Bank of Nova Scotia (TSX:BNS) Confirms $1.10 Dividend Amid Strong Q3 Earnings Rise

Reviewed by Simply Wall St

Bank of Nova Scotia (TSX:BNS) recently affirmed a dividend of CAD 1.10, and its Q3 earnings report showed strong growth compared to last year, with net income and net interest income both significantly up. While these factors could have positively influenced its share price, broader market conditions, such as President Trump's decision to remove a Federal Reserve official and speculation on interest rate cuts, also underpin investor sentiment. Despite market turbulence, the company's steady dividend and solid quarterly earnings suggest a reinforcing effect on its recent 9% stock price increase over the last quarter.

The recent affirmation of Bank of Nova Scotia's CA$1.10 dividend, alongside robust Q3 earnings, reinforces confidence in its initiatives like Mortgage+ and Scene+ which aim to enhance revenue and earnings stability. Despite short-term market volatility spurred by broader economic factors, such measures may support the bank's future revenue streams and bolster its earnings forecasts. The strategic emphasis on core deposits and higher-growth markets is crucial as it may mitigate risks from elevated credit loss provisions and geopolitical factors.

Over the past five years, Bank of Nova Scotia has delivered an impressive total return of 88.01%, highlighting its resilience and potential as a long-term investment. However, over the past year, the stock has not kept pace with the Canadian Banks industry, which returned 25.8%. This discrepancy indicates potential areas for growth and improvement, further underpinned by their new initiatives.

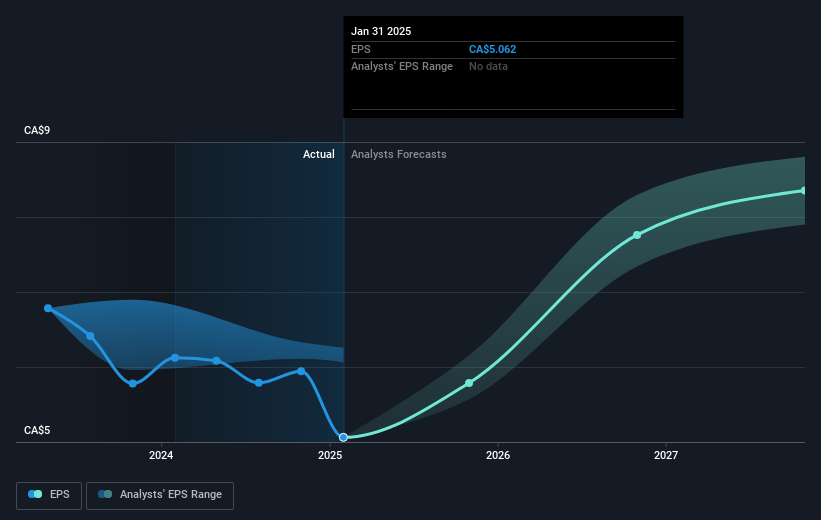

Currently trading at CA$79.53, the share price is slightly below the consensus analyst price target of CA$81.71, indicating limited upside potential according to market expectations. Nevertheless, the steady revenue and earnings growth assumptions, combined with solid dividend returns, suggest that Bank of Nova Scotia remains a company of interest, particularly with forecasts of revenue reaching CA$39.5 billion and earnings at CA$9.8 billion by 2028.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bank of Nova Scotia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:BNS

Bank of Nova Scotia

Provides various banking products and services in Canada, the United States, Mexico, Peru, Chile, Colombia, the Caribbean and Central America, and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Community Narratives