Advertisement

- Brazil

- /

- Electric Utilities

- /

- BOVESPA:CEEB3

Companhia de Eletricidade do Estado da Bahia - COELBA (BVMF:CEEB3) Takes On Some Risk With Its Use Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Companhia de Eletricidade do Estado da Bahia - COELBA (BVMF:CEEB3) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

View our latest analysis for Companhia de Eletricidade do Estado da Bahia - COELBA

What Is Companhia de Eletricidade do Estado da Bahia - COELBA's Net Debt?

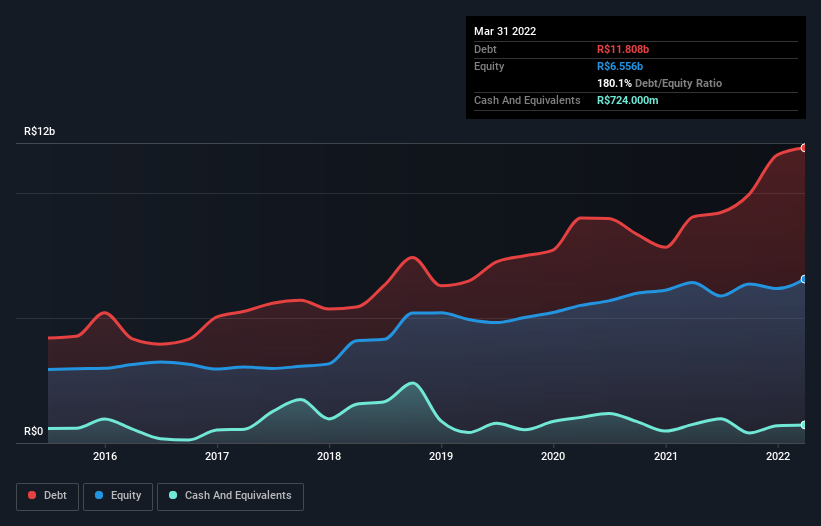

As you can see below, at the end of March 2022, Companhia de Eletricidade do Estado da Bahia - COELBA had R$11.8b of debt, up from R$9.05b a year ago. Click the image for more detail. However, because it has a cash reserve of R$724.0m, its net debt is less, at about R$11.1b.

How Healthy Is Companhia de Eletricidade do Estado da Bahia - COELBA's Balance Sheet?

The latest balance sheet data shows that Companhia de Eletricidade do Estado da Bahia - COELBA had liabilities of R$4.70b due within a year, and liabilities of R$13.8b falling due after that. Offsetting this, it had R$724.0m in cash and R$4.12b in receivables that were due within 12 months. So its liabilities total R$13.7b more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of R$9.18b, we think shareholders really should watch Companhia de Eletricidade do Estado da Bahia - COELBA's debt levels, like a parent watching their child ride a bike for the first time. In the scenario where the company had to clean up its balance sheet quickly, it seems likely shareholders would suffer extensive dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

Companhia de Eletricidade do Estado da Bahia - COELBA has a debt to EBITDA ratio of 2.8 and its EBIT covered its interest expense 5.8 times. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. It is well worth noting that Companhia de Eletricidade do Estado da Bahia - COELBA's EBIT shot up like bamboo after rain, gaining 68% in the last twelve months. That'll make it easier to manage its debt. There's no doubt that we learn most about debt from the balance sheet. But it is Companhia de Eletricidade do Estado da Bahia - COELBA's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. During the last three years, Companhia de Eletricidade do Estado da Bahia - COELBA burned a lot of cash. While investors are no doubt expecting a reversal of that situation in due course, it clearly does mean its use of debt is more risky.

Our View

On the face of it, Companhia de Eletricidade do Estado da Bahia - COELBA's level of total liabilities left us tentative about the stock, and its conversion of EBIT to free cash flow was no more enticing than the one empty restaurant on the busiest night of the year. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. We should also note that Electric Utilities industry companies like Companhia de Eletricidade do Estado da Bahia - COELBA commonly do use debt without problems. Overall, we think it's fair to say that Companhia de Eletricidade do Estado da Bahia - COELBA has enough debt that there are some real risks around the balance sheet. If all goes well, that should boost returns, but on the flip side, the risk of permanent capital loss is elevated by the debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. These risks can be hard to spot. Every company has them, and we've spotted 3 warning signs for Companhia de Eletricidade do Estado da Bahia - COELBA (of which 2 shouldn't be ignored!) you should know about.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:CEEB3

Companhia de Eletricidade do Estado da Bahia - COELBA

Engages in the distribution of electricity.

Slightly overvalued with questionable track record.

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor