Downgrade: Here's How Analysts See The Lion Electric Company (TSE:LEV) Performing In The Near Term

The analysts covering The Lion Electric Company (TSE:LEV) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. Both revenue and earnings per share (EPS) estimates were cut sharply as the analysts factored in the latest outlook for the business, concluding that they were too optimistic previously.

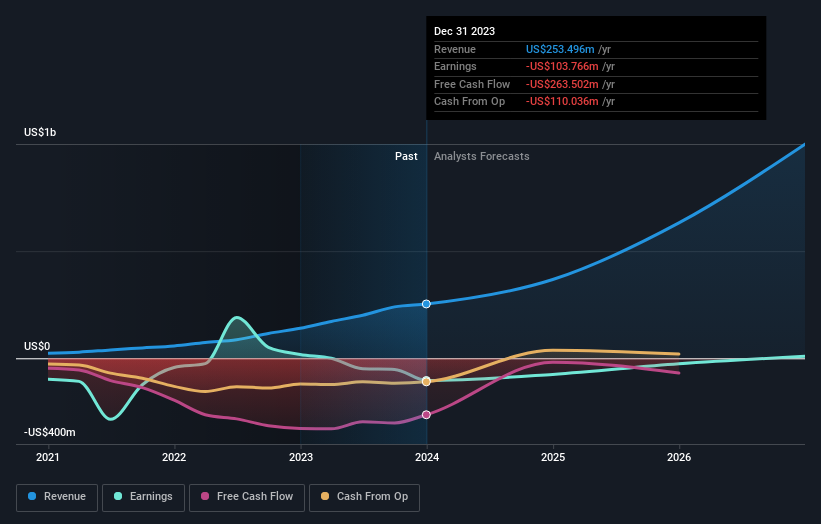

After this downgrade, Lion Electric's eight analysts are now forecasting revenues of US$368m in 2024. This would be a sizeable 45% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 29% to US$0.32 per share. Yet prior to the latest estimates, the analysts had been forecasting revenues of US$532m and losses of US$0.28 per share in 2024. Ergo, there's been a clear change in sentiment, with the analysts administering a notable cut to this year's revenue estimates, while at the same time increasing their loss per share forecasts.

Check out our latest analysis for Lion Electric

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. The period to the end of 2024 brings more of the same, according to the analysts, with revenue forecast to display 45% growth on an annualised basis. That is in line with its 53% annual growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 8.3% per year. So although Lion Electric is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The most important thing to take away is that analysts increased their loss per share estimates for this year. While analysts did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. Given the serious cut to this year's outlook, it's clear that analysts have turned more bearish on Lion Electric, and we wouldn't blame shareholders for feeling a little more cautious themselves.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Lion Electric analysts - going out to 2026, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:LEV

Lion Electric

Designs, develops, manufactures, and distributes purpose-built all-electric medium and heavy-duty urban vehicles in North America.

Slight with mediocre balance sheet.