Advertisement

Enghouse Systems And 2 Additional Premier TSX Dividend Stocks

Simply Wall St

Reviewed by Simply Wall St

As the Canadian economy experiences a cooling labor market and anticipates further rate cuts from the Bank of Canada, investors are presented with a potentially favorable environment for financial markets. In this context, dividend stocks can offer stability and income, making them an attractive option; Enghouse Systems and two other premier TSX dividend stocks exemplify how quality investments can thrive even amidst economic shifts.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 6.87% | ★★★★★★ |

| Acadian Timber (TSX:ADN) | 6.58% | ★★★★★★ |

| Olympia Financial Group (TSX:OLY) | 7.27% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 4.84% | ★★★★★☆ |

| Enghouse Systems (TSX:ENGH) | 3.40% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.35% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 3.84% | ★★★★★☆ |

| National Bank of Canada (TSX:NA) | 3.31% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.29% | ★★★★★☆ |

| Sun Life Financial (TSX:SLF) | 4.07% | ★★★★★☆ |

Click here to see the full list of 27 stocks from our Top TSX Dividend Stocks screener.

Here's a peek at a few of the choices from the screener.

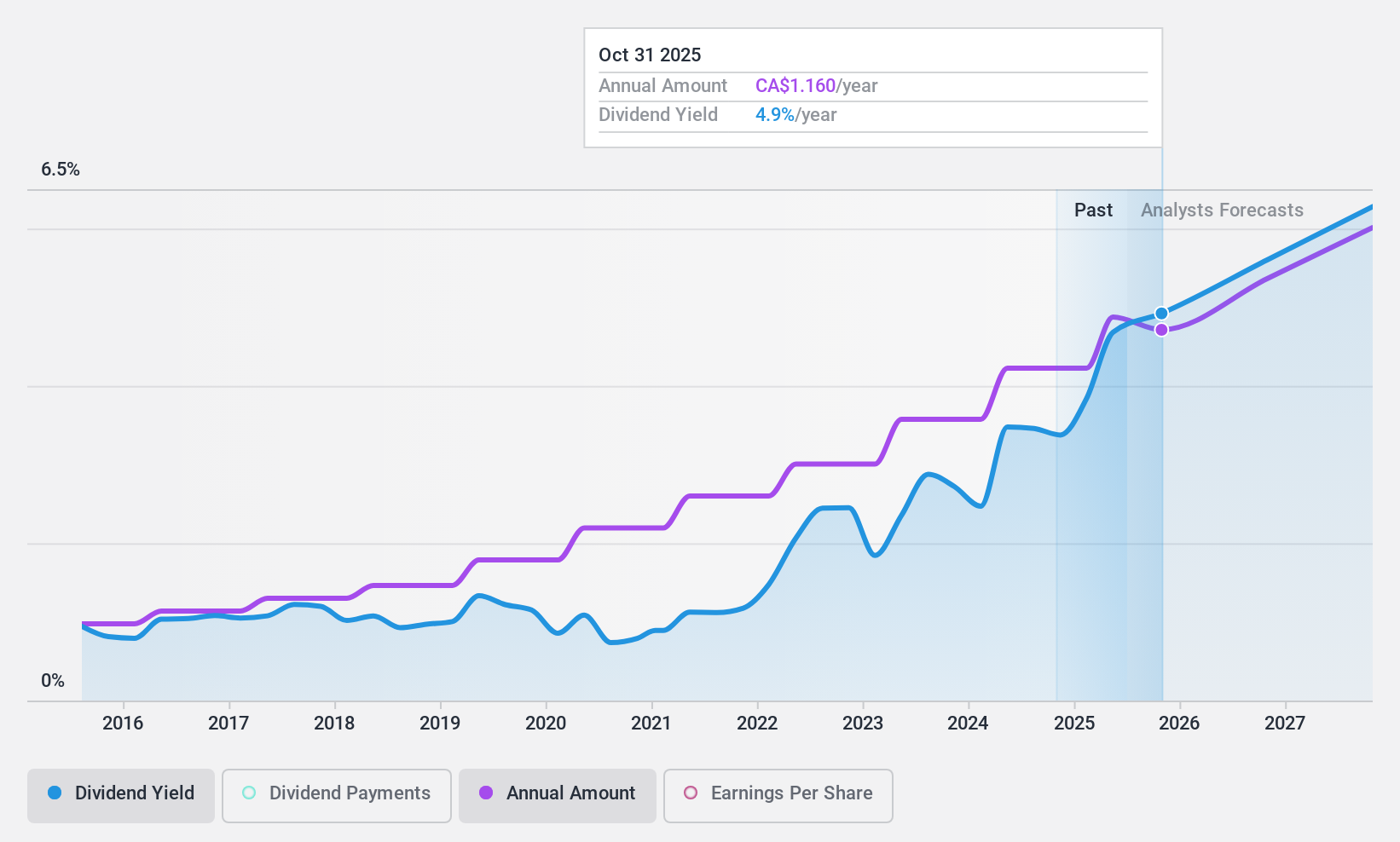

Enghouse Systems (TSX:ENGH)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Enghouse Systems Limited, along with its subsidiaries, develops enterprise software solutions globally and has a market cap of CA$1.68 billion.

Operations: Enghouse Systems Limited generates revenue through its Asset Management Group, contributing CA$187.17 million, and its Interactive Management Group, which brings in CA$312.77 million.

Dividend Yield: 3.4%

Enghouse Systems offers a stable dividend yield of 3.4%, supported by a sustainable payout ratio of 66% from earnings and 45.4% from cash flows. The company's dividends have been reliable and growing over the past decade, though they are lower than the top Canadian dividend payers. Recent financial results show increased revenue and net income, supporting continued dividend payments, while recent executive changes might impact future strategy.

- Click to explore a detailed breakdown of our findings in Enghouse Systems' dividend report.

- Insights from our recent valuation report point to the potential undervaluation of Enghouse Systems shares in the market.

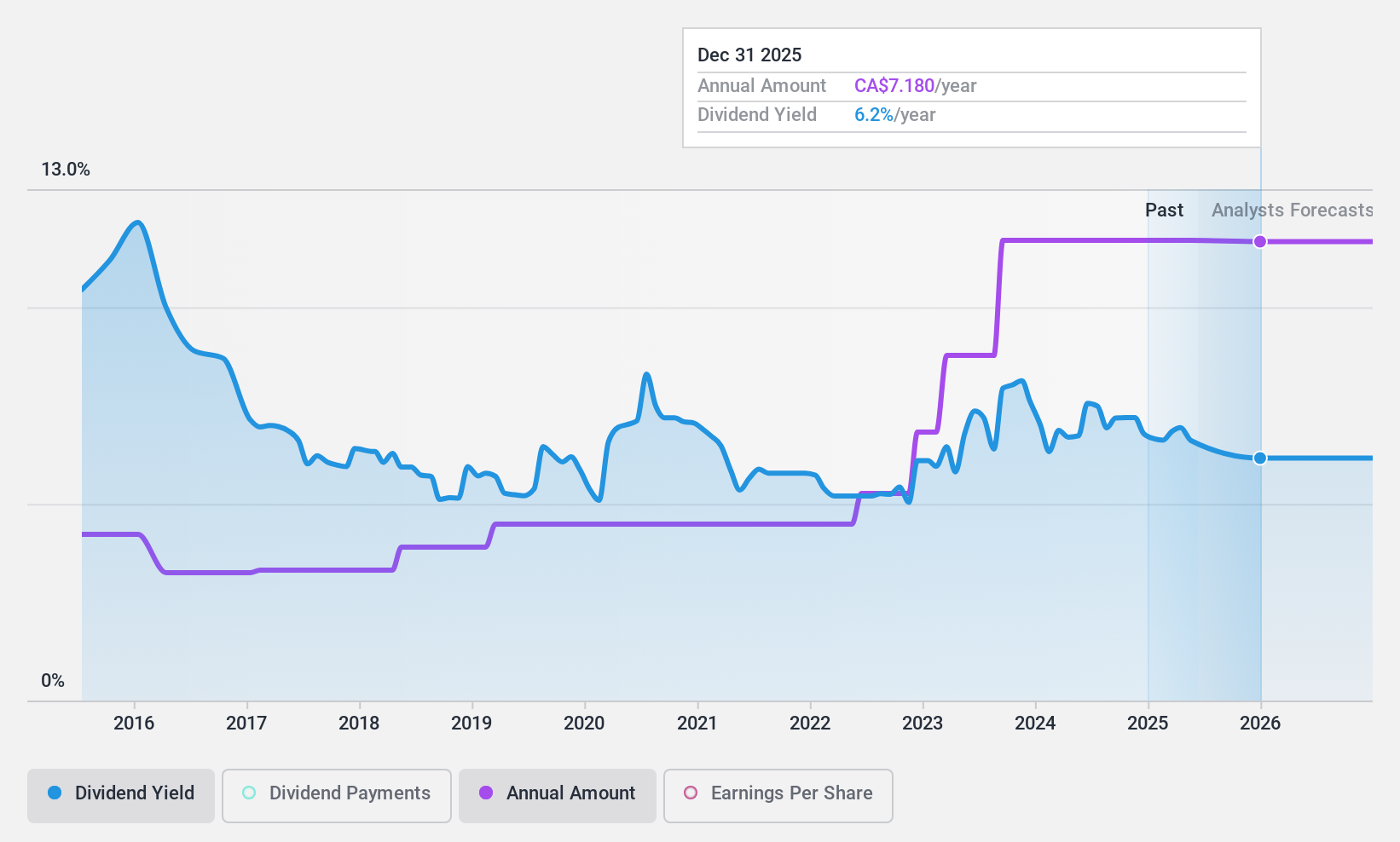

Olympia Financial Group (TSX:OLY)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Olympia Financial Group Inc., with a market cap of CA$235.82 million, operates in Canada as a non-deposit taking trust company through its subsidiary, Olympia Trust Company.

Operations: Olympia Financial Group Inc.'s revenue segments include Investment Account Services (CA$79.02 million), Health (CA$10.21 million), Currency and Global Payments (CA$8.43 million), Corporate and Shareholder Services (CA$3.98 million), Exempt Edge (CA$1.41 million), and Corporate (CA$0.13 million).

Dividend Yield: 7.3%

Olympia Financial Group's dividend yield of 7.27% ranks among the top Canadian dividend payers, supported by a payout ratio of 68.1% from earnings and 72.7% from cash flows. Despite this, its dividends have been volatile over the past decade, reflecting an unstable track record. Recent financials show modest revenue growth but a slight decline in net income for Q2 2024 compared to last year, which could impact future dividend sustainability amid forecasted earnings declines.

- Navigate through the intricacies of Olympia Financial Group with our comprehensive dividend report here.

- Our valuation report unveils the possibility Olympia Financial Group's shares may be trading at a discount.

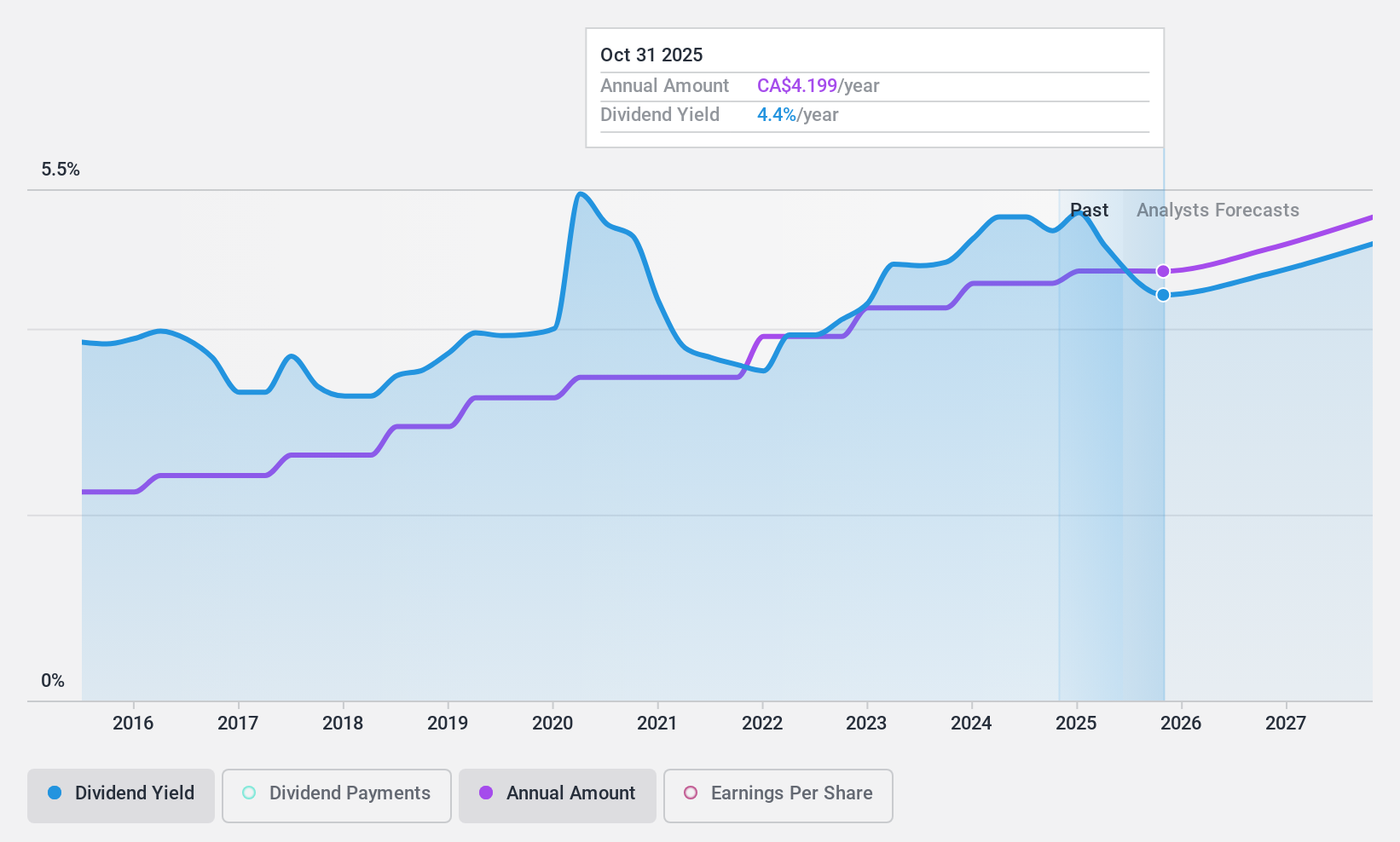

Toronto-Dominion Bank (TSX:TD)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: The Toronto-Dominion Bank, along with its subsidiaries, offers a range of financial products and services across Canada, the United States, and internationally, with a market cap of approximately CA$137.19 billion.

Operations: Toronto-Dominion Bank generates its revenue from several key segments, including Canadian Personal and Commercial Banking (CA$17.77 billion), U.S. Retail (CA$12.75 billion), Wealth Management and Insurance (CA$12.20 billion), Wholesale Banking (CA$6.76 billion), and Corporate activities (CA$1.19 billion).

Dividend Yield: 5.2%

Toronto-Dominion Bank's dividend has been reliable and growing over the past decade, but its high payout ratio of 92.7% raises concerns about sustainability. The bank's recent legal issues, including a $3.09 billion penalty related to AML compliance, have impacted its financials, resulting in a net loss for Q3 2024. Although trading below estimated fair value and with earnings forecasted to grow annually by 17.19%, these factors may affect future dividend coverage and stability.

- Click here to discover the nuances of Toronto-Dominion Bank with our detailed analytical dividend report.

- Our valuation report unveils the possibility Toronto-Dominion Bank's shares may be trading at a premium.

Seize The Opportunity

- Click here to access our complete index of 27 Top TSX Dividend Stocks.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enghouse Systems might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:ENGH

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor