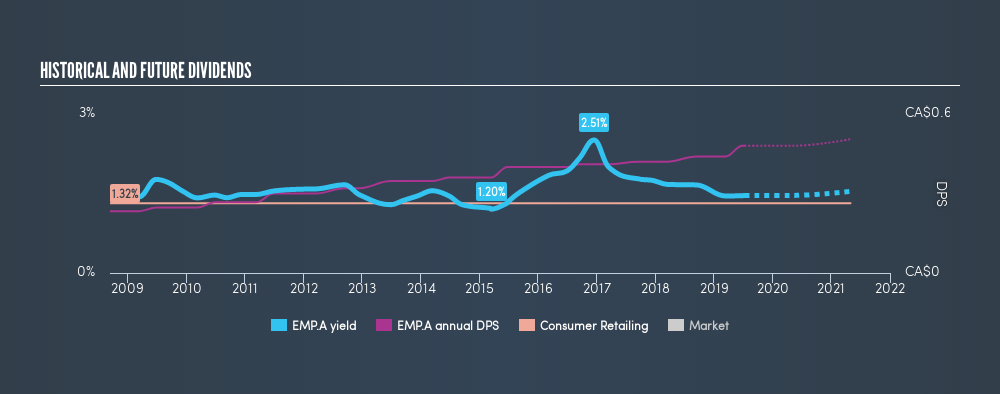

Empire's next dividend payment will be CA$0.12 per share, on the back of last year when the company paid a total of CA$0.44 to shareholders. Last year's total dividend payments show that Empire has a trailing yield of 1.5% on the current share price of CA$32.79. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether Empire can afford its dividend, and if the dividend could grow.

See our latest analysis for Empire

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Empire paid out a comfortable 31% of its profit last year. A useful secondary check can be to evaluate whether Empire generated enough free cash flow to afford its dividend. It distributed 26% of its free cash flow as dividends, a comfortable payout level for most companies.

It's positive to see that Empire's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings decline and the company is forced to cut its dividend, investors could watch the value of their investment go up in smoke. Fortunately for readers, Empire's earnings per share have been growing at 18% a year for the past five years.

Earnings per share have been growing rapidly and the company is retaining a majority of its earnings within the business. This will make it easier to fund future growth efforts and we think this is an attractive combination - plus the dividend can always be increased later.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. Since the start of our data, 10 years ago, Empire has lifted its dividend by approximately 7.5% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

Final Takeaway

Is Empire an attractive dividend stock, or better left on the shelf? We love that Empire is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. These characteristics suggest the company is reinvesting in growing its business, while the conservative payout ratio also implies a reduced risk of the dividend being cut in the future. Empire looks solid on this analysis overall, and we'd definitely consider investigating it more closely.

Wondering what the future holds for Empire? See what the seven analysts we track are forecasting, with this visualisation of its historical and future estimated earnings and cash flow

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:EMP.A

Empire

Engages in the food retail and related real estate businesses in Canada.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor