Stock Analysis

- United States

- /

- Capital Markets

- /

- NYSE:EVR

Prio And Two Other Stocks That May Be Priced Below Their Estimated Value

Reviewed by Simply Wall St

As global markets exhibit mixed signals with ongoing rotations and significant earnings reports influencing major indices, investors are navigating through a landscape marked by both uncertainties and opportunities. In this context, identifying stocks that may be undervalued becomes particularly pertinent, offering potential for those looking to invest in assets whose market prices might not fully reflect their underlying value.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Imeik Technology DevelopmentLtd (SZSE:300896) | CN¥161.99 | CN¥322.08 | 49.7% |

| Sumco (TSE:3436) | ¥2341.00 | ¥4661.70 | 49.8% |

| West China Cement (SEHK:2233) | HK$1.08 | HK$2.16 | 49.9% |

| Calnex Solutions (AIM:CLX) | £0.49 | £0.98 | 49.8% |

| Stewart Information Services (NYSE:STC) | US$73.25 | US$146.00 | 49.8% |

| Power and Water Utility Company for Jubail and Yanbu (SASE:2083) | SAR62.50 | SAR124.34 | 49.7% |

| Stratec (XTRA:SBS) | €41.30 | €82.14 | 49.7% |

| Elementis (LSE:ELM) | £1.532 | £3.05 | 49.7% |

| Sinch (OM:SINCH) | SEK28.54 | SEK56.74 | 49.7% |

| UCB (ENXTBR:UCB) | €152.05 | €302.46 | 49.7% |

Let's review some notable picks from our screened stocks.

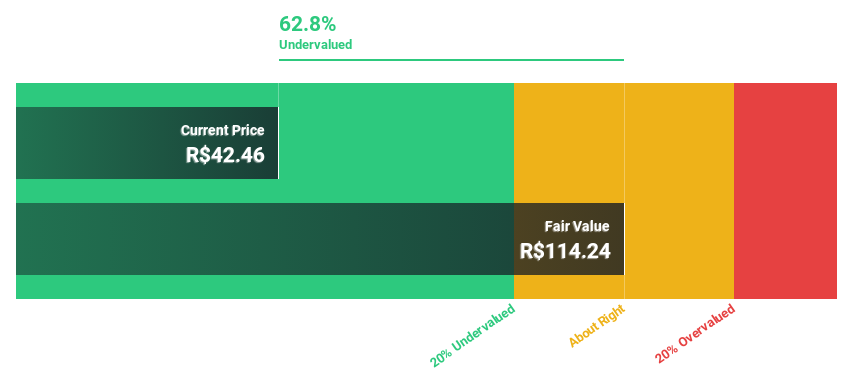

Prio (BOVESPA:PRIO3)

Overview: Prio S.A., along with its subsidiaries, focuses on exploring, developing, and producing oil and natural gas in Brazil and globally, with a market capitalization of R$39.78 billion.

Operations: The company generates its revenue primarily from the exploration and production of oil and gas, totaling R$12.39 billion.

Estimated Discount To Fair Value: 19.3%

Prio S.A. is currently trading below its estimated fair value by 19.3%, indicating potential undervaluation based on discounted cash flow analysis. With a robust forecast for earnings growth at 24.61% per year, Prio's financial performance is expected to outpace the Brazilian market's average. Despite a slight decline in net income and earnings per share in Q1 2024, the company maintains a strong cash position exceeding US$1 billion, actively seeking M&A opportunities to leverage this liquidity for expansion.

- In light of our recent growth report, it seems possible that Prio's financial performance will exceed current levels.

- Dive into the specifics of Prio here with our thorough financial health report.

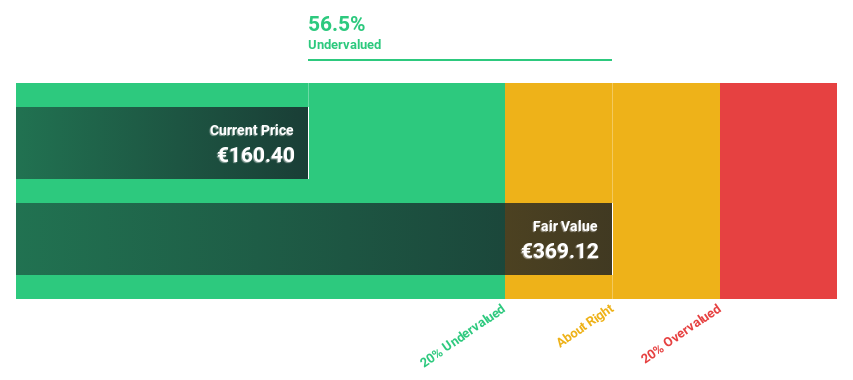

UCB (ENXTBR:UCB)

Overview: UCB SA is a global biopharmaceutical company focused on developing treatments for neurological and immunological diseases, with a market capitalization of approximately €28.85 billion.

Operations: The company generates €5.45 billion in revenue from its biopharmaceutical segment, specializing in neurological and immunological treatments.

Estimated Discount To Fair Value: 49.7%

UCB is trading significantly below its fair value, priced at €152.05 against an estimated €302.46, marking a substantial undervaluation based on discounted cash flow analysis. Despite recent financial results showing a decline in net income from €311 million to €208 million and earnings per share dropping from €1.64 to €1.09, UCB's future looks promising with expected earnings growth of 33.4% annually, outpacing the Belgian market forecast of 19.6%. However, its profit margins have decreased from last year's 6.5% to 4.4%, and return on equity is anticipated to be low at 13.9% in three years' time.

- Our comprehensive growth report raises the possibility that UCB is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of UCB.

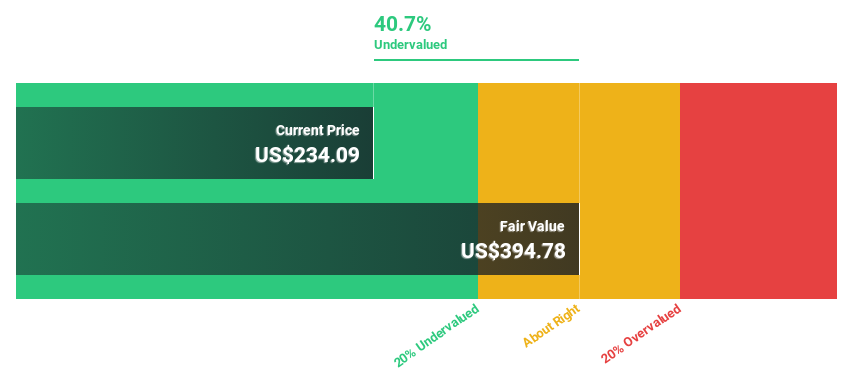

Evercore (NYSE:EVR)

Overview: Evercore Inc., along with its subsidiaries, functions as an independent investment banking advisory firm worldwide, boasting a market capitalization of approximately $10.98 billion.

Operations: The firm's revenue is primarily derived from its Investment Banking & Equities segment, which generated $2.55 billion, complemented by the Investment Management segment with revenues of $73.80 million.

Estimated Discount To Fair Value: 28.1%

Evercore is currently trading at US$249.23, well below the estimated fair value of US$346.66, suggesting significant undervaluation based on discounted cash flow metrics. The firm's earnings are projected to grow by 27.4% annually over the next three years, outstripping the US market projection of 14.9%. Despite recent shareholder dilution, Evercore's revenue growth forecast at 15.1% annually also exceeds market averages, and its return on equity is expected to be very high at 40.2% in three years' time.

- The growth report we've compiled suggests that Evercore's future prospects could be on the up.

- Take a closer look at Evercore's balance sheet health here in our report.

Taking Advantage

- Click here to access our complete index of 998 Undervalued Stocks Based On Cash Flows.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evercore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EVR

Evercore

Operates as an independent investment banking advisory firm in the United States, Europe, Latin America, and internationally.

High growth potential with adequate balance sheet and pays a dividend.