Advertisement

- Brazil

- /

- Metals and Mining

- /

- BOVESPA:CSNA3

Companhia Siderúrgica Nacional (BVMF:CSNA3) Seems To Use Debt Quite Sensibly

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Companhia Siderúrgica Nacional (BVMF:CSNA3) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Companhia Siderúrgica Nacional

What Is Companhia Siderúrgica Nacional's Net Debt?

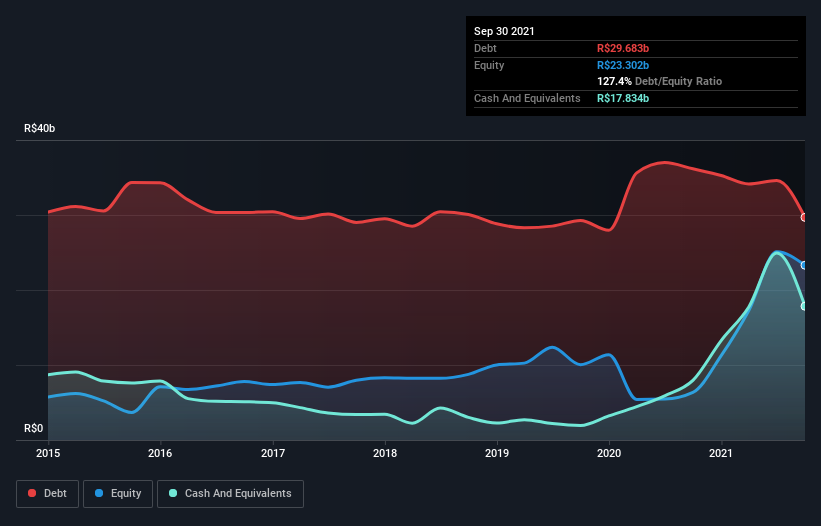

As you can see below, Companhia Siderúrgica Nacional had R$29.7b of debt at September 2021, down from R$36.2b a year prior. However, because it has a cash reserve of R$17.8b, its net debt is less, at about R$11.8b.

How Healthy Is Companhia Siderúrgica Nacional's Balance Sheet?

According to the last reported balance sheet, Companhia Siderúrgica Nacional had liabilities of R$22.2b due within 12 months, and liabilities of R$30.6b due beyond 12 months. On the other hand, it had cash of R$17.8b and R$4.60b worth of receivables due within a year. So its liabilities total R$30.3b more than the combination of its cash and short-term receivables.

This is a mountain of leverage relative to its market capitalization of R$35.6b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With net debt sitting at just 0.58 times EBITDA, Companhia Siderúrgica Nacional is arguably pretty conservatively geared. And this view is supported by the solid interest coverage, with EBIT coming in at 8.6 times the interest expense over the last year. Even more impressive was the fact that Companhia Siderúrgica Nacional grew its EBIT by 394% over twelve months. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Companhia Siderúrgica Nacional can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Companhia Siderúrgica Nacional generated free cash flow amounting to a very robust 86% of its EBIT, more than we'd expect. That positions it well to pay down debt if desirable to do so.

Our View

The good news is that Companhia Siderúrgica Nacional's demonstrated ability to convert EBIT to free cash flow delights us like a fluffy puppy does a toddler. But truth be told we feel its level of total liabilities does undermine this impression a bit. Taking all this data into account, it seems to us that Companhia Siderúrgica Nacional takes a pretty sensible approach to debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Companhia Siderúrgica Nacional has 5 warning signs (and 1 which makes us a bit uncomfortable) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:CSNA3

Companhia Siderúrgica Nacional

Operates as an integrated steel producer in Brazil and Latin America.

Undervalued average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor