Advertisement

Revenues Working Against Mithra Pharmaceuticals SA's (EBR:MITRA) Share Price Following 39% Dive

The Mithra Pharmaceuticals SA (EBR:MITRA) share price has fared very poorly over the last month, falling by a substantial 39%. The recent drop completes a disastrous twelve months for shareholders, who are sitting on a 77% loss during that time.

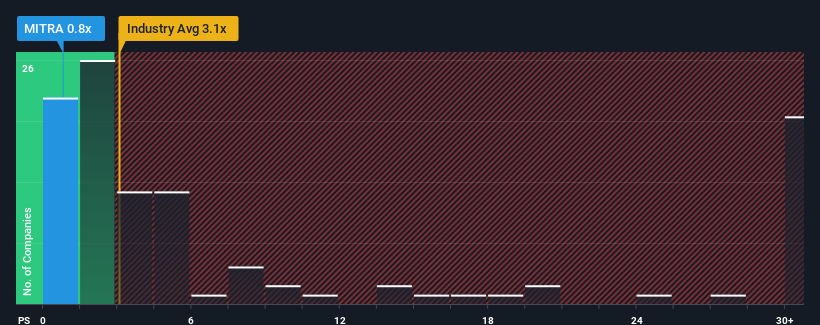

After such a large drop in price, Mithra Pharmaceuticals' price-to-sales (or "P/S") ratio of 0.8x might make it look like a strong buy right now compared to the wider Pharmaceuticals industry in Belgium, where around half of the companies have P/S ratios above 3.1x and even P/S above 14x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

See our latest analysis for Mithra Pharmaceuticals

How Mithra Pharmaceuticals Has Been Performing

Recent times have been advantageous for Mithra Pharmaceuticals as its revenues have been rising faster than most other companies. It might be that many expect the strong revenue performance to degrade substantially, which has repressed the share price, and thus the P/S ratio. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Mithra Pharmaceuticals.How Is Mithra Pharmaceuticals' Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as depressed as Mithra Pharmaceuticals' is when the company's growth is on track to lag the industry decidedly.

Retrospectively, the last year delivered an exceptional 186% gain to the company's top line. Despite this strong recent growth, it's still struggling to catch up as its three-year revenue frustratingly shrank by 21% overall. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to climb by 0.2% during the coming year according to the three analysts following the company. That's shaping up to be materially lower than the 11% growth forecast for the broader industry.

With this in consideration, its clear as to why Mithra Pharmaceuticals' P/S is falling short industry peers. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

The Key Takeaway

Having almost fallen off a cliff, Mithra Pharmaceuticals' share price has pulled its P/S way down as well. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

As expected, our analysis of Mithra Pharmaceuticals' analyst forecasts confirms that the company's underwhelming revenue outlook is a major contributor to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. It's hard to see the share price rising strongly in the near future under these circumstances.

You need to take note of risks, for example - Mithra Pharmaceuticals has 5 warning signs (and 2 which shouldn't be ignored) we think you should know about.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ENXTBR:MITRA

Mithra Pharmaceuticals

Develops, manufactures, and markets complex therapeutics in the areas of contraception, menopause, and hormone-dependent cancers in Belgium, Europe and internationally.

High growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.8% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.2% undervalued

AX

Community Contributor