- Canada

- /

- Trade Distributors

- /

- TSX:TIH

Toromont Industries (TSE:TIH) Is Paying Out A Larger Dividend Than Last Year

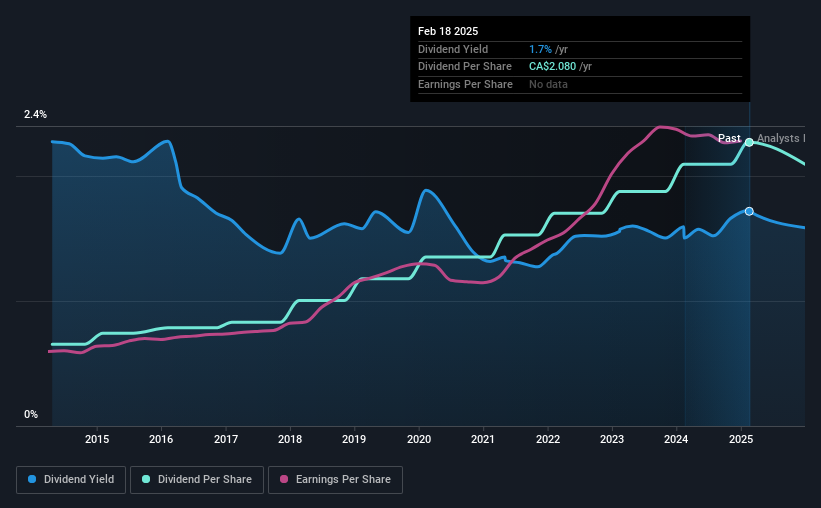

The board of Toromont Industries Ltd. (TSE:TIH) has announced that it will be paying its dividend of CA$0.52 on the 4th of April, an increased payment from last year's comparable dividend. Although the dividend is now higher, the yield is only 1.7%, which is below the industry average.

See our latest analysis for Toromont Industries

Toromont Industries' Future Dividend Projections Appear Well Covered By Earnings

If it is predictable over a long period, even low dividend yields can be attractive. However, based ont he last payment, Toromont Industries was earning enough to cover the dividend pretty comfortably. However, with more than 75% of free cash flow being paid out to shareholders, future growth could potentially be constrained.

Over the next year, EPS is forecast to expand by 6.8%. If the dividend continues along recent trends, we estimate the payout ratio will be 33%, which is in the range that makes us comfortable with the sustainability of the dividend.

Toromont Industries Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. The dividend has gone from an annual total of CA$0.60 in 2015 to the most recent total annual payment of CA$2.08. This means that it has been growing its distributions at 13% per annum over that time. We can see that payments have shown some very nice upward momentum without faltering, which provides some reassurance that future payments will also be reliable.

The Dividend Looks Likely To Grow

Some investors will be chomping at the bit to buy some of the company's stock based on its dividend history. Toromont Industries has impressed us by growing EPS at 12% per year over the past five years. Toromont Industries definitely has the potential to grow its dividend in the future with earnings on an uptrend and a low payout ratio.

In Summary

In summary, it's great to see that the company can raise the dividend and keep it in a sustainable range. The payments look okay by most measures, the lack of cash flow could definitely cause problems for them in the future. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Meanwhile, despite the importance of dividend payments, they are not the only factors our readers should know when assessing a company. Earnings growth generally bodes well for the future value of company dividend payments. See if the 9 Toromont Industries analysts we track are forecasting continued growth with our free report on analyst estimates for the company. Is Toromont Industries not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Toromont Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:TIH

Toromont Industries

Provides specialized capital equipment in Canada, the United States, and internationally.

Flawless balance sheet average dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)