Advertisement

- Belgium

- /

- Semiconductors

- /

- ENXTBR:MELE

Shareholders Will Probably Be Cautious Of Increasing Melexis NV's (EBR:MELE) CEO Compensation At The Moment

Key Insights

- Melexis' Annual General Meeting to take place on 14th of May

- Total pay for CEO Marc Biron includes €381.7k salary

- The total compensation is similar to the average for the industry

- Over the past three years, Melexis' EPS grew by 40% and over the past three years, the total shareholder return was 4.6%

CEO Marc Biron has done a decent job of delivering relatively good performance at Melexis NV (EBR:MELE) recently. As shareholders go into the upcoming AGM on 14th of May, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. Here is our take on why we think the CEO compensation looks appropriate.

See our latest analysis for Melexis

How Does Total Compensation For Marc Biron Compare With Other Companies In The Industry?

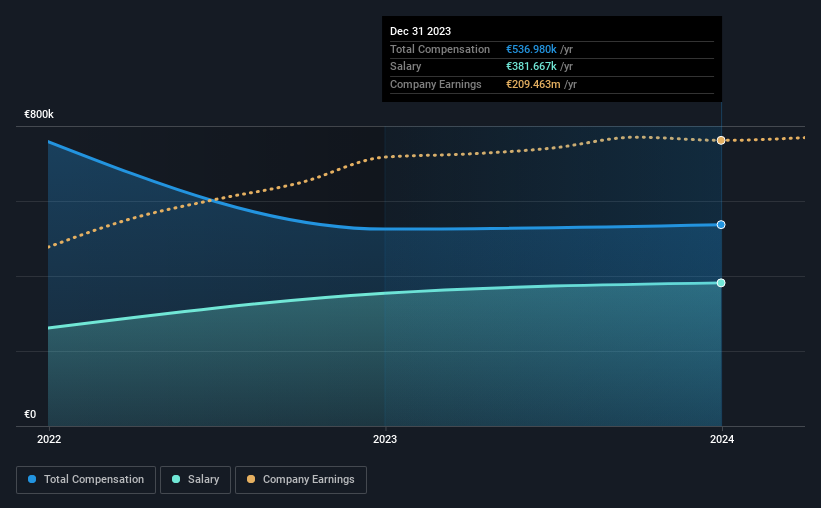

Our data indicates that Melexis NV has a market capitalization of €3.3b, and total annual CEO compensation was reported as €537k for the year to December 2023. That is, the compensation was roughly the same as last year. In particular, the salary of €381.7k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the Belgium Semiconductor industry with market capitalizations ranging from €1.9b to €6.0b, the reported median CEO total compensation was €537k. From this we gather that Marc Biron is paid around the median for CEOs in the industry.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | €382k | €354k | 71% |

| Other | €155k | €171k | 29% |

| Total Compensation | €537k | €525k | 100% |

On an industry level, roughly 45% of total compensation represents salary and 55% is other remuneration. Melexis pays out 71% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Melexis NV's Growth Numbers

Melexis NV's earnings per share (EPS) grew 40% per year over the last three years. Its revenue is up 11% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see decent revenue growth in the last year, suggesting the business is healthy and growing. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Melexis NV Been A Good Investment?

Melexis NV has generated a total shareholder return of 4.6% over three years, so most shareholders wouldn't be too disappointed. Although, there's always room to improve. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

In Summary...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. That's why we did our research, and identified 3 warning signs for Melexis (of which 1 is a bit unpleasant!) that you should know about in order to have a holistic understanding of the stock.

Important note: Melexis is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTBR:MELE

Melexis

Designs, develops, tests, and markets advanced integrated semiconductor devices primarily for the automotive industry in Europe, the Middle East, Africa, the Asia Pacific, and North and Latin America.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|32.6% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.6% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.6% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.2% undervalued

RO

Community Contributor