Advertisement

- Brazil

- /

- Personal Products

- /

- BOVESPA:NTCO3

A Piece Of The Puzzle Missing From Natura &Co Holding S.A.'s (BVMF:NTCO3) Share Price

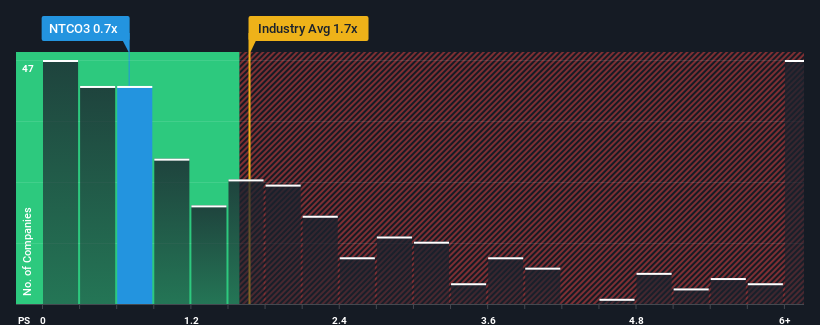

Natura &Co Holding S.A.'s (BVMF:NTCO3) price-to-sales (or "P/S") ratio of 0.7x might make it look like a buy right now compared to the Personal Products industry in Brazil, where around half of the companies have P/S ratios above 1.7x and even P/S above 4x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the reduced P/S.

Check out our latest analysis for Natura &Co Holding

What Does Natura &Co Holding's Recent Performance Look Like?

Natura &Co Holding could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

Want the full picture on analyst estimates for the company? Then our free report on Natura &Co Holding will help you uncover what's on the horizon.Is There Any Revenue Growth Forecasted For Natura &Co Holding?

The only time you'd be truly comfortable seeing a P/S as low as Natura &Co Holding's is when the company's growth is on track to lag the industry.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. This isn't what shareholders were looking for as it means they've been left with a 35% decline in revenue over the last three years in total. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 4.8% per annum during the coming three years according to the twelve analysts following the company. With the industry predicted to deliver 5.6% growth each year, the company is positioned for a comparable revenue result.

With this in consideration, we find it intriguing that Natura &Co Holding's P/S is lagging behind its industry peers. It may be that most investors are not convinced the company can achieve future growth expectations.

The Key Takeaway

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've seen that Natura &Co Holding currently trades on a lower than expected P/S since its forecast growth is in line with the wider industry. Despite average revenue growth estimates, there could be some unobserved threats keeping the P/S low. Perhaps investors are concerned that the company could underperform against the forecasts over the near term.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Natura &Co Holding (of which 1 makes us a bit uncomfortable!) you should know about.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

Valuation is complex, but we're here to simplify it.

Discover if Natura &Co Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:NTCO3

Natura &Co Holding

Engages in the manufacturing, distribution, and sale of cosmetics, fragrances, and personal care products in Brazil, Asia, Europe, North America, South America, the Middle East, Africa, and Oceania.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|24.5% undervalued

CH

Community Contributor