Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that T4F Entretenimento S.A. (BVMF:SHOW3) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for T4F Entretenimento

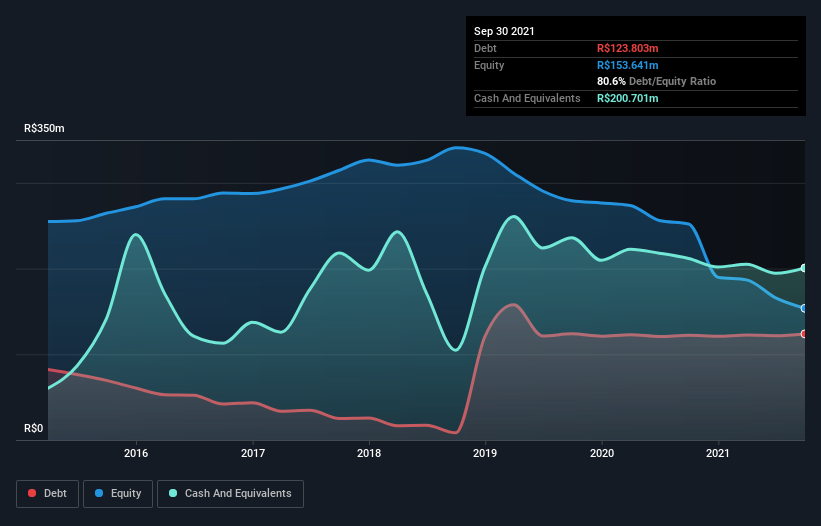

How Much Debt Does T4F Entretenimento Carry?

As you can see below, T4F Entretenimento had R$123.8m of debt, at September 2021, which is about the same as the year before. You can click the chart for greater detail. However, its balance sheet shows it holds R$200.7m in cash, so it actually has R$76.9m net cash.

How Healthy Is T4F Entretenimento's Balance Sheet?

According to the last reported balance sheet, T4F Entretenimento had liabilities of R$205.8m due within 12 months, and liabilities of R$137.7m due beyond 12 months. Offsetting these obligations, it had cash of R$200.7m as well as receivables valued at R$59.9m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by R$83.0m.

T4F Entretenimento has a market capitalization of R$178.6m, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt. While it does have liabilities worth noting, T4F Entretenimento also has more cash than debt, so we're pretty confident it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since T4F Entretenimento will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, T4F Entretenimento made a loss at the EBIT level, and saw its revenue drop to R$12m, which is a fall of 90%. That makes us nervous, to say the least.

So How Risky Is T4F Entretenimento?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And we do note that T4F Entretenimento had an earnings before interest and tax (EBIT) loss, over the last year. Indeed, in that time it burnt through R$33m of cash and made a loss of R$101m. But the saving grace is the R$76.9m on the balance sheet. That kitty means the company can keep spending for growth for at least two years, at current rates. Overall, we'd say the stock is a bit risky, and we're usually very cautious until we see positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 4 warning signs for T4F Entretenimento (1 is potentially serious) you should be aware of.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if T4F Entretenimento might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:SHOW3

T4F Entretenimento

Operates as a live entertainment company in South America.

Excellent balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

18 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6090.0% undervalued

21 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8142.8% undervalued

41 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CW

Cwburton on Verano Holdings ·

Waiting for the Inevitable

Fair Value:CA$5.5278.8% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.6% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8684.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

WA

Wane_Investment_House on FCMB Group ·

This aligns FCMB with global green finance standards and strengthens its attractiveness to impact investors. 4. Deepens Strategic Partnerships and International Collaboration The collaboration with FMO and HeaveVentures broadens FCMB’s relationship with: Development finance institutions (DFIs), Venture capital and innovation hubs, Global agri-value chain partners. These partnerships provide FCMB with: Access to co-financing opportunities, Technical expertise, Future pipeline collaboration, which collectively expands FCMB’s capacity to support complex and scalable agribusiness projects. 5. Builds a Pipeline for Future Lending, Investment, and Market Expansion The Hackathon serves as a feeder mechanism into FCMB’s broader agribusiness strategy by: Identifying innovative startups that can evolve into long-term borrowers or partners. Creating opportunities for structured financing, contract farming solutions, and supply-chain digitization. Enhancing FCMB’s advisory and merchant banking relevance in the agritech investment landscape. This creates a sustainable pipeline of bankable opportunities in a sector with high long-term growth potential. 6. Strengthens FCMB’s Brand Positioning and Competitive Advantage The initiative differentiates FCMB from peer institutions by: Showcasing its commitment to innovation-led economic transformation. Demonstrating leadership in supporting Nigeria’s food security agenda. Reinforcing customer loyalty in the SME and agribusiness segments. This positions FCMB as a future-ready financial partner with strong sectoral expertise and deep development impact. Strategic Outlook The FCMB AgriTech Hackathon 2025 is expected to deliver medium-to-long-term value by: Deepening FCMB’s market share in agribusiness finance, Enabling new digital lending frameworks, Strengthening ESG positioning, Expanding cross-border innovation partnerships, Supporting scalable agritech solutions capable of transforming Nigeria’s food system.

0

|0