Advertisement

- Brazil

- /

- Consumer Services

- /

- BOVESPA:SEER3

These 4 Measures Indicate That Ser Educacional (BVMF:SEER3) Is Using Debt Extensively

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Ser Educacional S.A. (BVMF:SEER3) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Ser Educacional

What Is Ser Educacional's Net Debt?

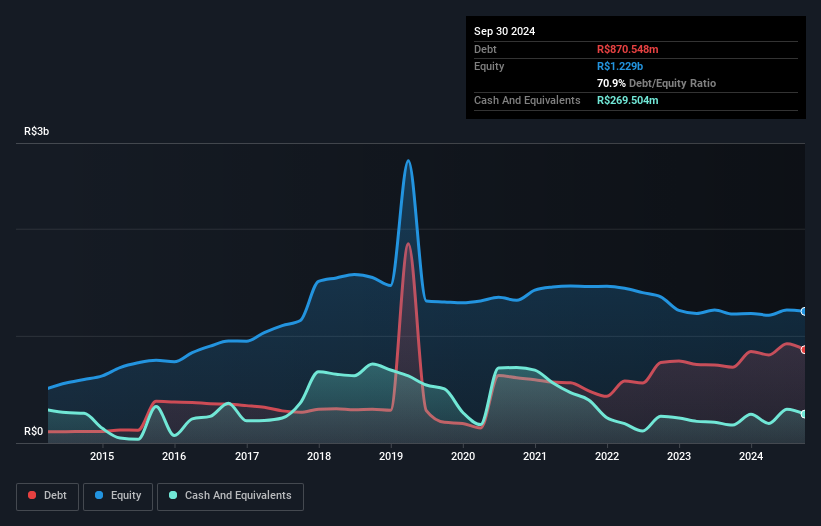

The image below, which you can click on for greater detail, shows that at September 2024 Ser Educacional had debt of R$870.5m, up from R$706.9m in one year. However, it does have R$269.5m in cash offsetting this, leading to net debt of about R$601.0m.

How Strong Is Ser Educacional's Balance Sheet?

The latest balance sheet data shows that Ser Educacional had liabilities of R$734.9m due within a year, and liabilities of R$1.46b falling due after that. Offsetting this, it had R$269.5m in cash and R$559.3m in receivables that were due within 12 months. So it has liabilities totalling R$1.37b more than its cash and near-term receivables, combined.

This deficit casts a shadow over the R$585.0m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Ser Educacional would probably need a major re-capitalization if its creditors were to demand repayment.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While Ser Educacional has a quite reasonable net debt to EBITDA multiple of 1.8, its interest cover seems weak, at 2.3. This does suggest the company is paying fairly high interest rates. Either way there's no doubt the stock is using meaningful leverage. Notably, Ser Educacional's EBIT launched higher than Elon Musk, gaining a whopping 182% on last year. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ser Educacional can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Looking at the most recent three years, Ser Educacional recorded free cash flow of 28% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Mulling over Ser Educacional's attempt at staying on top of its total liabilities, we're certainly not enthusiastic. But on the bright side, its EBIT growth rate is a good sign, and makes us more optimistic. Looking at the bigger picture, it seems clear to us that Ser Educacional's use of debt is creating risks for the company. If everything goes well that may pay off but the downside of this debt is a greater risk of permanent losses. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example Ser Educacional has 4 warning signs (and 2 which are potentially serious) we think you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:SEER3

Ser Educacional

Develops and manages activities for on-campus and distance-learning undergraduate, graduate, and professional training courses and other education-related areas in Brazil.

Reasonable growth potential and fair value.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.8% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.3% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.6% undervalued

RO

Community Contributor