- Canada

- /

- Trade Distributors

- /

- TSX:E

Earnings Troubles May Signal Larger Issues for Enterprise Group (TSE:E) Shareholders

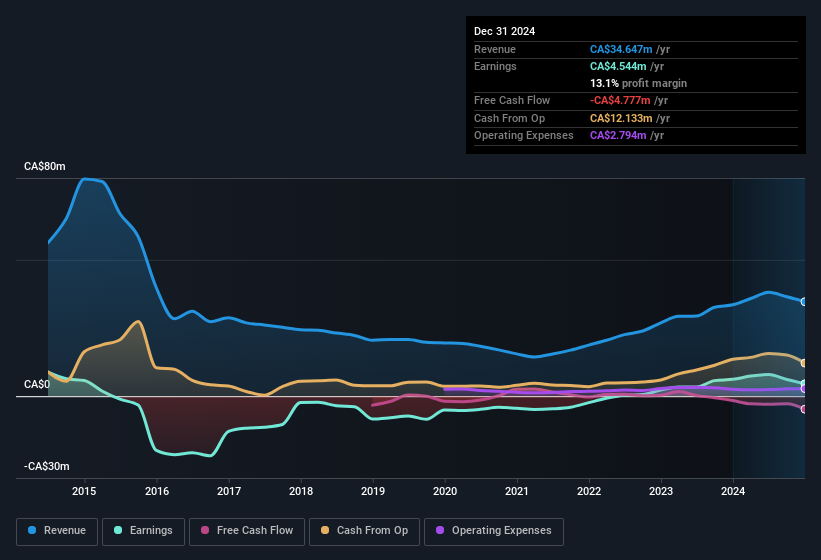

The market wasn't impressed with the soft earnings from Enterprise Group, Inc. (TSE:E) recently. We did some analysis, and found that there are some reasons to be cautious about the headline numbers.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. Enterprise Group expanded the number of shares on issue by 34% over the last year. Therefore, each share now receives a smaller portion of profit. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out Enterprise Group's historical EPS growth by clicking on this link.

How Is Dilution Impacting Enterprise Group's Earnings Per Share (EPS)?

Enterprise Group was losing money three years ago. And even focusing only on the last twelve months, we see profit is down 26%. Like a sack of potatoes thrown from a delivery truck, EPS fell harder, down 40% in the same period. And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

In the long term, if Enterprise Group's earnings per share can increase, then the share price should too. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Enterprise Group's Profit Performance

Over the last year Enterprise Group issued new shares and so, there's a noteworthy divergence between EPS and net income growth. As a result, we think it may well be the case that Enterprise Group's underlying earnings power is lower than its statutory profit. Sadly, its EPS was down over the last twelve months. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. For example, we've found that Enterprise Group has 2 warning signs (1 shouldn't be ignored!) that deserve your attention before going any further with your analysis.

Today we've zoomed in on a single data point to better understand the nature of Enterprise Group's profit. But there are plenty of other ways to inform your opinion of a company. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Enterprise Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:E

Enterprise Group

Through its subsidiaries, operates as an equipment rental and construction services company in Canada.

High growth potential with adequate balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)