Advertisement

- Brazil

- /

- Food and Staples Retail

- /

- BOVESPA:PNVL3

These 4 Measures Indicate That Dimed Distribuidora de Medicamentos (BVMF:PNVL3) Is Using Debt Extensively

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Dimed S.A. Distribuidora de Medicamentos (BVMF:PNVL3) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Dimed Distribuidora de Medicamentos

What Is Dimed Distribuidora de Medicamentos's Net Debt?

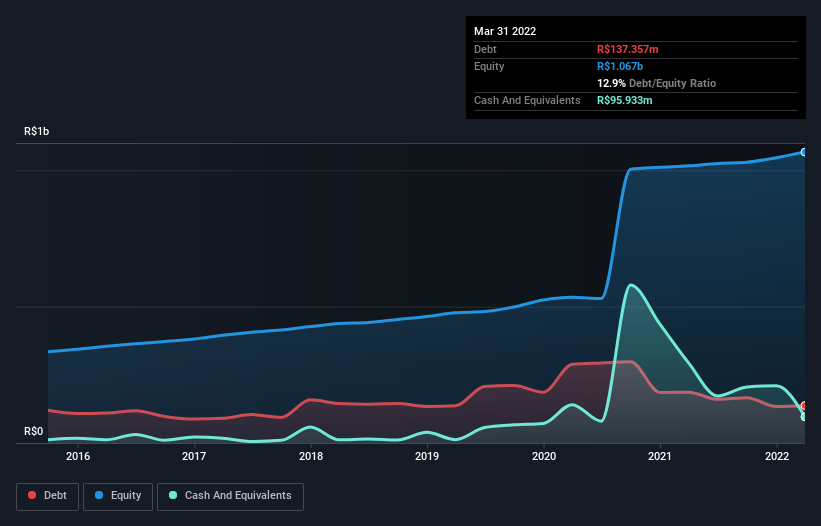

You can click the graphic below for the historical numbers, but it shows that Dimed Distribuidora de Medicamentos had R$137.4m of debt in March 2022, down from R$186.5m, one year before. However, because it has a cash reserve of R$95.9m, its net debt is less, at about R$41.4m.

How Strong Is Dimed Distribuidora de Medicamentos' Balance Sheet?

According to the last reported balance sheet, Dimed Distribuidora de Medicamentos had liabilities of R$869.1m due within 12 months, and liabilities of R$546.4m due beyond 12 months. On the other hand, it had cash of R$95.9m and R$487.2m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by R$832.3m.

While this might seem like a lot, it is not so bad since Dimed Distribuidora de Medicamentos has a market capitalization of R$1.49b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Dimed Distribuidora de Medicamentos's low debt to EBITDA ratio of 0.37 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 4.1 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. One way Dimed Distribuidora de Medicamentos could vanquish its debt would be if it stops borrowing more but continues to grow EBIT at around 15%, as it did over the last year. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Dimed Distribuidora de Medicamentos's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, Dimed Distribuidora de Medicamentos created free cash flow amounting to 15% of its EBIT, an uninspiring performance. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

Neither Dimed Distribuidora de Medicamentos's ability to convert EBIT to free cash flow nor its interest cover gave us confidence in its ability to take on more debt. But its net debt to EBITDA tells a very different story, and suggests some resilience. Looking at all the angles mentioned above, it does seem to us that Dimed Distribuidora de Medicamentos is a somewhat risky investment as a result of its debt. Not all risk is bad, as it can boost share price returns if it pays off, but this debt risk is worth keeping in mind. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example - Dimed Distribuidora de Medicamentos has 1 warning sign we think you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:PNVL3

Dimed Distribuidora de Medicamentos

Sells medicines, perfumeries, personal care and beauty products, cosmetics, and dermo-cosmetics in Brazil.

Undervalued with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor