Aussie Broadband (ASX:ABB): Evaluating Valuation After FY26 Guidance Shifts and Bullish Broker Outlook

Reviewed by Kshitija Bhandaru

Aussie Broadband (ASX:ABB) shares slipped 1.5% after a trading update revealed that FY26 growth forecasts fell short of market expectations, sparking a swift reaction among investors and industry watchers.

See our latest analysis for Aussie Broadband.

Despite the short-term wobble following its cautious FY26 outlook, Aussie Broadband’s share price is still up an impressive 58% so far this year, and its three-year total shareholder return has soared over 150%. Recent volatility mainly reflects shifting market sentiment as investors weigh slower near-term guidance against the company’s strong long-term growth track record and upbeat broker commentary, which points to future upside.

If you’re interested in companies showing strong momentum and resilience, now is the perfect time to broaden your search and uncover fast growing stocks with high insider ownership

With cautious guidance clashing against upbeat broker forecasts and the stock trading below its estimated fair value, the real question is whether Aussie Broadband represents a bargain at current levels or if future growth is already reflected in the price.

Most Popular Narrative: 3.3% Undervalued

With a narrative fair value of A$5.79 compared to a last close price of A$5.60, Aussie Broadband sits just under analyst consensus. This reflects optimism for further upside based on projected growth and margin expansion.

The ongoing rollout of faster NBN plans, new full fibre (FTTP) and HFC upgrades, and the proliferation of connected devices in Australian households are expected to significantly increase demand for high-speed broadband. This positions Aussie Broadband to capture higher ARPU and market share, supporting both top-line revenue growth and margin expansion.

Earnings upgrades, bullish revenue growth trends, and a radical shift in profit margins are the backbone of this narrative. Want to discover the bold assumptions powering this valuation? See which upgrades and forecasts are driving the price target and what happens if they hold up?

Result: Fair Value of $5.79 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing price competition or regulatory shifts could squeeze margins; this could quickly derail expected earnings growth and put the bullish outlook at risk.

Find out about the key risks to this Aussie Broadband narrative.

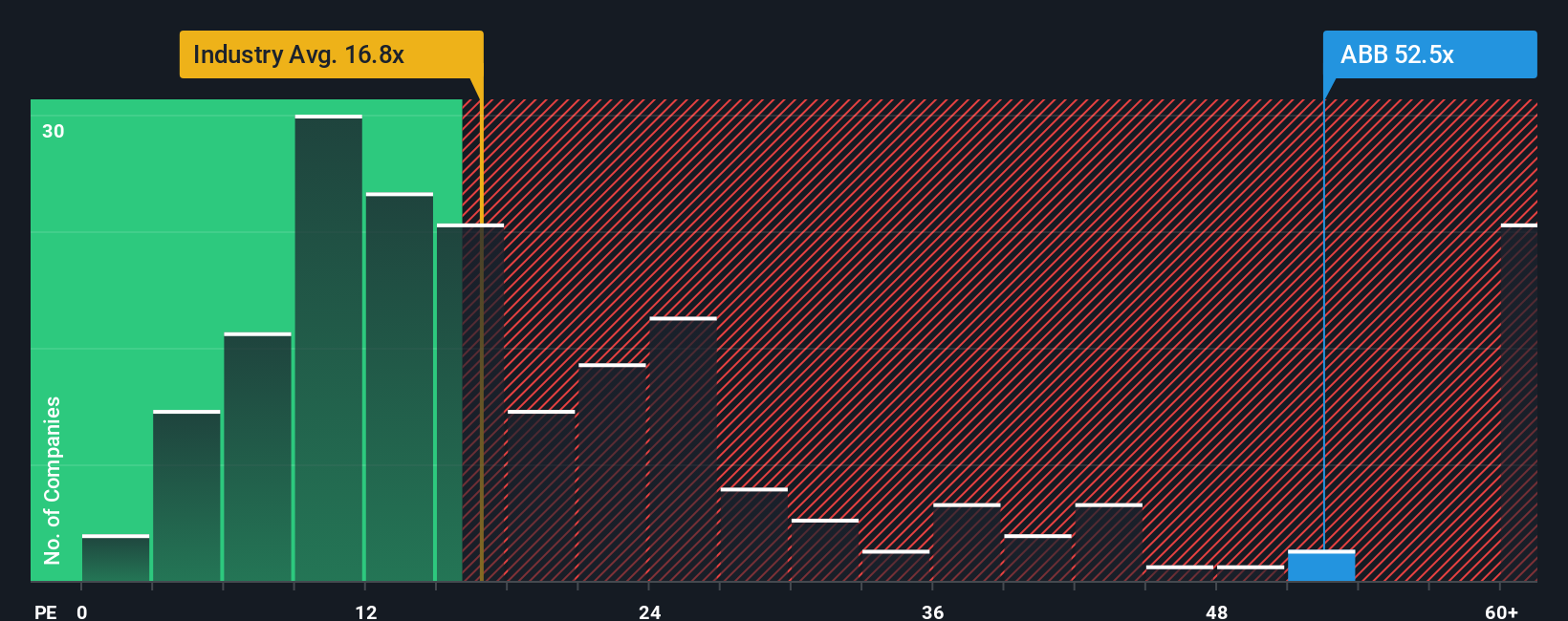

Another View: Market Ratios Signal Caution

Looking through the lens of the common price-to-earnings ratio, Aussie Broadband comes up as pricey, with a 49.9x multiple, much higher than both its peer average of 21.4x and the industry fair ratio of 38.5x. This suggests the market sees a lot of future growth, but also heightens the risk if expectations slip. Is this premium a signal of confidence or potential trouble for new investors?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Aussie Broadband Narrative

If the consensus doesn’t match your perspective or you prefer taking a hands-on approach, you can dive into the numbers and craft your own view in just a few minutes, too, and Do it your way

A great starting point for your Aussie Broadband research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don’t let your next big opportunity slip by. Simply Wall St’s powerful Screener can help you uncover fresh stock ideas tailored to your interests and goals.

- Unleash the potential of technology with these 25 AI penny stocks that are fueling advancements in artificial intelligence and automation across industries.

- Boost your portfolio with steady income by targeting these 18 dividend stocks with yields > 3% offering yields above 3% for consistent returns.

- Stay ahead of undervalued gems and get a jump on market opportunities with these 881 undervalued stocks based on cash flows based on real cash flow analysis.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:ABB

Aussie Broadband

Provides telecommunications and technology services in Australia.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion