Advertisement

- Brazil

- /

- Electric Utilities

- /

- BOVESPA:CSRN3

Here's Why Companhia Energética do Rio Grande do Norte - COSERN (BVMF:CSRN3) Can Manage Its Debt Responsibly

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Companhia Energética do Rio Grande do Norte - COSERN (BVMF:CSRN3) makes use of debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Companhia Energética do Rio Grande do Norte - COSERN

What Is Companhia Energética do Rio Grande do Norte - COSERN's Debt?

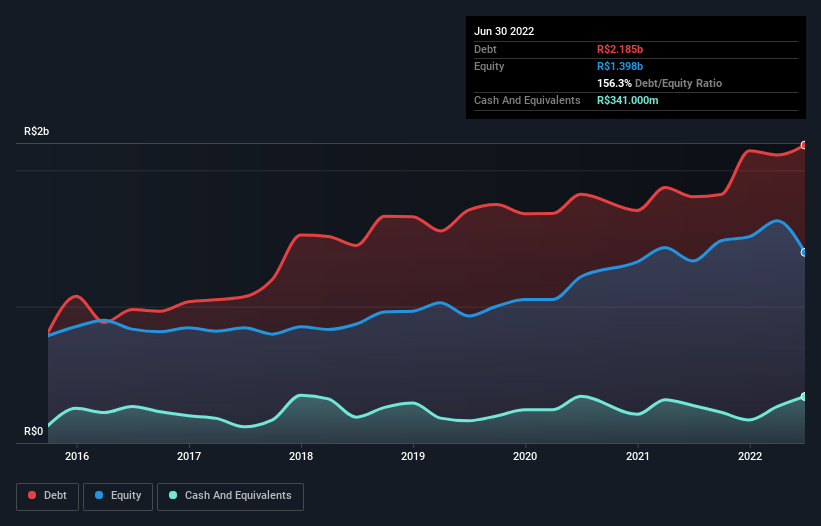

As you can see below, at the end of June 2022, Companhia Energética do Rio Grande do Norte - COSERN had R$2.19b of debt, up from R$1.81b a year ago. Click the image for more detail. On the flip side, it has R$341.0m in cash leading to net debt of about R$1.84b.

A Look At Companhia Energética do Rio Grande do Norte - COSERN's Liabilities

The latest balance sheet data shows that Companhia Energética do Rio Grande do Norte - COSERN had liabilities of R$1.83b due within a year, and liabilities of R$2.23b falling due after that. On the other hand, it had cash of R$341.0m and R$818.0m worth of receivables due within a year. So it has liabilities totalling R$2.90b more than its cash and near-term receivables, combined.

This is a mountain of leverage relative to its market capitalization of R$3.68b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Companhia Energética do Rio Grande do Norte - COSERN's net debt is sitting at a very reasonable 1.9 times its EBITDA, while its EBIT covered its interest expense just 5.6 times last year. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. It is well worth noting that Companhia Energética do Rio Grande do Norte - COSERN's EBIT shot up like bamboo after rain, gaining 48% in the last twelve months. That'll make it easier to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Companhia Energética do Rio Grande do Norte - COSERN will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Companhia Energética do Rio Grande do Norte - COSERN recorded free cash flow of 22% of its EBIT, which is weaker than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

When it comes to the balance sheet, the standout positive for Companhia Energética do Rio Grande do Norte - COSERN was the fact that it seems able to grow its EBIT confidently. But the other factors we noted above weren't so encouraging. For example, its level of total liabilities makes us a little nervous about its debt. We would also note that Electric Utilities industry companies like Companhia Energética do Rio Grande do Norte - COSERN commonly do use debt without problems. Looking at all this data makes us feel a little cautious about Companhia Energética do Rio Grande do Norte - COSERN's debt levels. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 3 warning signs for Companhia Energética do Rio Grande do Norte - COSERN you should be aware of, and 1 of them is concerning.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:CSRN3

Companhia Energética do Rio Grande do Norte - COSERN

Engages in the distribution, transmission, and transmission of electricity in Brazil.

Established dividend payer with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|18.9% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|22.2% undervalued

CH

Community Contributor