The harsh reality for GreenPower Motor Company Inc. (CVE:GPV) shareholders is that its auditors, BDO LLP, expressed doubts about its ability to continue as a going concern, in its reported results to March 2023. Thus we can say that, based on the results to that date, the company should raise capital or otherwise raise cash, without much delay.

If the company does have to issue more shares, potential investors will be sure to consider how desperate it is for capital. So current risks on the balance sheet could have a big impact on how shareholders fare from here. The biggest concern we would have is the company's debt, since its lenders might force the company into administration if it cannot repay them.

Check out our latest analysis for GreenPower Motor

What Is GreenPower Motor's Debt?

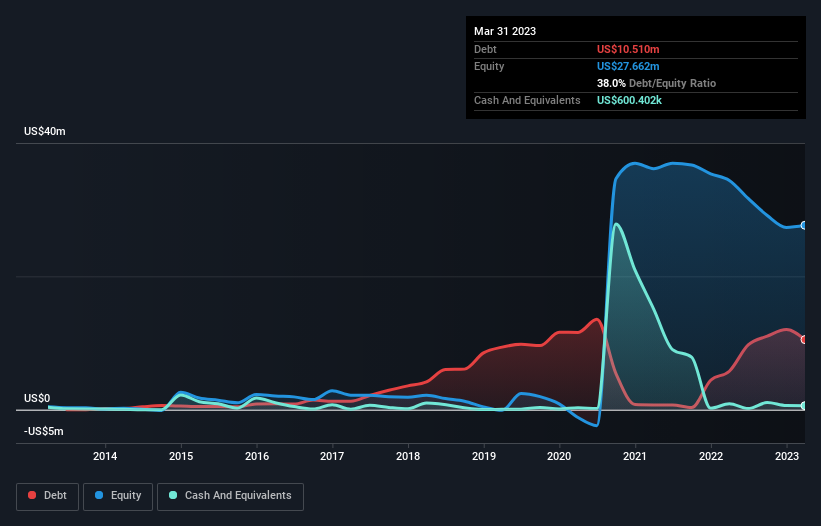

You can click the graphic below for the historical numbers, but it shows that as of March 2023 GreenPower Motor had US$10.5m of debt, an increase on US$5.77m, over one year. On the flip side, it has US$600.4k in cash leading to net debt of about US$9.91m.

A Look At GreenPower Motor's Liabilities

We can see from the most recent balance sheet that GreenPower Motor had liabilities of US$26.5m falling due within a year, and liabilities of US$9.36m due beyond that. Offsetting this, it had US$600.4k in cash and US$11.6m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$23.6m.

GreenPower Motor has a market capitalization of US$111.2m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine GreenPower Motor's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year GreenPower Motor wasn't profitable at an EBIT level, but managed to grow its revenue by 130%, to US$40m. So its pretty obvious shareholders are hoping for more growth!

Caveat Emptor

Despite the top line growth, GreenPower Motor still had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping US$13m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through US$15m of cash over the last year. So suffice it to say we consider the stock very risky. We're too cautious to want to invest in a company after an auditor has expressed doubts about its ability to continue as a going concern. That's because we find it more comfortable to invest in companies that always keep the balance sheet reasonably strong. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. To that end, you should learn about the 3 warning signs we've spotted with GreenPower Motor (including 2 which are a bit concerning) .

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:GPV

GreenPower Motor

Designs, manufactures, and distributes electric vehicles for commercial markets in the United States and Canada.

Excellent balance sheet slight.